Xylem Inc. (NYSE:XYL) has been performing well over the past 12 months, with the share price increasing 45% since November 2023.

In this article, I considered reviewing Xylem’s recent financial performance, with a focus on the headwinds and pressures that the company is currently facing, including a significant decline in orders in their water infrastructure segment due to delays in large infrastructure projects in China.

In my view, shareholders have fully priced in the good performance of the company and the smooth integration of Evoqua Water Technologies.

I believe the overbuying activity in May, followed by a 10% decline in the share price could be an early sign of shareholder excitement cooling off, which may continue through the second half of the year.

I will provide the rationale behind my Hold rating in the outlook section. For now, I will start with a brief company overview for those readers new to this stock.

Business Overview

Xylem is an American-based company that designs, manufactures, and services products for water-related applications. They are focused on the entire water cycle, from delivering, treating, and measuring drinking water, to collecting and treating wastewater before returning it to the environment.

I considered including below a breakdown of their revenue per business segment over the past 3 years.

| Business Segment | 2023 Revenue (in millions USD) | 2022 Revenue (in millions USD) | 2021 Revenue (in millions USD) |

|---|---|---|---|

| Water Infrastructure | $2,967 | $2,364 | $2,247 |

| Applied Water | $1,853 | $1,767 | $1,613 |

| Measurement and Control Solutions | $1,729 | $1,391 | $1,335 |

| Integrated Solutions and Services | $815 | – | – |

| Total | $7,364 | $5,522 | $5,195 |

Author’s compilation from the latest 10-K available.

As a side note, their newly integrated solutions and services segment was introduced in 2023 following the acquisition of Evoqua Water Technologies.

Despite the water infrastructure segment accounting for 40% of their total revenue in 2023, I like that the other segments aren’t too far behind; applied water accounts for 25%, which is about the same as the measurement and control solutions, and their integrated solutions segment accounts for 11%.

As a side note, my investment style favors businesses with diversified revenue streams that don’t heavily rely on one single segment.

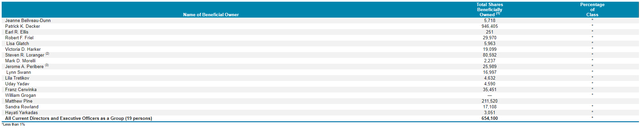

In regards to the company ownership, their latest published 14A shows that the total stake among all 19 directors and executive officers is less than 1%. Frankly, I would like to see management have more skin in the game.

SEC | 14A

Recent performance

As always, I like to start with the dessert, so I will cover the headwinds first.

Their measurement and control solutions segment experienced an 18% decline in new orders, with a backlog reduction of 12% YoY. In my view, this is a strong indication of their high sensitivity to delays in large infrastructure projects.

Another example of these delays is the decline in orders from China in the water infrastructure segment during the first half of 2024 due to broader economic challenges in China, where government funding for large infrastructure projects is becoming increasingly constrained.

Another pressure comes from a demand softness in developed markets, particularly in commercial real estate and manufacturing (mainly the US and Europe), which led to a 4% decline in revenue in the applied water systems segment. In my view, this segment is highly cyclical and sensitive to macroeconomic conditions, which can cause big fluctuations in the total revenue.

Aside from these headwinds, their Q2 results were quite favorable, beating both EPS and revenue estimations, and raising their full-year guidance.

EPS increased by 78%, and revenue increased by 26%, reaching $2.2 billion. This was mainly driven by a 26% revenue growth in their measurement and control solutions segment.

Additionally, the water infrastructure segment also performed well, with a 22% increase in revenue.

Profitability-wise, I favor the 1.7% increase YoY in their adjusted EBITDA despite the challenges that come with the integration of a newly acquired company.

In regards to their newly revised guidance, management raised full-year revenue guidance to $8.55 billion, up by 16%, with an organic revenue growth forecast of 5% to 6%. Adjusted EPS guidance has been increased from $4.18 to $4.28.

Despite these good results and an increase in guidance, the share price dropped by over 5% during the Q2 earnings release day. I view this as a strong indication that good results are already priced in by shareholders. I discuss more details in the next section.

Outlook

Let’s start with a quick look at the weekly chart below.

Trading View

I like the clear uptrend that started in 2020, which, I believe, is backed up by solid growth. A quick look at the chart below shows an increase in both operating income, net income, and EBITDA since 2020.

Trading View

However, the weekly chart above shows the RSI at a level above 80 during mid-May 2024, which indicates overbuying activity. Therefore, I am not surprised to see a 10% decline in the share price since the peak in May this year.

From a technical analysis perspective, I don’t like seeing the support line of the upward trend far below the current share price. I’m not saying the price will drop to that support line—in fact, I believe there’s a very low chance of it reaching the $100 level. However, if the pressures and headwinds that I discussed earlier persist and they miss their full-year guidance, this lower support line could be an interesting entry point for a long position if there is a major selloff.

The main reason I believe now is probably not a good moment to enter a long position is due to their excessively high valuation ratios.

EV/EBITDA is 53% above the sector median, price to sales is 152%, price to cash flow is 83% and price to book value is 9% above the Industrials sector median.

Another key factor in my investment style is recent insider buying activity in the open market. Frankly, I am discouraged by the lack of insider buying activity in the past 2 years, which in addition to the management’s low stake in the company (<1% ownership among all 19 directors and executive officers) is not something I favor.

Conclusion

To conclude, I believe that despite a good second quarter, with strong revenue, adjusted EBITDA growth, and a raised guidance, the good performance of the company is most likely fully priced in.

The overbuying activity in May, followed by a 10% decline in the share price could be an indication of shareholder excitement cooling off, which I view as a healthy sign, considering the RSI was over 80 in mid-May.

However, I believe there is still a risk for a continued decline toward the support of the upward trend line in the weekly chart, especially if the delays in large infrastructure projects in China persist during the second part of the year.

Another factor that motivates my Hold rating is the high valuation ratios when compared to the industrials sector, especially for the price to sales and EV/EBITDA ratios.

Nonetheless, I believe it is worth keeping this stock on your watch list in case a selloff drives the share price down to the upward trend line support level. This would be close to the $100 price mark, which I believe is a good price to initiate a long position. However, until then, my rating for this stock is a Hold.

Read the full article here