Introduction

With the market evidently cautious about the mega-cap stocks, income investors can actually embrace many interesting income alternatives. Virtus InfraCap U.S. Preferred Stock ETF (NYSEARCA:PFFA) is an attractive income play offering a 9% dividend and featuring a unique portfolio with an infrastructure focus. These companies will get a much needed business boost when the rate-cutting cycle starts. Despite the non-investable credit rating (BBB-), I consider PFFA a buy considering the friendly macro backdrop and the active management to deal with the credit risks. Income investors may want to include it in their shopping list.

PFFA ETF Highlight

PFFA is a preferred stock ETF actively managed by Virtus, with an official fund description shown as below:

The Fund seeks current income and, secondarily, capital appreciation through a portfolio of preferred securities issued by U.S. companies with market capitalizations of over $100 million.

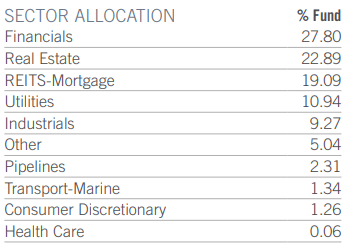

Unlike some of the sector-focused preferred stock ETFs, ETF has exposures to many major sectors except technology, as shown below. This is so because of its infrastructure-centric approach for asset allocations. In fact, sectors like Financials (27.8%), Real Estate (22.89%), REITs (19.09), Utilities (10.94%), Industrials (9.27%) are the sectors where the quality preferred shares can often be found. The diversification of the sectors increases the breadth of the portfolio and reduces the overall volatility.

PFFA Sector Allocation – from Virtus ETF Fact Sheet

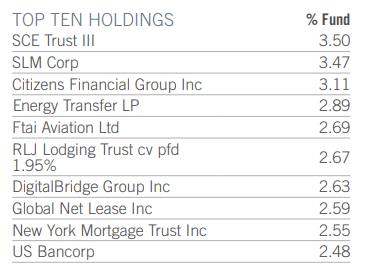

There are 208 holdings in the portfolio. The following is top 10 list. These holdings are scattered in the financial banks, REIT, MLP, etc., the sectors highlighted above.

PFFA Top Ten Holdings – from Virtus ETF Fact Sheet

This active managed ETF uses leverages to enhance the income and portfolio performance. The target range of leverage is 20-30%, which is slightly lower than the average leverage CEF funds use.

In addition, the management also uses option strategies to increase income, and hedge interest rate risk. As a result of heavy activities, the ETF charges pretty hefty fees with a 2.52% expense ratio.

However, the ETF offers high monthly paid dividends with a 9.09% yield. This is the most attractive feature to the income investors.

PFFA was incepted on May 15, 2018. It has gained quite popularity in its relative short history of 6 years or so. The AUM is at $1.17B currently, with a decent trading liquidity.

Preferred stocks benefit from macro tailwinds.

Preferred stocks are often considered as “a hybrid investment” with market characteristics illustrating a mix of common stocks and bonds. For example, the preferred shares behavior like equity stock, although much less volatile. On the other hand, they are sensitive to interest rate changes, similar to bonds. Therefore, it is expected that preferred stocks will get a boost from the rate cut that is highly anticipated in mid-September.

Furthermore, PFFA employs a high leverage, which will add positive impact to the return when the rate cutting cycle gets started. This is when the borrowing cost will be reduced, and more importantly the risky leverage should produce the corresponding high return. In other words, the macro backdrop seems to be supportive to the leveraging approach, this is the risk I am willing to take for the high-yield dividend income under the ETF’s active management, including its rate-hedging option approach.

There are strong signals for recent growth.

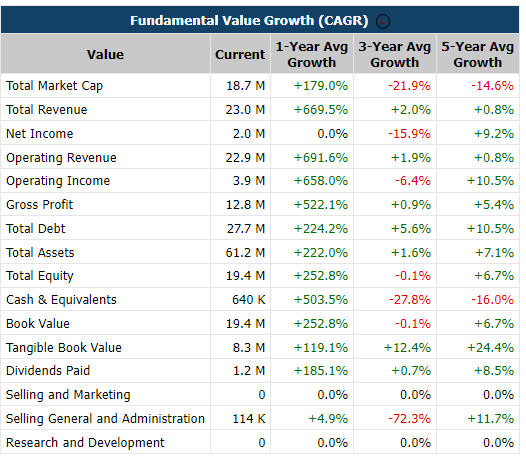

On the aspect of the stock characteristics, PFFA portfolio has shown very encouraging improvements in growth. The following is the CAGR metrics for the aggregation of all the constituents in the portfolio. It can be seen that the total revenue is increased by almost 700% year-over-year. The gross profit is increased by 522.1%. Keep in mind that these huge incremental growth rates are based on a very bad year prior to the current one. But they do give strong signals for the recovery of the business growth in the covered sectors. Those companies selected by the ETF are perhaps among the best growth plays that can be found in their corresponding industries.

PFFA Growth Metrics – from marketchameloen.com

I believe that the most interesting growth for income investors should be the dividend growth. If I just take the 5-year average of 8.5%, it would make it an impressive dividend-growth “stock” almost since its inception (2018).

Please note that PFFA ETF itself has not been able to illustrate the similar dividend growth because of the fund-specific volatilities, caused by the leverages and the option overlay deployed by the fund. But the constituents’ dividend growth can certainly be viewed as a base insurance for maintaining PFFA’s high yield.

Market rotation tailwinds will help the total performance.

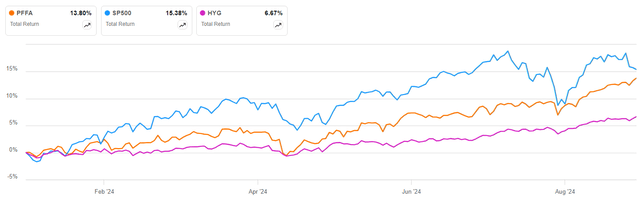

PFFA stock price has done reasonably well in 2024. The following chart shows the performance comparisons with S&P500 index and the high-yield bond ETF HYG. PFFA’s total performance has gained 13.86% so far this year. It is very close to S&P 500’s 15.38% gain. On the other hand, HYG’s gain is only about half at 6.67%. While it pretty much conforms the mixed behavior of the preferred shares as mentioned earlier, the PFFA’s total performance has been closer to the upper end on the stock side, not the lower end on the bond side in 2024.

PFFA Performance YTD – from SA charting

There is currently a “growth scare” in the stock market, which could be a catalyst for value rotations in the coming months. I believe that Investors will continue to move from the mega-cap growth stocks. The top sectors of PFFA’s allocation, including Financials, Utilities and Industrials, are the traditional “value” sectors. These are the sectors where I expect more money will flow into in the near future. The preferred shares will benefit from this type of market rotation.

The other two key sectors in PFFA’s portfolio, Real Estate and REITS-Mortgage, are on the verge of recovery in their own market, thanks to the promising rate cut. The preferred shares in these sectors are also expected to be the market winners during the rotations.

In fact, the above chart has already shown some strong signals for the rotations. PFFA has been on a relative steady climb. Even during the recent pullback of the stock market in late July, PFFA just had a small dip then. The most recent price behavior demonstrates a more convincing trend divergence between PFFA and S&P 500. They seem to move in different directions. It is still too early to tell if PFFA would actually outperform the broad market in terms of total performance in the rest of 2014. However, I certainly believe these “value” sectors will continue to perform well in the foreseeable future.

I currently have some minor position with PFFA in my income portfolio and I plan to buy in dip and accumulate more shares for the attractive 9% dividend, and a promising anticipation of good total returns in 2024.

Risks & Caveats

Generally speaking, preferred stock is of higher risk than bonds, although it is safer than the common stock. Compared to the bond investment, preferred shares are lower in seniority than bondholders. In the case of liquidation due to company bankruptcy, preferred shareholders get paid after bondholders. So the ETFs of preferred shares could be affected more by the company bankruptcy once it happens.

Infrastructure companies are usually capital intensive and tend to be rate sensitive. There is a risk of inflation staying at the current high level. This may affect the rate cutting and have a negative impact on the ETF’s performance.

Investors should also look at the risk statement contained in the ETF’s Factsheet, including the leverage risk, non-diversification risk etc., before making an investment decision.

Closing Thought

Preferred stock ETFs are income alternatives for investors with high yield such as 9% in mind. PFFA has an infrastructure-centric portfolio which covers multiple sectors, which are considered to be value asset classes. The portfolio should perform well during the market rotations. The constituent companies are experiencing a significant growth recovery after being hit hard from the rapid rate hiking. The highly anticipated rate cut will be a tailwind for the continued growth. I rate PFFA as a buy and recommend it to the income seekers.

Read the full article here