MELI’s High Growth Investment Thesis Is In Overdrive

We previously covered MercadoLibre, Inc. (NASDAQ:MELI) in July 2024, discussing why we had reiterated our Buy rating then, attributed to its double beat FQ1’24 earnings call, growing market share in Latam, and robust performance metrics.

We had also highlighted a few metrics that readers should look out for in the FQ2’24 earnings call on August 02, 2024, with it underscoring the health of its businesses along with near-term prospects.

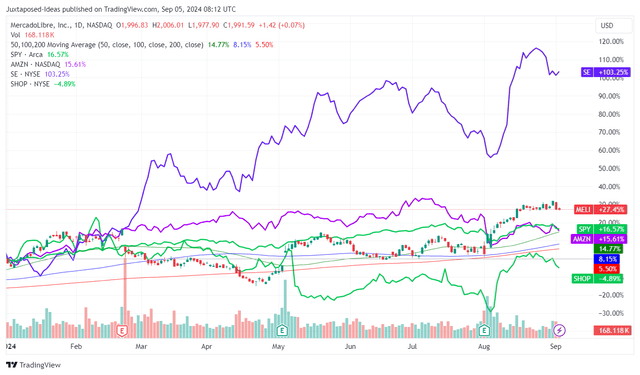

MELI YTD Stock Price

Trading View

Since then, MELI has generated a robust return of +16.9%, well outperforming the wider market at -2%. Otherwise, by +215.8%/ +53.2% since the June 2022 bottom, respectively.

Much of the tailwinds are attributed to the massive sell off that occurred after the September 2021 peak, which decimated most of the stock’s COVID-19 pandemic gains.

This is significantly aided by MELI’s seven consecutive quarters of top/ bottom line beats, one that we have also observed in the FQ2’24 quarter, with revenues of $5.07B (+17% QoQ/ +41.6% YoY) and adj EPS of $10.48 (+54.5% QoQ/ +103% YoY).

MELI’s Robust Performance Metrics

Seeking Alpha

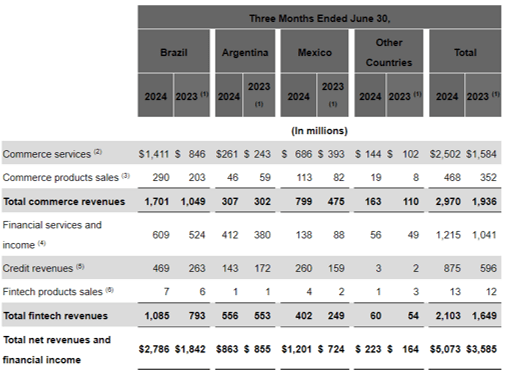

Much of MELI’s top-line growth is attributed to the accelerating total commerce revenues of $2.97B (+19.2% QoQ/ +53.8% YoY), with it well outperforming the fintech segment at $2.1B (+14.7% QoQ/ +28% YoY).

With commerce service revenues comprising fees derived from intermediation services/shipping/ storage fees and classified fees derived from classified advertising services/ ad sales, we believe that commerce remains its top-line driver at approximately 91.5% of its FQ2’24 sales.

This is because the MELI management already highlights that its advertising penetration reaches 2% of its commerce GMV in FQ2’24 (+0.4 points YoY) – implying $252M in advertising revenues (+51% YoY constant currency) based on the GMV of $12.64B (+83% YoY constant currency).

Even so, with most of the advertising tailwinds attributed to “great performance coming from cross-border sellers from 1P brands and that product continues to represent the majority of the business,” we believe that there remain great future growth opportunities as the management scales its advertising business to complement its ecommerce business.

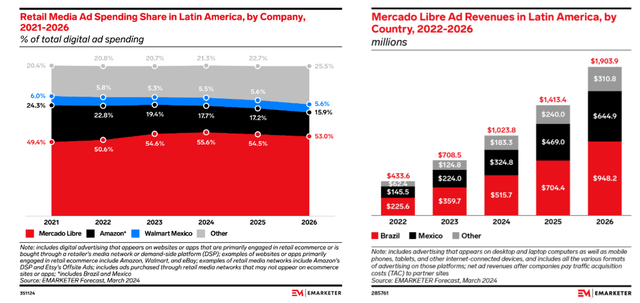

MELI’s Future Advertising Opportunities

eMarketer

If anything, eMarketer already expects MELI’s advertising revenues to grow from $708.5M in 2023 to $1.9B in 2026, expanding at an accelerated CAGR of +39.4% and potentially, being its top/ bottom-line driver given the typically high margin nature of the advertising business.

This is on top of the projected expansion in its retail media ad spending market share to 53% by 2026, up from 49.4% in 2021, if not more – based on the company’s “eighth consecutive quarter with a (advertising) growth rate above +50%” on a YoY basis.

As a result of the high growth trend and the accelerating bottom-line growth as discussed above, it is unsurprising that MELI has outperformed its commerce peers on a YTD basis, aside from Sea Limited (SE).

Readers must not ignore MELI’s fintech segment as well, Mercado Pago, with the management already reporting growing fintech Monthly Active Users [MAU] of 52M (+6.1% QoQ/ +36.8% YoY) in the latest quarter.

We believe that much of its success is attributed to the strategic launch of “the remunerated account, which pays interest as soon as funds are deposited with immediate liquidity” – one that we have similarly observed with MariBank, a digital bank that is a wholly owned subsidiary of SE.

This strategy has allowed MELI to report tripled user and more than doubled USD Assets Under Management [AUM] growth over the past 18 months in Argentina, triggering the country’s consolidated net revenues and financial income growth by +285% YoY at constant currency.

The same has been observed in Brazil, with +46% YoY growth in MAU, +86% in AUM, and +59% in sales.

As a result of these promising early results, it is unsurprising that MELI has announced its intention to apply for a digital banking license in Mexico in May 2024, allowing the company to tap a high growth fintech opportunity while improving its cross selling to the existing commerce users in the country.

While the management does not break down its digital banking segment’s bottom-line performance, we may infer from SE Digital Financial Services’ rich adj EBITDA margins of 31.7% in the latest quarter (+2 points QoQ/ -0.3 YoY), with it suggesting MELI’s (likely to be) highly profitable fintech business.

Lastly, while Mercado Pago’s consolidated Net Interest Margins After Losses [NIMAL] has already moderated to 31.1% (-0.4 points QoQ/ -5.7 YoY), part of the headwinds are attributed to the lower spreads on its credit card, one that we have also observed with other credit card issuers as delinquency rates/ charge-off rates normalize.

Part of the risks are also attributed to Argentina’s ongoing devaluation, which has triggered MELI’s impacted consolidated net revenues and financial income growth at +1% YoY in the country, compared to +285% YoY at constant currency.

This issue has led to contraction in its overall EBIT margins on a comparable basis by approximately 120 basis points YoY, partly attributed to the higher bad debt provisioning as well, as the management seeks to grow its credit book origination – explaining the impacted NIMAL margins, as discussed above.

However, readers must also note that MELI’s 15-90 day NPL has already moderated to 8.2% (inline QoQ/ -1.1 points YoY), with it highlighting the fintech’s robust portfolio quality and the improving underwriting capability.

These developments further underscore why MELI has outperformed as it does, thanks to its well diversified growth prospects across the e-commerce, logistics, fintech, and advertising offerings

So, Is MELI Stock A Buy, Sell, or Hold?

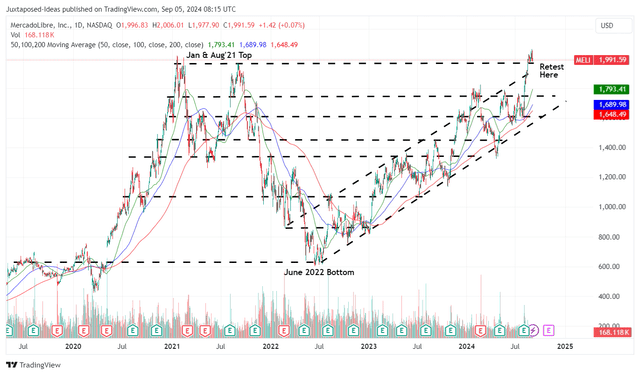

MELI 5Y Stock Price

Trading View

For now, MELI has sustained the robust upward trend since the June 2022 bottom, with minimal deviation observed thus far as the stock trades closely to its 50/ 100/ 200 day moving averages.

However, based on the LTM adj EPS of $32.37 ending FQ2’24 and the 1Y P/E mean of 45x, it is apparent that the stock is now trading at a notable premium to our fair value estimates of $1.45K.

Does this mean that we are downgrading MELI to a Hold now?

Not quite.

One, we maintain our belief that MELI remains a compelling growth stock with robust double digit growth prospects over the next few years. With market leaders rarely coming cheap, we believe that investors should only time their buys according to market sentiments and dollar cost averages.

This is especially since the stock is currently trading at a relatively reasonable PEG ratio of 1.42x, based on the the FWD non-GAAP P/E of 55.82x (higher than its 1Y mean of 45x) and the projected adj EPS expansion at a CAGR of +39.3% through FY2026.

When compared to its well diversified commerce peers, such as:

- Amazon.com, Inc. (AMZN) at 1x (author’s calculation, based a similar method at FWD non-GAAP P/E of 36.74x and adj EPS growth at +36.6%),

- Shopify (SHOP) at 1.95x (author’s calculation, based on 65.88x and +33.7%),

- SE at 0.53x (author’s calculation, based on 41.40x and +77.6%),

it is undeniable that MELI is trading somewhat attractively here.

Two, there remains an excellent upside potential of +38.6% to our reiterated long-term price target of $2.76K from current levels (otherwise upgraded to $2.82K), based on the 1Y P/E mean of 45x (attributed to the fluctuation from 1Y peak of 62.66x and 1Y low of 40.78x) and the consensus FY2026 adj EPS estimates of $61.52 (otherwise upgraded to $62.76).

Otherwise, interested investors may want to wait for a moderate pullback to our recommended entry point of $1.65K for an improved margin of safety.

This potential correction is not overly aggressive indeed, since MELI has recently broken out of its uptrend pattern as it has in early 2024, with a further correction to its previous support levels of $1.65K likely in the near-term and those levels triggering an expanded upside potential of +70% to our raised long-term price target.

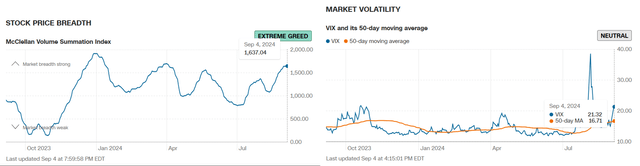

Stock Market Volatility

CNN

With the CBOE Volatility Index already exceeding October 2023 levels and the McClellan Volume Summation Index hitting extreme greed levels of 1,637 (compared to the neutral levels of 1,000x), we believe that there may be more volatility in the near term indeed.

As a result, while we remain optimistic about MELI’s long-term prospects, we believe that there may be near-term market-wide correction as observed in SPY’s moderation since the end of August 2024.

While we are reiterating our long-term Buy rating, interested investors may want to monitor its stock movement for a little longer before adding at its upcoming pullback to the support levels of $1.65K for an improved margin of safety.

Read the full article here