Investment Thesis

I recommend holding Sendas Distribuidora (NYSE:ASAI) shares after its Q2 results. The company reported mixed results, with a healthy 11.8% revenue growth and margin gains.

However, there was a slowdown in same-store sales growth and profitability was negatively impacted by higher financial expenses, which makes me cautious and reiterate the recommendation from my last report.

The period after the results also saw rumors of a possible merger between Sendas Distribuidora and Grupo Mateus, with shares traded on the Brazilian stock exchange, but without any major developments up to that point.

Review Of Sendas Distribuidora’s 2Q24 Results

Sendas Distribuidora released its results on August 8th, and as we can see below, they came in slightly below expectations.

Earnings (Investing)

Below, I will provide a full report on Sendas Distribuidora’s results for the 2nd quarter. It is important to note that the company releases its results in BRL, and I will convert them to dollars using the exchange rate of 1 dollar = 5.59 reais, as this was the exchange rate on the last day of the second quarter. Enjoy your reading!

Revenue – Slowdown In Same-Store Sales Growth

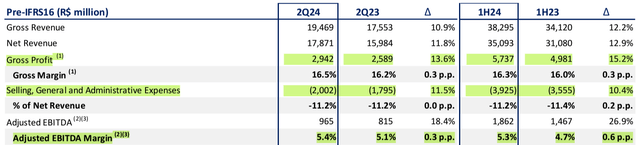

Sendas Distribuidora achieved a nice 11.8% annual increase in net revenue to BRL 17.8 billion ($3.2 billion). This was due to its expansion strategy, with the opening of 24 stores, 9 of which were renovated.

Net Revenue (IR Company)

However, the company also stated that same-store sales had annual growth of only 2.9%, a reduction of 0.5% compared to 1Q24. Growth was also below competitor Atacadão (OTCPK:ATAAY) which was 7.4% y/y, and this makes me skeptical about the thesis.

Costs, Expenses and Margins – Good Trends

With strict cost and expense control, Sendas Distribuidora achieved gross margin and adjusted EBITDA expansion in 2Q24. The company attributed the improvement to store maturation and an effective commercial strategy with no promotional campaigns in the quarter.

Margins (IR Company)

As for perspectives, I believe that the continuous expansion and maturation of stores should keep the EBITDA margin at good levels, even if it brings an increase in operating expenses at first.

Debt – Reducing Leverage

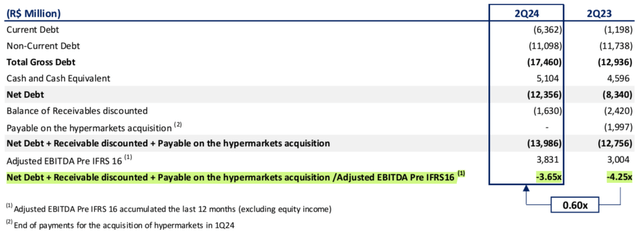

The company achieved good deleveraging in the annual comparison, reaching 3.6x EBITDA (4.25x in 2Q23). Net debt reached BRL 13.9 billion ($2.48 billion).

Net Debt / EBITDA (IR Company)

In my view, one of the major triggers for the company’s shares to rise sharply is for the company to deleverage to levels below 1x EBITDA. I believe this process is underway, but it will still take some time, and this corroborates my recommendation to hold the shares.

Net Income – Reducing Leverage

After a good increase in revenue and gain in margins, offset by higher financial expenses and accounting adjustments, Sendas Distribuidora saw a 21% annual drop in net income, to BRL 123 million ($22 million).

Net Income (IR Company)

In my view, the outlook is for maintaining this level of profitability, given that the company may see an increase in operating margins, but until there is a drastic deleveraging, the results will remain stagnant, which corroborates my recommendation to hold the shares.

Valuation – I Don’t Find It Attractive

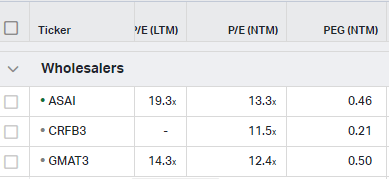

To perform the valuation, I will use the P/E comparative evaluation method with Sendas and its competitors in Brazil, Carrefour Brasil (CRFB3) and Grupo Mateus (GMAT3).

P/E (Koyfin)

By averaging the P/E (NTM), we have a P/E of 12.4x, which implies a downside of 6.7% for Sendas Distribuidora shares. Since the margin of safety is small, I reiterate the recommendation to hold the shares. I would like to point out that Seeking Alpha’s tools already point to another scenario.

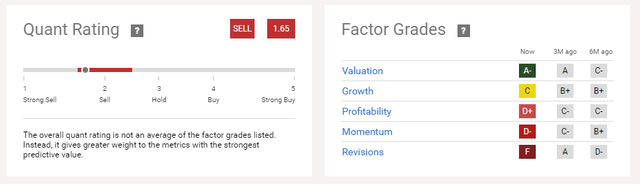

Quant Rating & Factor Grades (Seeking Alpha)

The grade factor points to poor profitability, momentum and revisions. But I will counter my skeptical thesis and Quant Rating’s sell recommendation with the risk chapter below.

Potential Risks To The Bearish Thesis

One fact could completely change my assessment and that of the entire market. In September, there were rumors that Grupo Mateus, which has shares traded on the Brazilian stock exchange, would make a merger offer to Sendas Distribuidora.

It is true that the rumors were denied, but episodes of this type involving the closing of operations have already occurred several times. The merger could begin the consolidation of the sector in Brazil by the player and would also bring a more diversified business model to the new company.

The Bottom Line

Sendas Distribuidora reported mixed results, with ups and downs in 2Q24. Although the expansion strategy is increasing revenues, same-store sales show signs of slowing down.

Likewise, although the company has managed to control costs and expenses well to improve its operating margins, the financial result is still weighed down by strong leverage.

Based on this analysis, I recommend holding Sendas Distribuidora shares. Without further developments from the merger with Grupo Mateus, I believe it is necessary to wait for the company to further deleverage.

Read the full article here