Genesco Inc. (NYSE:GCO), the footwear & apparel retailer, reported its fiscal Q2 results on the 6th of September, sending the stock down nearly -12%. The stock crashed despite a very slightly raised FY2025 outlook and a Q2 earnings beat, with the market seeming to price in a much better performance than Wall Street’s analysts expected.

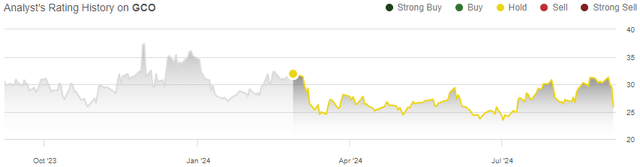

Previously, I published an article on the stock on the 27th of February, titled “Genesco: Focus On Future Margin Trajectory”. Since I initiated the stock at a neutral Hold rating, the stock has now lost -18% of its value compared to S&P 500’s return of 7%.

My Rating History on GCO (Seeking Alpha)

Q2 Report: Weak Comparable Sales, As Expected

Genesco’s Q2 results came in better than Wall Street expected – the revenues of $525.2 million, up 0.4% year-on-year, beat Wall Street’s consensus by $13.0 million. With the relatively good beat in revenues, the GAAP EPS of -$0.83 also beat the consensus estimate by $0.29 as Genesco is heating up for the better H2 seasonality.

Underneath the small sales increase, Genesco’s sales still performed poorly comparably – $20-25 million of the Q2 sales were related to Genesco’s shift in the fiscal year, now pushing back-to-school sales into Q2 instead of Q3. Comparably, Journeys Group revenues declined -1%, Schuh Group’s by -2%, Johnston & Murphy Group’s by -5%, and the Genesco Brands Group’s revenues declined -13% – Genesco’s brands showed underlying weakness across the line with a total comparable retail sales growth of -4% but better e-commerce sales growth of 8%.

Amid a weak US consumer sentiment, some peers have also reported considerable weakness although Genesco’s -4% comparable retail growth does seem to trail other retailers. For example, Shoe Carnival’s (SCVL) Q2 results showed a -2.1% comparable sales decline, still above Genesco’s. J.Jill (JILL) showed a better 1.7% comparable Q2 growth that I wrote about, but the comparable growth still slowed down from 3.1% in the company’s fiscal Q1. Designer Brands (DBI) is only reporting its recent quarterly results on the 11th, and Wall Street expects a 3.0% revenue growth implying an accelerated growth from -2.5% comparable growth in Q1 – while some peers have clearly shown starting weakness as J.Jill also related to weakening traffic from July forward, Genesco’s comparable growth was weak. Wall Street analysts were still expecting worse, though, as Genesco’s relative weakness isn’t very new. Genesco communicated in the Q2 earnings call that Q2 traffic has outpaced the market, but I don’t believe that the traffic trend can be seen in Genesco’s revenues.

With fewer stores pushing SG&A down $4.4 million in Q2, also down 1.0 percentage points as a share of sales, the -$9.5 million operating income (excluding impairments) beat prior year’s -$10.0 operating income slightly despite the lower comparable sales – the profitability improvement was overall good when considering the industry backdrop’s adverse effect on sales. Notably, Genesco Brand Group’s operating income increased $0.8 million year-on-year despite considerably weaker revenues, but Johnston & Murphy Group’s -5% comparable sales decline led to a -$3.1 million decline in the segment’s operating income.

Overall, the quarterly financials were weak, as could already be expected; the Q2 financials beat Wall Street’s weak expectations amid cautious consumer spending. Prior store closedowns seem to have aided profitability even in weaker consumer spending, as the EPS came in well above expectations and with a considerable SG&A decrease.

Genesco’s FY2025 Guidance Is a Positive Sign

The FY2025 guidance remained nearly unchanged, but showing a slight revenue outlook raise. Genesco now expects sales to decline -1% to -2%, being down 0% to -1% comparably when excluding the 53rd week in the company’s fiscal 2024. The sales guidance range was raised by one percentage point with the Q2 report, being a positive boost as Genesco has surprisingly seen accelerating growth trends starting in Q3 contrary to what Urban Outfitters (URBN) and J.Jill have led believe from overall consumer spending, for example discussed in Urban Outfitters’ Q2 earnings call.

The EPS range was kept the same at quite a wide $0.6-1.0 range.

I believe that the slight raise in Genesco’s sales guidance is great, as some retailers have related to deepening weakness from July forward with Genesco’s trends only strengthening – it seems that Genesco is going to have a relatively strong H2 ahead compared to peers, if the positive trend sustains for the rest of the year.

With the new guidance, I believe that the market’s -12% reaction to the Q2 report wasn’t quite justified, also as Wall Street’s expectations for the Q2 financials were beat. Still, the comparable growth is quite worrying.

Do Genesco’s Brands Have Value?

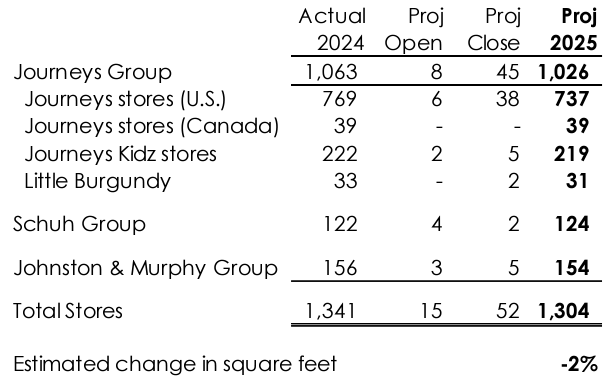

The Q2 comparable sales were clearly affected by weak consumer spending, but Genesco’s brands’ value is still up for debate. The company has continued shrinking its retail footprint, expecting to close 37 additional stores in FY2025 into 1304 total outstanding stores. The retail footprint compares to a total of 1554 outstanding stores at the end of FY2017. Although the store closures clearly improve short-term profitability, store closedowns are fundamentally a weak sign over the long term, as I already previously noted with Genesco’s weakening long-term margin level – fixed costs have to be spread to less average stores, being very negative for the bottom line over the longer term.

Journeys’ Google search volumes, being Genesco’s clearly largest chain, have continued declining over the long term after around 2018. Johnston & Murphy’s Google searches on the other hand have performed more stably in the past five years after a prior decline, but the brand has continued performing poorly with a -5% comparable decline in Q2 – it seems that the company doesn’t likely have a very bright future ahead either, and the Q2 comparable growth underperformance highlighted the existing weakness. While a better H2 seems to be expected, I wouldn’t extrapolate such short signals yet.

GCO Q2/FY25 Investor Presentation

The company also designs and sources footwear under the Levi’s and Dockers brands with the Genesco Brands Group segment, with both brands being owned by Levi Strauss Co (LEVI). Levi’s total sales have also shown quite slow growth, not enabling for very good growth in the segment either – the brands’ health don’t seem to be good, and Genesco’s trailing operating margin of just 0.3% clearly signals such. The store closures are good to improve the retail network’s health, but don’t look to revitalize long-term earnings unless a brand turnaround is achieved.

Updated Valuation

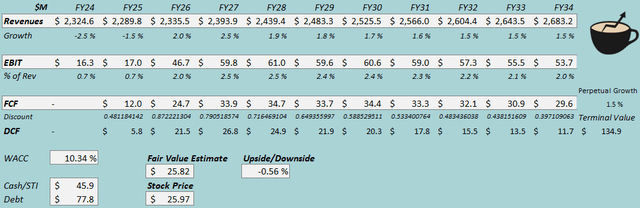

I updated my discounted cash flow [DCF] model quite significantly – with Genesco’s weak comparable sales, I now estimate slower revenue growth; after FY2026 growth of 2.0% and FY2027 growth of 2.5% with a recovery in consumer spending, I estimate Genesco’s revenue growth to slow down into just 1.5% as the weak brand perceptions don’t look to create the foundation for good growth anymore in a baseline scenario.

With the persisting weakness, I estimate the EBIT margin to also slowly fall into 2.0% after a recovery into 2.5% in FY2027 from better consumer spending – the long-term earnings outlook doesn’t stand very good in my opinion.

The cash flow conversion should remain moderate, as even with Genesco’s shrinking store footprint, the company is spending quite a good amount in capital expenditures.

DCF Model (Author’s Calculation)

The estimates put Genesco’s fair value estimate at $25.82, very near the stock price at the time of writing – while I don’t expect a good performance from the company anymore, neither does the market. With the uncertain future regarding Genesco’s margins, the investment case is still very volatile with the potential for significant losses if the retailer continues underperforming, or gains if Genesco can turn around its weakly performing brands’ perceptions. With an unlikely operating margin like Shoe Carnival’s trailing 8.2%, the stock could have immense upside.

The fair value estimate is down from $35.46 previously as I slashed my growth and margin estimates in the baseline scenario.

CAPM

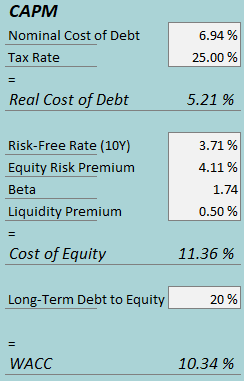

A weighted average cost of capital of 10.34% is used in the DCF model, down from 12.90% previously. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q2, Genesco had $1.3 million in interest expenses, making the company’s interest rate 6.94% with the current amount of interest-bearing debt. With Genesco’s recent debt paydowns, I now only estimate a 20% long-term debt-to-equity ratio.

To estimate the cost of equity, I use the 10-year bond yield of 3.71% as the risk-free rate. The equity risk premium of 4.11% is Professor Aswath Damodaran’s estimate for the US, updated in July. Seeking Alpha now estimates Genesco’s beta at 1.74. With a liquidity premium of 0.5%, the cost of equity stands at 11.36% and the WACC at 10.34%.

Takeaway

Genesco’s Q2 results beat Wall Street’s expectations, but underperformed against the market’s expectations as the stock took a -12% hit. Comparable sales were clearly affected by weaker consumer spending across the industry, but Genesco’s growth seemed to come below peers’ at a noticeable level. The company has seen positive trends going into Q3, against other retailers’ remarks of weak July and August traffic, but the improvement is too short to extrapolate longer-term conclusions from as Genesco’s brand perception still seems weak.

The stock’s valuation already prices in weak estimates that I believe to be fair – with a likely volatile investment case, depending on longer-term comparable sales improvements and their margin impact, I remain with a Hold rating for Genesco but suggest caution.

Read the full article here