KKR Real Estate Finance (NYSE:KREF) has seen its commons and preferreds (NYSE:KREF.PR.A) recover substantially from lows over the last few months since I last covered the mortgage REIT’s portfolio. The preferreds are now trading for 84.6 cents on the dollar, a roughly 15.4% discount to their $25 per share liquidation value, and offer a 7.7% yield on cost against their $1.625 per share annual coupon. This discount should be closer to 90% as pending Fed rate cuts look set to catalyze broad yield compression for fixed-income securities. KREF generated fiscal 2024 second-quarter revenue of $47.65 million, a dip of roughly 6.4% year-over-year but a huge beat on consensus by $10.12 million.

KKR Real Estate Finance Fiscal 2024 Second Quarter Supplemental

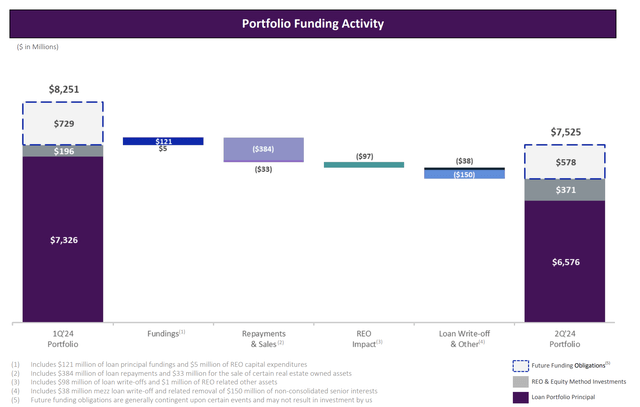

The revenue dip was led by a reduction in KREF’s total portfolio to $6.95 billion, down sequentially from $7.52 billion in the first quarter as repayments continue to lead new loan originations. KREF funded $121 million in new loans during the quarter, a $296 million difference to repayments and sales of $417 million. Non-GAAP EPS was negative at $1.57 but beat consensus by 14 cents. Distributable earnings before realized losses on loan write-offs at $28 million, around $0.40 per share, were up sequentially by 1 cent. Repayments have now exceeded originations in four of the last five quarters, highlighting a defensive strategy mirrored by other mREITs dealing with the intense disruption and risk spike stemming from the Fed’s more than two-year fight with inflation.

KKR Real Estate Finance Fiscal 2024 Second Quarter Supplemental

Originations, Repayments, And Book Value

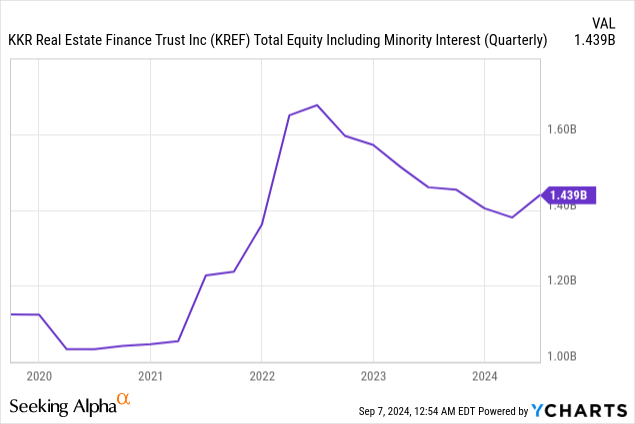

KREF last declared a quarterly cash dividend of $0.25 per share, the same as the prior quarter, and $1 per share annualized for an 8.2% dividend yield on the common shares. Distributable earnings cover this payout by 160%, helping boost the mREIT’s overall liquidity and book value. Book value per share was $15.24 at the end of the second quarter, a growth of 6 cents sequentially as CECL allowance dipped to $1.65 per share from $3.54 per share. Total equity at $1.44 billion was also up sequentially, reversing a downtrend in place since the summer of 2022 and setting KREF up to begin the process of closing the current 20.28% discount to book value on the commons.

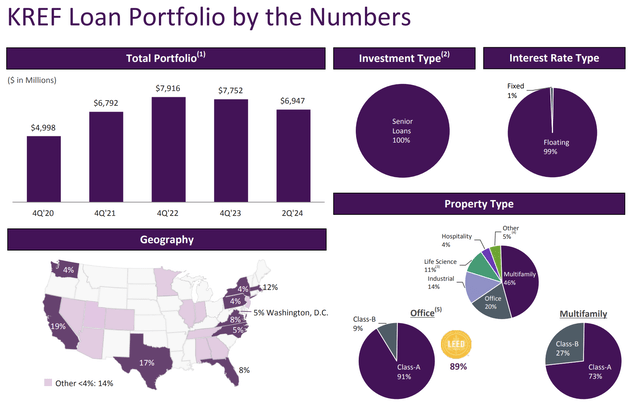

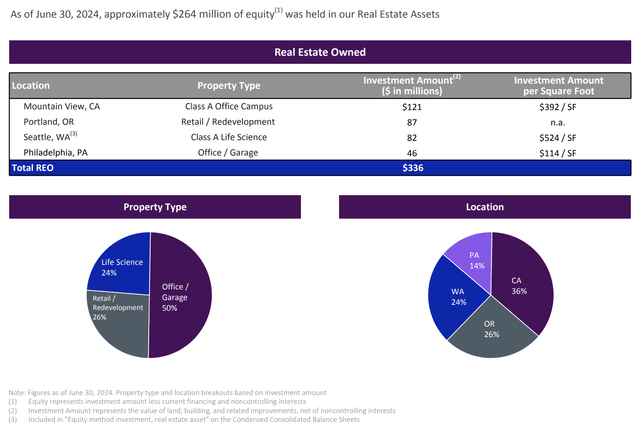

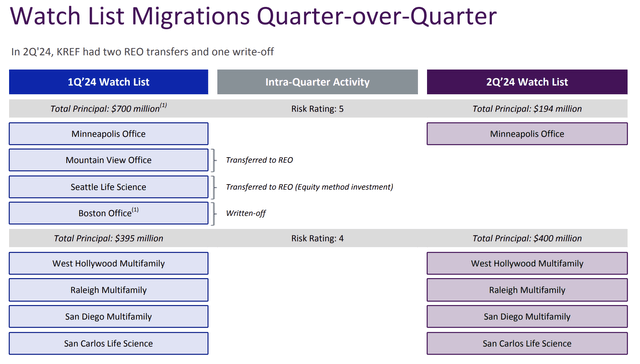

KREF’s portfolio is predominantly senior loans which means the mREIT can manage risk by taking possession of underlying collateral. This meant real estate owned of $336 million at the end of the second quarter, a figure that was 50% comprised of office properties and 24% and 26% split between life science and retail properties respectively. The mREIT sold a portion of the Philadelphia office real estate owned during the quarter as two watch-list loans were transitioned to real estate owned.

KKR Real Estate Finance Fiscal 2024 Second Quarter Supplemental

Watch-list loans transferred to real estate owned were a Mountain View Office and a Seattle Life Science building, with the number of watchlist loans at the end of the second quarter a single Minneapolis office loan with a total principal of $194 million. KREF had four loans with a risk rating of 4 as of the end of the second quarter, mainly comprised of Multifamily properties with the weighted average risk rating on the portfolio improving to 3.1 from 3.2 sequentially.

KKR Real Estate Finance Fiscal 2024 Second Quarter Supplemental

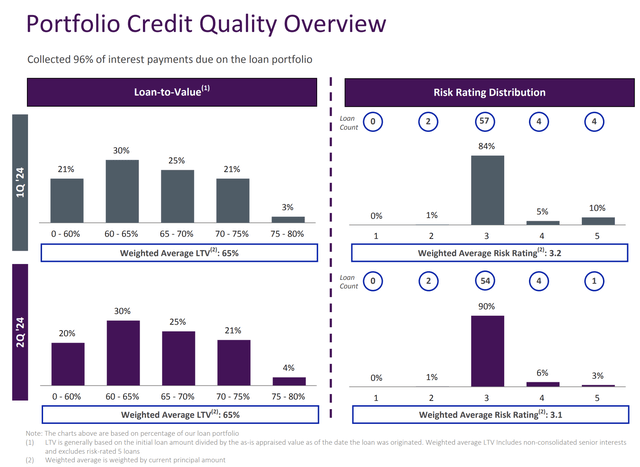

Risks And Portfolio Credit Quality

KREF had over 90% of its portfolio risk rated 3 or better, an improvement from roughly 85% in the first quarter. The mREIT’s weighted average loan-to-value ratio was constant sequentially with its weighted average unlevered all-in yield of 8.9% at the end of the second quarter staying constant sequentially.

KKR Real Estate Finance Fiscal 2024 Second Quarter Supplemental

I like that multifamily and industrial assets form 60% of the loan portfolio with the asset class less privy to headwinds from changes to the way of work. While office properties in certain urban markets like Manhattan will be expected to recover against a better backdrop of constrained supply, the national vacancy rates continue to rise with the date for stabilization still uncertain even as rate cuts look set to deliver broad relief to debtors.

KKR Real Estate Finance Fiscal 2024 Second Quarter Supplemental

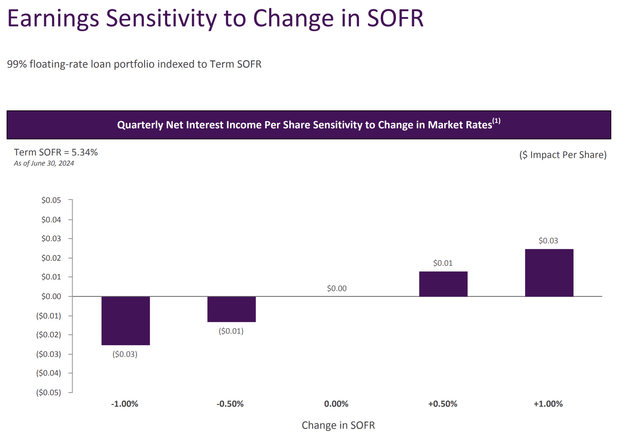

Critically, a reduction in the Fed funds rate will have a minor dampening impact on short-term profitability. KREF expects that for every 50 basis point cut in the Fed funds rate, its quarterly net interest income per share will dip by 1 cent. However, the dampening effect of rate cuts on earnings will be somewhat mitigated by the recovery of origination volume. This is as rate cuts would form a relief to debtors who have faced elevated interest payments for two years.

KKR Real Estate Finance Fiscal 2024 Second Quarter Supplemental

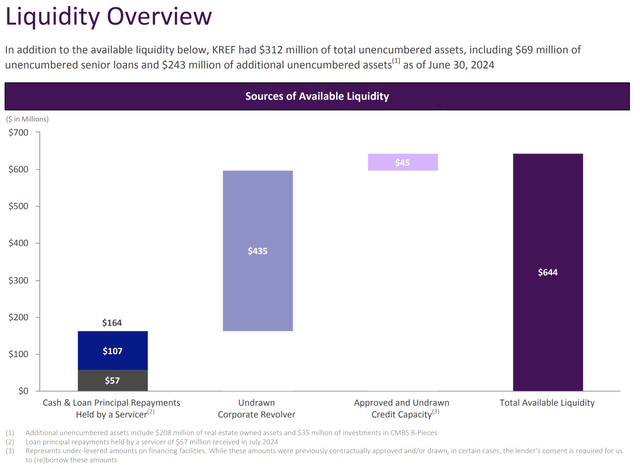

KREF held total liquidity of $644 million at the end of the second quarter, up from the first quarter with the mREIT also having $2.8 billion of undrawn capacity from its financing. KREF also has $312 million of total unencumbered assets, with $208 million of this total formed from real estate owned. These assets will be monetized when the time comes, with lower interest rates likely to see a recovery of their value. KREF has steered its portfolio to book value growth and now faces a positive sentiment change from rate cuts. I continue to add to my position in the preferreds through DRIP as the commons now also a buy.

Read the full article here