Amid renewed turmoil across retail supply chains and in broader markets, the case to own leading fashion retailer Industria de Diseño Textil, S.A. (OTCPK:IDEXY) (OTCPK:IDEXF) or ‘Inditex’, backed by its presence across multiple channels and store formats (Zara, Massimo Dutti, Pull & Bear, etc.), remains as compelling as ever (see Inditex: No Stopping The World’s Premier Fast Fashion Compounder). There’s also solid momentum heading into next week’s Q2 report – if the company’s trading update and trends across the broader consumer space are any indications.

Even if the company does disappoint near-term, investors can always fall back on Inditex’s attractive longer-term positioning, which ticks all the right boxes from logistics, space utilization, and omnichannel growth. The only catch is the pricing, which, at >20x ex-cash earnings, isn’t the cheapest it’s ever been.

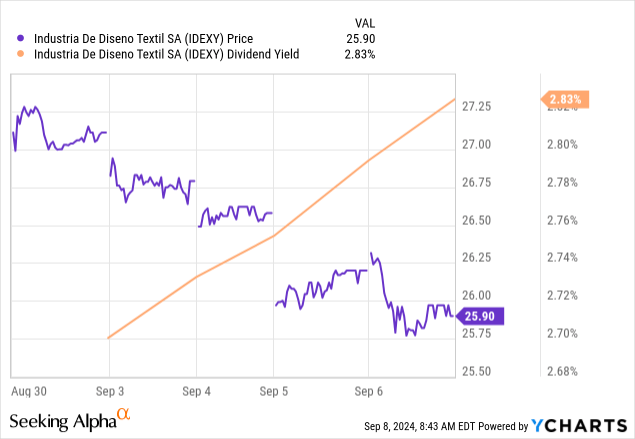

But this week’s selloff helps, as do the underlying growth and quality of cash flow generation here, as well as Inditex’s ‘safe-haven’ qualities, all of which support the case for more upside. Plus, with the Fed finally kickstarting its rate cut cycle, Inditex’s ~3% dividend yield, backed by a growing net cash balance, presents an increasingly attractive bonus for investors willing to sit and wait.

A Possible Headline Deceleration in Q2…

Fundamentally, there’s never too much to fault with Inditex, and that remains the case heading into this week’s quarterly print. Expect another strong P&L and cash generation update overall, helped by the company’s highly efficient business model. Where Inditex could disappoint slightly, though, is on the top line.

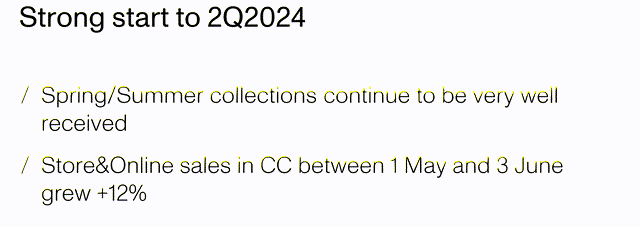

Yes, management disclosed +12% YoY headline growth from the start of May through early June (per last quarter’s trading update). But bear in mind that the company will also be going up against a very high YoY base (recall Q2 2023 saw +18% YoY growth) and a few percentage points of currency headwinds (in line with Q1).

Inditex

…but Look to the Underlying Rate of Change

By market, Inditex remains levered to the European consumer; more so after its Russian exit. The good news on this front is that high-frequency retail data from Southern Europe (mixed but slightly improving in Spain), Northern Europe (improving in Sweden), and Western Europe (improving in the U.K.) suggest a net positive direction of travel.

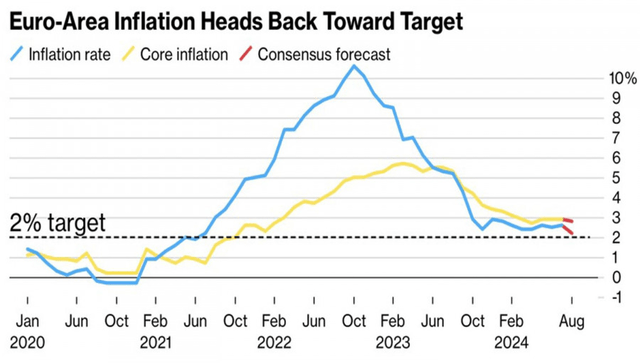

Perhaps even more importantly, Europe appears to be well past its inflationary ‘peak’ – good news for disposable income through the rest of the year. Similarly, forward-looking consumer sentiment indicators are on a clear recovery path, supporting the case for further retail spending upside from here.

FX.co

Beyond Europe, the U.S. is the key growth market. Here, penetration is relatively low but growing – a testament to Inditex’s brand appeal. And as Inditex further builds out its U.S. presence, it likely has a lot of runway for outgrowth in a market that, per guidance updates from peers like Abercrombie & Fitch (ANF) and Gap (GAP), is trending quite positively.

Also worth watching in Q2 is Inditex’s ‘omnichannel’ progress, particularly in China, a market Inditex has been penetrating via online livestreams since last year. While small, getting ‘omnichannel’ right in China and other previously untapped markets could mean higher margin income streams down the line; thus, progress here will also be a key Q2 monitorable with regard to the longer-term growth runway.

…and Mid to Long-Term Growth Targets

To some extent, the customary quarter-to-date trading update will give investors some idea of whether Inditex is on the right track for this year. For longer-term investors, though, management’s commentary on its growth initiatives will perhaps be an even more important gauge.

Top of mind is the target to add +5%/year of gross new space through 2026 – an initiative that, if utilized efficiently alongside ongoing store refurbishments, should boost revenue growth. Also in the pipeline are efforts to further improve stock management efficiency across the store base (building on the prior success of inventory tracking via ‘RFID’ and integrated stock management via ‘SINT’). Of course, growth will come at a cost and there’s always risk of overruns. Hence, tracking management’s EUR900m/year capex guidance (through 2024/2025) will be just as important a monitorable on this week’s Q2 call.

…also for Margin Resilience to Shine Through

Inditex has always been a retail ‘safe haven’ in times of turmoil (note its outperformance through the logistical disruptions of COVID, Russia-Ukraine, and, more recently, the Red Sea), so more supply chain headwinds should play into its hands. This time around, it’s turbulence in Bangladesh, a key part of most retail supply chains, after ex-Prime Minister Sheik Hasina abruptly fled the country amid political unrest.

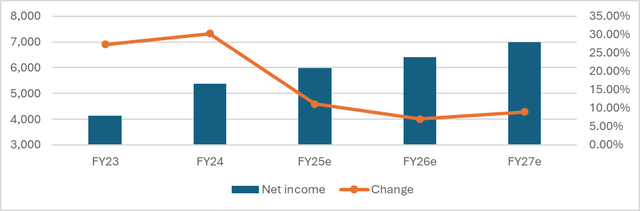

Unlike many of its peers that will be forced into diverting orders to Southeast Asia in response, the fact that Inditex designs and produced merchandise in proximity to its Spanish base means it will again be relatively insulated here. P&L-wise, this means better gross margins, inventory management, and potentially even some market share gains in the coming months. So as long as Inditex keeps a handle on operating expenses, there’s a good chance we see a beat-and-raise coming – particularly with Street forward earnings growth estimates not all that demanding in the ~11% range.

S&P via Market Screener

Final Note on Risks & Summing Up

To be clear, Inditex isn’t devoid of downside risks. Some of these I’ve highlighted above (e.g., slower Q2 sales growth and higher capex to fund long-term growth targets). There are also risks that could re-emerge; for instance, competition from the Chinese fast fashion upstarts, though the fact that Inditex has thrived through Shein’s disruptive growth is testament to its moat.

Still, the stock has also traded down into this week’s earnings – likely in reaction to some of these near-term risks. This is ‘good’ news, in my view, in that it keeps the bar relatively low; so even with some of the positives also reflected in the higher ex-cash P/E, there’s plenty of space for the company to grow into its valuation over time. In the interim, investors get paid more than ever to sit and wait.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here