Golub Capital BDC (NASDAQ:GBDC) recently completed its merger with Golub Capital 3 BDC which has led to a much bigger market portfolio value for the BDC. Golub Capital’s net investment income outstripped its dividend by a good margin in the second quarter, leading to a safe 12% yield for income investors. Golub Capital also convinces in terms of non-accrual percentage which, despite edging up post-merger, the longer term trend is very much favorable. I also like that Golub Capital’s shares have fallen below net asset value lately which likely has something to do with the broader sell-off in the BDC sector lately. I believe the drop is a buying opportunity for Golub Capital and the risk profile for income investors is skewed to the upside!

Previous rating

I rated shares of Golub Capital a buy in June — 11% Yield And Upside Related To Merger Transaction — as the BDC had a catalyst relating to the merger with Golub Capital 3 BDC. Golub Capital’s merger was set to lead to transaction synergies and to create a much larger, more diversified BDC for investors to draw income from. Golub Capital’s portfolio value increased significantly following the merger and the BDC generated a ton of net investment income while maintaining good balance sheet quality.

Merger completion and portfolio growth

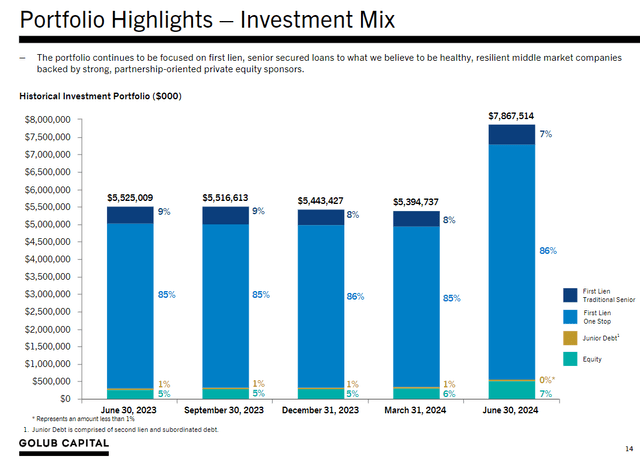

The merger with Golub Capital 3 BDC caused the BDC’s portfolio value to increase drastically in the second-quarter. The increase in the portfolio value to $7.87B (+46% Q/Q) was almost exclusively driven due to the merger between the two BDCs and is not the result of a major boost to the BDC’s originations. As in the past, Golub Capital’s portfolio includes mainly first liens so a major change to the portfolio structure post-merger did not occur.

Golub Capital

Golub Capital’s non-accrual percentage, after the close of the merger, deteriorated slightly, but not by a lot. The BDC’s non-accrual percentage, which shows the amount of troublesome and non-performing loans in its portfolio, was 1.0% (based off of fair value) as of the end of the June quarter. While the non-accrual percentage increased 0.1 PP quarter-over-quarter, Golub Capital’s non-accrual trend over the last year, however, is positive and indicates a material improvement in asset quality ahead of the merger.

| $M | Q2’23 | Q3’23 | Q4’23 | Q1’24 | Q2’24 |

| Total Investments | $5,525.0 | $5,516.6 | $5,443.4 | $5,394.7 | $7,867.5 |

| Non-Accrual (at cost) | 1.8% | 1.6% | 1.7% | 1.5% | 1.6% |

| Non-Accrual (at fair value) | 1.5% | 1.2% | 1.1% | 0.9% | 1.0% |

(Source: Author)

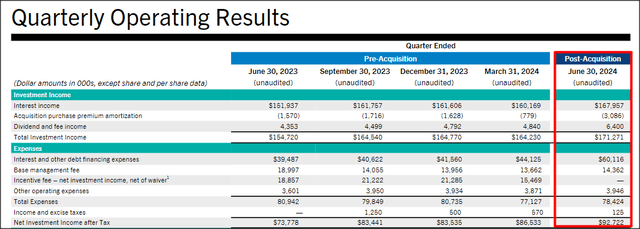

Golub Capital generated $92.7M in net investment income (after tax) in Q2’24, showing 26% year-over-year growth. The increase in net investment income is due to the BDC combined its portfolio with its acquisition target, so investors should not expect a continuation of the current NII trend. Golub Capital did, however, guide for transaction synergies, including a reduction in its incentive fees on income and capital gains.

Golub Capital

The distribution coverage profile looked as healthy as ever for Golub Capital, with the BDC generating 1.18X coverage compared to 1.31X in Q1’24. I calculate the dividend coverage ratio by dividing the company’s net investment income by GBDC’s $0.39 per-share regular dividend only. However, investors should note that Golub Capital pays supplementary dividends, which amounted to $0.11 per-share in the last quarter. As a result, shares of Golub Capital yield 12%, and not 11% (which is the yield calculated based solely off of the regular dividend).

Golub Capital Is A Bargain

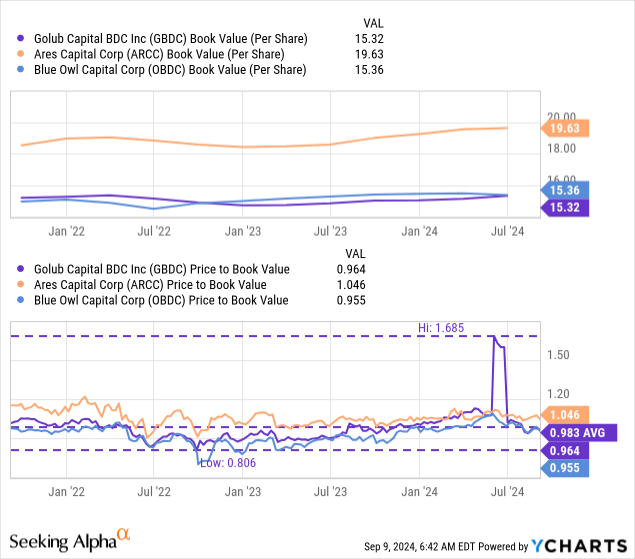

After the acquisition of Golub Capital 3 BDC, the combination of asset values also led to an increase in net asset value: in Q2’24, Golub Capital’s BDC totaled $15.32/share compared to a pre-acquisition net asset value of $15.12/share.

Income investors can currently get a 4% discount to net asset value, which is due to BDCs selling off in expectation of the Federal Reserve cutting the federal fund rate. A positive inflation report for July — which showed an inflation rate of only 2.9% — and a weak reading of the employment report last week all but guarantee a Federal Fund rate cut later this month. Rate cuts are typically perceived as a negative event for BDCs, especially those that have invested funds into variable rate-paying debt.

I believe Golub Capital could trade at a P/NAV ratio of 1.1X given its low non-accrual percentage and considerable excess dividend coverage. A 10% premium to net asset value implies a fair value in the neighborhood of $16.85 per-share and could be achieved in case the BDC captures synergy potential related to its merger with Golub Capital 3 BDC.

Risks with Golub Capital

As things stand now, I don’t see any issues with the non-accrual percentage or with the BDC’s NII performance. Golub Capital’s dividend coverage profile strongly supports the regular dividend and the company is lowering its fees, which is set to be a positive catalyst for NII growth. What would change my mind about Golub Capital is if the BDC saw a higher non-performing loan ratio or if the BDC failed to earn sufficient net investment income.

Closing thoughts

Golub Capital just completed its merger with Golub Capital 3 BDC and the investment firm has seen a material increase in its portfolio value as well as its net investment income. Golub Capital also supported its dividend well with net investment income in Q2’24 and is set to capture merger synergies, which should further improve the company’s dividend coverage profile.

Golub Capital’s non-accrual percentage increased slightly in the last quarter, but the longer term (1-year) trend in non-performing loans is actually quite positive: the non-accrual percentage decreased by approximately 33% in the last year. Further, due to the sell-off in the BDC industry in recent weeks, shares of Golub Capital are now priced below net asset value, leading to an improved risk profile as well as a higher yield for income investors.

Read the full article here