A Diversified Financial Firm Currently On A Dip

One financial-sector stock has been on my watchlist for over a year now and since it has recently taken a price dip despite being profitable and having positive future EPS estimates, today’s article takes another look at it more closely.

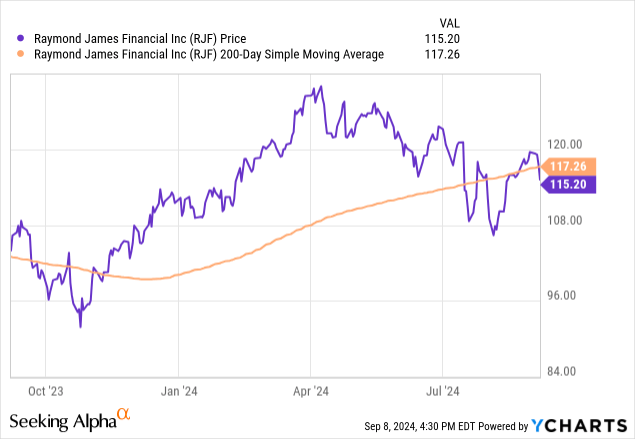

As the YCharts above shows, the stock is currently trading nearly 2% below its 200-day SMA and having had a series of dips this summer.

I first covered Raymond James Financial (NYSE:RJF) in my June 2023 article when I called it a buy, and since my bullish call it has gone from $99.20 to $115, a +16% gain. At the time of my bullish call, some points I liked about this firm were positive client inflows, a diversified business model, and stable dividend income.

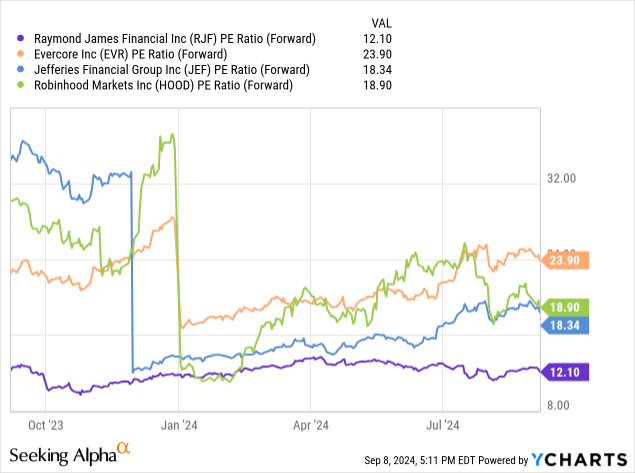

SA lists some of its peers as Jefferies Financial (JEF), Robinhood Markets (HOOD), and Evercore (EVR), so those will be my 3 comparable stocks today.

As far as what the firm does, in the words of their official site, it includes the following:

Serve client accounts through approximately 8,800 financial advisors in the United States, Canada and overseas.

The company has expanded through the years to serve corporations, institutions and municipalities through significant capital markets, banking and asset management services.

This firm also serves the investment banking and M&A space; however, it is in a very competitive sector with huge players.

In fact, according to data from Statista, RayJay is not among the top investment banks. The data goes on to say:

JPMorgan (JPM) was the leading investment bank globally as of June 2024 in terms of market share of revenue. Between January and June 2024, JPMorgan’s revenue accounted for 9.2 percent of the global investment banking revenue. Goldman Sachs (GS) followed, with a market share of 7.3 percent.

To kick off this analysis, we will first look at where the market is currently valuing this stock, in the next section.

A Low Valuation Among Peers

From market momentum data on SA, Raymond James has actually been underperforming the S&P500 since about spring.

What the following graphic tells us is that on a forward P/E basis, the market is undervaluing this stock vs. these 3 peers I selected.

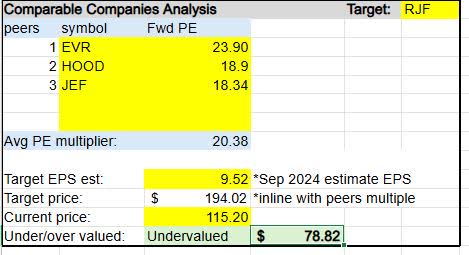

In fact, if you look at the comparable analysis I created below, using the above forward P/E ratios and this stock’s EPS estimates, Raymond James is undervalued by around $79 right now, since a price in line with its peer average multiple would put it at a share price of $194.

RayJay – comps analysis (author work)

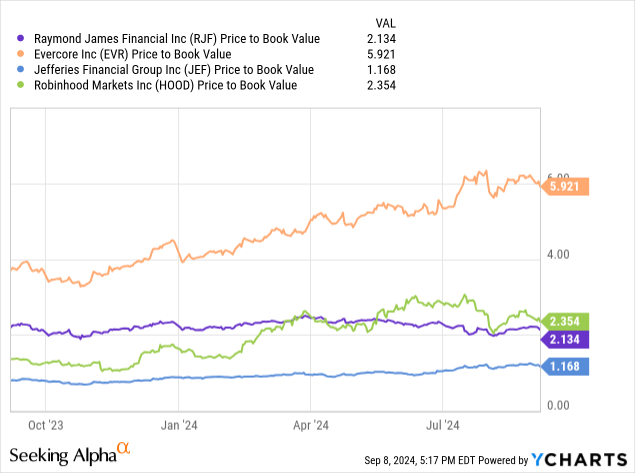

Besides forward price-to-earnings, since this firm has a considerable about of assets on its balance sheet, and in fact holds $8.8B worth of investments in debt and equity securities, here is a look at their price-to-book value (P/B) compared to peers:

What this data tells me is that Raymond James is near the bottom of this peer group in terms of P/B ratio.

To help better understand what could be driving these lower valuations, and lower market momentum, let’s take a closer look at recent earnings performance and future potential growth in the next section.

Past Earnings Impressive While Future Shows Positive Signs

What we can gather from the most recent earnings reported on July 24th for fiscal Q3 of 2024, as its next one is not until late October, is that quarter-ending June earnings were up 33% YoY.

One clear driver of this was YoY revenue growth, according to the income statement, and although net interest income saw a YoY decline due to a spike in interest expenses, it was offset by revenue from the firm’s other businesses such as trading, asset management, underwriting/investment banking, and brokerage commissions. In fact, the firm pulled in $1.6B that quarter just from asset management fees alone.

This data also supports my claim that the firm has a diversified business model, which I find valuable since it is not fully reliant on just one revenue driver.

More importantly for my readers, however, is where I think this firm is going a year from now. In this type of business, which has a huge fee-driven component, I am looking for current growth in new clients, inflows, new loans made, and assets under management, for example, as they contribute to future revenue flows.

The firm’s July earnings release describes growth in some of those components that contribute to future fees revenue:

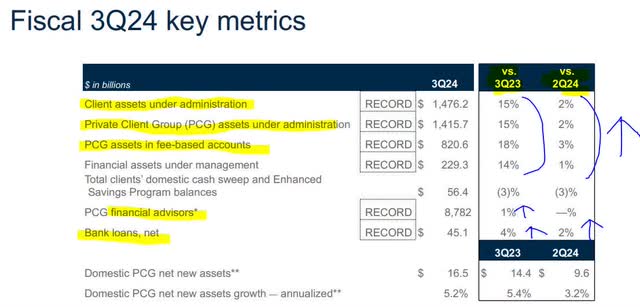

Record client assets under administration of $1.48 trillion and record Private Client Group assets in fee-based accounts of $820.6 billion, up 15% and 18%, respectively, over June 2023.

The below graphic from their July presentation also gives a nice look at how the firm has grown assets under administration (AUA) but also loans which can drive interest income. As a firm with a substantial number of financial advisors, as mentioned in the intro, growth in new advisors I think could mean bringing in new client monies into the firm, driving future fees and helping future earnings, which could boost the share price if investors become bullish again.

RJF – growth metrics (RJF quarterly presentation)

In terms of their capital markets business, it should be noted that it has had mixed results, but the CEO in his remarks struck a positive tone about the firm’s mergers & acquisitions (M&A) pipeline, which, I think, could help future fees earned:

Investment banking revenues increased slightly from the preceding quarter driven by higher debt and equity underwriting revenues, whereas M&A revenues declined,” said Reilly. “We continue to be optimistic about our healthy M&A pipeline and new business activity; however, timing of closings remains difficult to predict.

In terms of the M&A segment, a May article from global bank Barclay’s struck a positive tone about the potential for this business segment this year, which, I think, could benefit firms like Raymond James and its M&A business, despite it having very large competitors like Goldman and JPMorgan.

Following a slow market in 2023, M&A volumes are set to increase as sponsors become more active while corporates continue to leverage their healthy balance sheets in search of strategic transactions. With growing expectations of rate cuts and a soft landing in the US and healthy pressure from activists, 2024 could shape up to be a solid year for the market, according to our Global M&A team.

What other analysts are saying about Raymond James in terms of future EPS estimates are also positive, with YoY EPS growth projected for the fiscal 2024 year ending September as well as growth in 2025. In fact, there have been 7 upward revisions vs. 6 downward revisions.

This positive earnings picture I am painting sets up a nice scenario for sustainability and growth of dividend payments, which I will talk about next.

A Proven Dividend Grower Among Peers

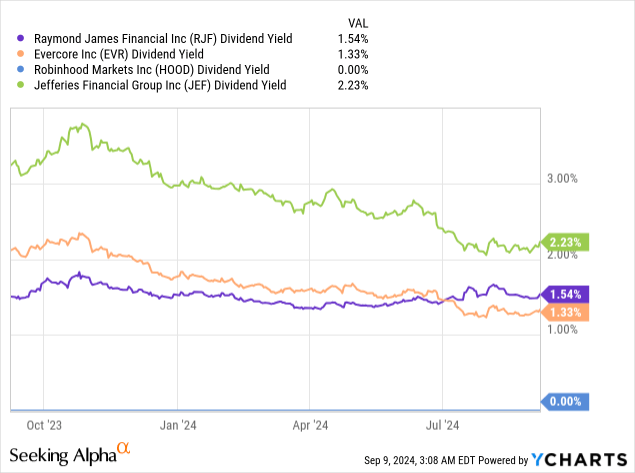

Here is what we know about this firm’s dividend yield vs. its 3 peers I selected:

This data puts Raymond James somewhere in the middle of this peer group with a yield of 1.54%, so not anything terrible or exceptional either.

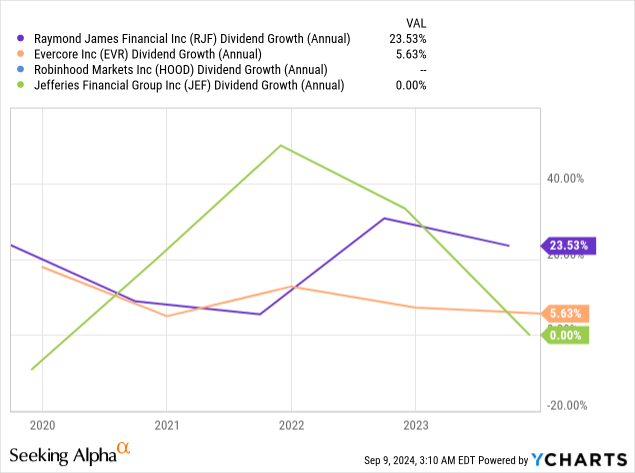

Further, evidence shows Raymond James exceeds this peer group in terms of proven annual dividend growth in the last 5 years, which the YCharts below shows, and further adds to my confidence about their ability to pay out dividends:

So, this firm has a proven track record of dividend sustainability and growth, and I think if those future EPS estimates materialize it will add to the likelihood of further dividend stability and growth in a year. This is especially relevant to investors who are building a dividend-income portfolio and want to add this stock to their basket of dividend stocks, with a goal of future dividend growth of course that is sustainable.

Risk Profile Impacted By Recent Downgrade But Otherwise Positive

Although I have shown the firm has seen YoY profitability growth, top-line growth and potential for future earnings growth, I think the key driver of the undervaluation on this stock by investors is the downgrade this summer by Wolfe Research, who reduced its rating to Peer Perform from Outperform.

In a news desk article from global financial portal Investing.com, here is why they were downgraded:

Despite the company’s strong performance, Wolfe Research anticipates a slowdown in earnings per share EPS growth relative to its peers. Factors contributing to this outlook include sensitivity to short-term interest rates, emerging net new asset (NNA) challenges, and shifts within the company’s operational structure. Additionally, the firm may face increased compensation expenses and has less exposure to capital markets activities, which could affect its growth prospects.

The risk I think downgrades like this pose is that they will push investors away from this stock in the short term, hence the slower market momentum and undervaluation I described, which could impact existing shareholders that bought at an earlier, higher price.

However, this price dip scenario also presents a buying opportunity in my opinion for new investors, taking advantage of the dip below the 200-day SMA.

Consider the otherwise positive risk profile of this firm in terms of having a leverage ratio well above regulatory minimums, according to its last quarterly presentation:

RJF – leverage ratio (company presentation)

In addition, since this firm has a banking component that “lends” money, another risk to consider is holding on to bad loans. The company struck a positive tone in that regard, in its last quarterly release:

The credit quality of the loan portfolio remains solid, with criticized loans as a percent of total loans held for investment ending the quarter at 1.15%, down from 1.21% in the preceding quarter. Bank loan allowance for credit losses as a percent of total loans held for investment was 1.00%, and bank loan allowance for credit losses on corporate loans as a percent of corporate loans held for investment was 2.00%.

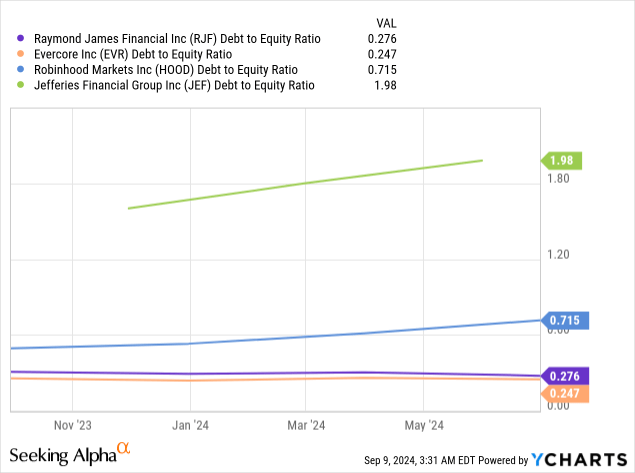

Also, I would highlight that RJF has a relatively low debt-to-equity ratio at just 0.27, aligned with most of this selected peer group, with Jefferies being an outlier:

The evidence shows that despite the modest downgrade from Wolfe, which had more to do with future growth projections than to do with liquidity or balance sheet risks, it seems this firm has a relatively acceptable risk profile in my opinion.

Another risk factor to consider is the breakdown of this firm’s interest-earning assets, and the following section goes into that briefly, particularly exposure to commercial real estate loans.

A Diverse Interest-Earning Portfolio With Some CRE Exposure

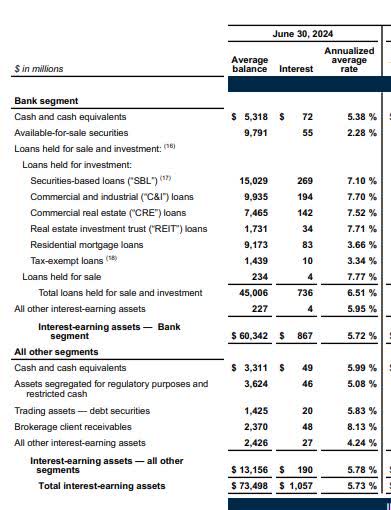

According to the company’s last earnings report, here is an overview of the interest-earning assets this firm holds and how they break down:

RJF – interest earning assets (company data)

Some items I am concerned about are the overexposure to commercial real estate, for example, or lack of diversification. In the above data, we can see that CRE loans they hold ($7.4B) make up 16.5% of total loans held for sale and investment($45B), and 10% of total interest-earning assets ($73.5B).

I point out CRE exposure since a July article in the Harvard Business Review pointed out that US banks will face $1T in CRE loans coming due in the next few years.

The article goes on to say:

The risks of U.S. commercial banks being overexposed to CRE have intensified as the global pandemic upended long-held economic assumptions: perpetually subdued inflation, low interest rates, and in-office work.

With this risk exposure to CRE at RJF, that brings us to the final question: is it a potential buy right now at this below-average price? Continue reading as I give my “clinical impression” next.

Positives Outweigh Negatives

To bring together the key points we talked about today, it appears the positives of this firm include:

Recent growth both on the top and bottom lines, a diversified business mix, positive sentiment from the analyst consensus and indicators that future fees-driven revenue could grow from current growth in AUA. In addition, it appears to have an acceptable risk profile in terms of debt-to-equity, and losses from bad loans.

At the same time, overshadowing this firm is the downgrade this summer from Wolfe Research, the potential for lower future interest income if predictions of Fed rate cuts by CME Fedwatch end up materializing, and questions on will this firm benefit enough if M&A activity continues growing, considering that it competes with several large firms for such business. In addition, although CRE loan exposure is just 16% of its loan book, it remains an area of concern to keep an eye on as it is a topic of concern to many banks in the last year.

Where I think this firm has its competitive edge will be in the financial advisor space and managing assets, which has proven to be a major driver for this firm. In fact, the income statement data on SA clearly shows asset management fees are nearly 50% of total revenue at RJF.

It is more than well capitalized right now, I think, to withstand some short-term shocks if it does see some pain on CRE loans, particularly since it made no mention of any significantly high loan losses in its last earnings result.

Keep in mind, making real estate loans is not this firm’s primary business, as with some regional banks, but it is essentially a wealth advisor/asset manager with a banking component.

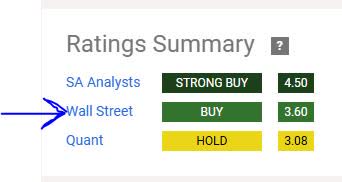

Therefore, my overall clinical impression is that it is a buy, reaffirming my original sentiment on this stock back in June 2023 and siding with the Wall Street bulls. I think it is an undervaluation opportunity, and that the market is unjustifiably undervaluing it, mostly because of the summer downgrade.

RJF – rating (SA)

Read the full article here