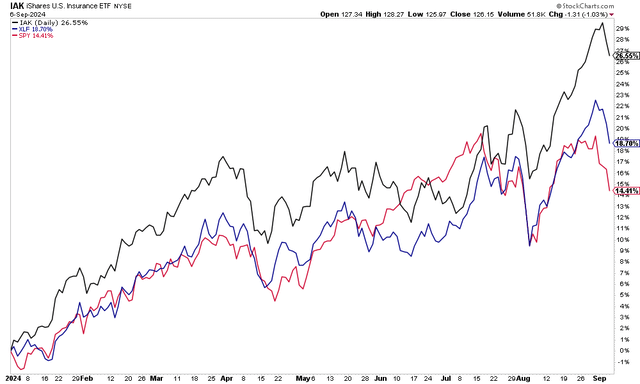

Insurance equities have been one of the leading areas of the US stock market so far this year. The iShares US Insurance ETF (IAK) is higher by 27% even after a modest pullback to begin September, outpacing the S&P 500 by more than 12 percentage points.

More broadly, Financials stocks, as measured by the SPDR Financials Select Sector ETF (XLF) have been a second-half winner as the growth trade has taken a backseat to value. Digging into the insurance slice of Financials, I had a buy rating in Q2 2023 on The Hartford Financial Services Group (NYSE:HIG).

Back then, the Property & Casualty Insurance company sported a price-to-earnings ratio of about 9, below its peers, and at a significant discount to its long-term average. Today, after a more than 60% rally since April last year, the earnings story has been strong and is still healthy. HIG features a 9.9x P/E when using 2025 EPS estimates and its technical situation is healthy. I reiterate a buy.

Insurance Stocks Soar in 2024

Stockcharts.com

Back in July, HIG reported a mixed set of quarterly results. Q2 non-GAAP EPS of $2.50 beat the Wall Street consensus target of $2.25 while revenue of $6.5 billion, up 7% from the same period a year earlier, was a material $70 million miss.

Digging into the quarter, the Connecticut-based $34 billion company posted a net income ROE of 19.8% with core earnings ROE of 17.4%. Its P&C written premiums jumped 12% in the quarter, helped by low-mid-teens percentage growth in its Commercial Lines and Personal Lines segments. The stock rose by more than 7% that followed the release.

For shareholders, HIG’s dividend yield of 1.64% is nothing to write home about, but the firm’s management team authorized a new $3.3 billion stock buyback plan, effective from August 1st of this year through the end of 2026. These shareholder accretive activities should be viewed quite favorably in light of HIG’s low valuation.

Key risks include softer premium growth in the quarters ahead amid a weaker economy. HIG could also have a tough time keeping its margins up if demand for insurance wanes or if competitors enter the group benefits business. Also, natural disaster risk may be higher than average right now given the number of billion-dollar disasters in the past 12 months, and extremely high home insurance rates could draw the ire of politicians.

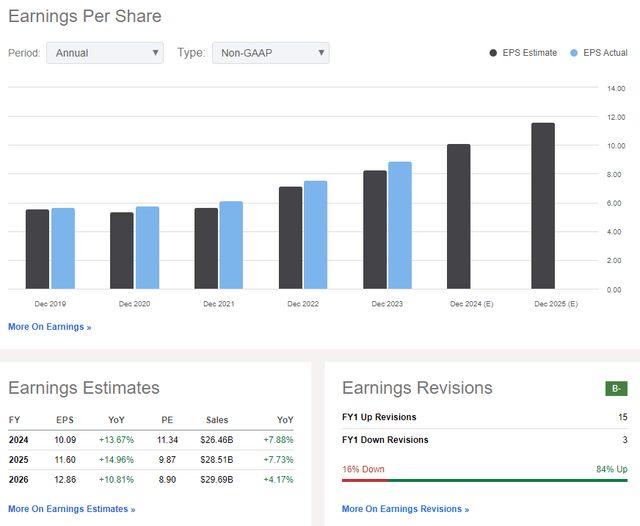

On the earnings outlook, analysts expect non-GAAP EPS to rise at a steady and high rate now through 2026. Current year EPS is likely to verify slightly above $10 while out-year EPS is seen accelerating to $11.60, but even by 2026, the bottom-line growth rate is high, above 10%. Thus, a higher-than-average earnings multiple is warranted in my view. HIG’s revenue is seen increasing in a low-to-mid single-digit range too.

The Hartford: Revenue, Earnings, Revisions Trends

Seeking Alpha

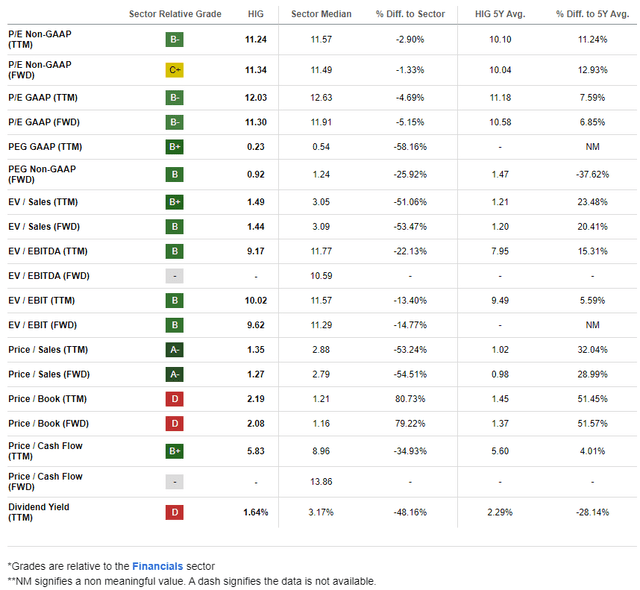

On valuation, if we assume $11 of normalized forward non-GAAP EPS over the coming 12 months and assume a 12x P/E, slightly above its long-term average of 10.6 due to the high and steady growth rate, then shares should trade near $132.

HIG also trades to the cheap side from a price-to-sales perspective versus the sector median, though it is somewhat expensive when analyzing the price-to-book multiple.

HIG: Mixed Valuation Indicators, Modest P/E

Seeking Alpha

Compared to its peers, with a solid valuation, but mixed overall metrics, HIG’s growth trajectory is healthy. Profitability trends, meanwhile, are likewise robust considering a free cash flow yield that is currently above 15% today.

The sellside has been turning increasingly bullish on HIG, evidenced by 15 EPS upgrades in the past 90 days compared to just 3 downgrades. Finally, share-price momentum is exceptionally high with HIG – I will detail key price levels to watch on the chart later in the article.

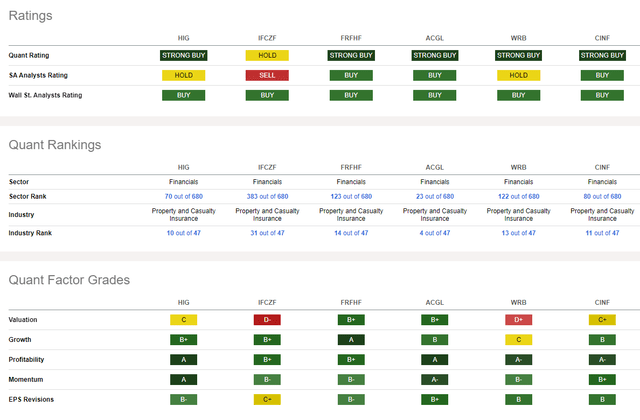

Competitor Analysis

Seeking Alpha

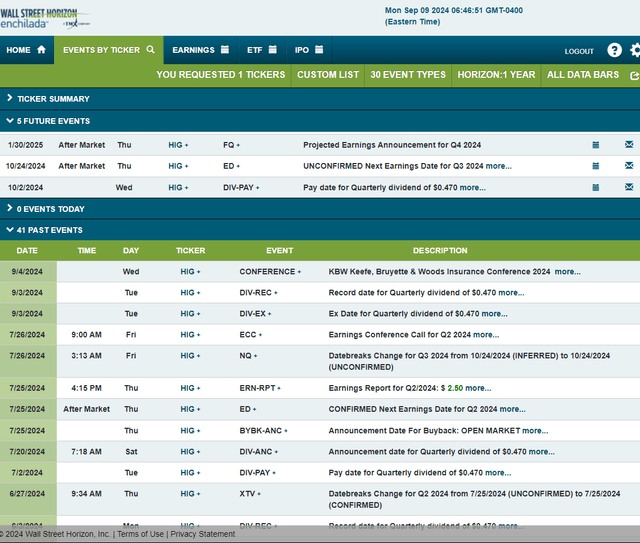

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q3 2024 earnings date of Thursday, October 24 AMC. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

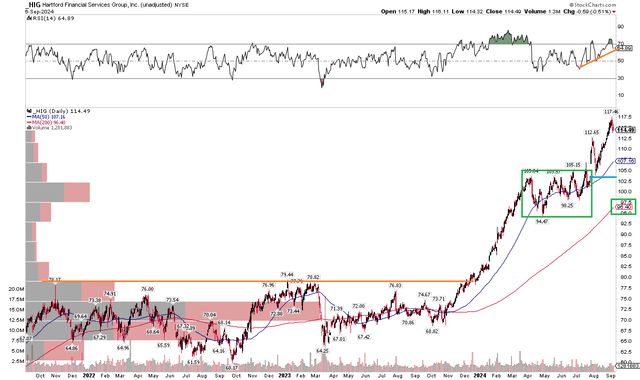

The Technical Take

HIG is one of the biggest winners in the US stock market in the past year (and it has nothing to do with AI). Shares have returned more than 60%, nearly tripling the S&P 500’s performance. The question now is, “Has HIG come too far, too fast?” I don’t think so. Notice in the chart below that the insurance stock went through a multi-month consolidation period from March through much of July before taking its next leg higher. That pause was very healthy, setting the stage for another notable run.

But with shares more than 20% above the long-term 200-day moving average and a high RSI momentum reading, bears might suggest that there are ‘overbought’ risks. Perhaps the stock does pull back, but support should come into play at previous resistance levels in the $103 to $105 range. Moreover, the stock did achieve its measured move price objective of $116 based on the height of the Q2-Q3 range. Big picture, however, the bulls control the primary trend, and I see momentum persisting.

HIG: Bullish Uptrend, Shares Extended from the 200dma

Stockcharts.com

The Bottom Line

I have a buy rating on HIG. I see its earnings story as strong while the technical situation is likewise sanguine ahead of earnings next month.

Read the full article here