September Market Struggles

Market volatility spiked in August, with major indices taking heavy losses, before quickly bouncing back. While the remainder of the month saw more docile markets, there’s no guarantee this trend will continue, especially given the persistent volatility in the S&P VIX Index. If the early days of September are any indication, it seems seasonal volatility is here to stay, with markets potentially facing a turbulent month ahead.

Why is September the worst month for stocks?

September can be a rough month for equity markets, as traders often reassess their portfolios and make adjustments for the fourth quarter that can spur market sell-offs. The S&P 500 slipped last Friday, and historical precedent suggests that September could be an overall down market month

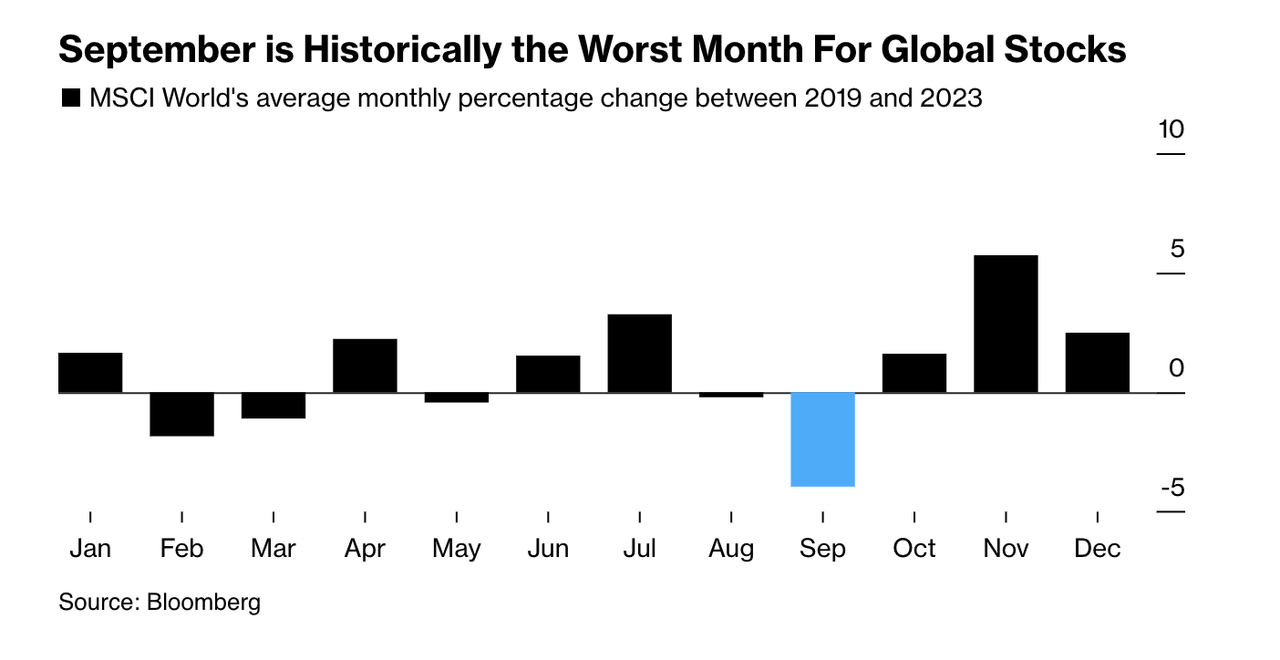

September is Historically the Worst Month For Global Stocks (Bloomberg)

The chart above illustrates average monthly returns for global stocks between 2019 and 2023, with September performing the worst. Outside of the seasonal volatility, a couple of events could impact market movements in September.

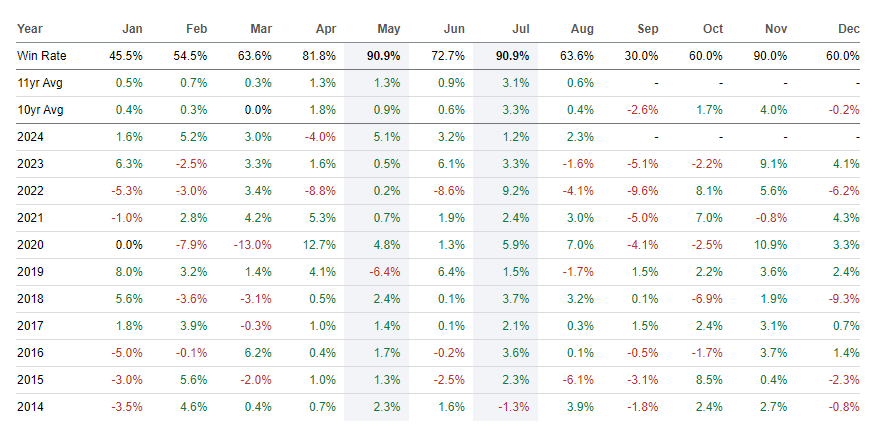

Over The Last 10 Years, During September the S&P 500 Win Rate Was Only 30%

Historical S&P 500 Monthly Returns (SA Premium)

The September Effect

As investors return from summer, seasonal volatility and the potential impacts of this year’s presidential election and upcoming FOMC meeting may also drive market movement this month.

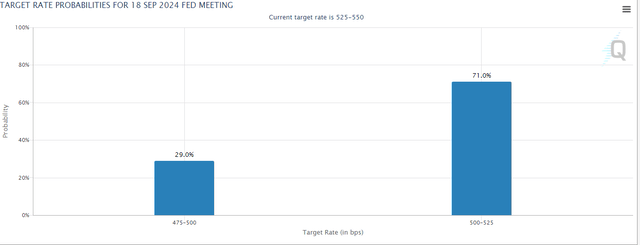

1. September 18 FOMC Meeting

The Federal Reserve is expected to cut interest rates at its next meeting. The August jobs report, considered a key factor in the Fed’s decision on the size of the rate cut, showed slight improvement compared with July figures, though still missed consensus estimates. The direction the Fed will take remains ambiguous. Right now the probabilities for a 25 bps cut remain at 71%. A higher or lower than anticipated rate cut has the potential to swing markets in the coming month.

Target Rate Probabilities For 18 September 2024 Fed Meeting (CME FedWatch)

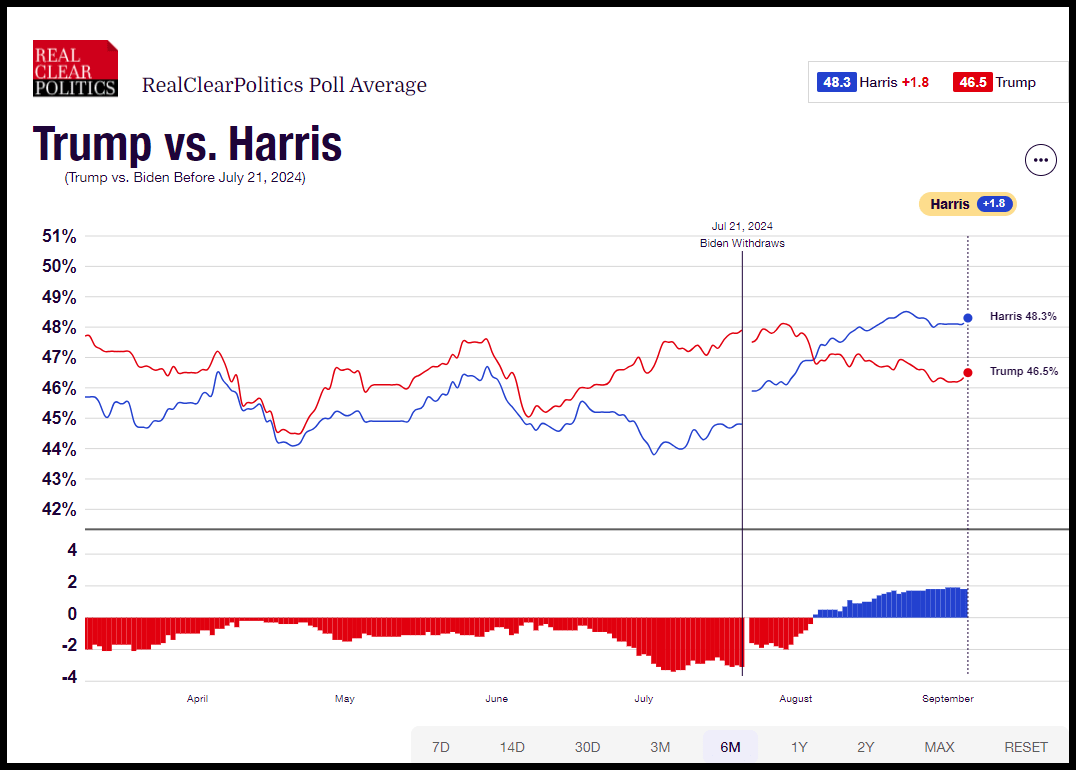

2. Presidential Elections

The forthcoming US presidential elections could also contribute to a sustained period of uncertainty for equity markets.

Trump vs. Harris Poll Average (RealClear Polling)

As the U.S. presidential election draws near, Wall Street speculates how changes in administration might impact the markets. As the news cycle accelerates between now and November, markets could move based on outcome perceptions, which is why the Quant Team has identified some top stocks for a September dip.

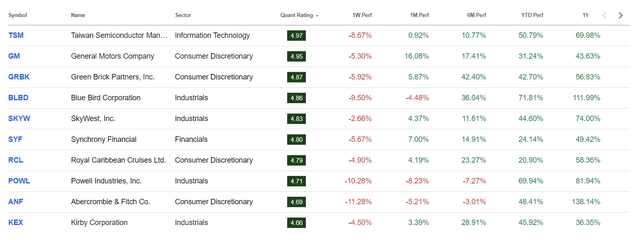

Top Rated Stocks for A September Dip

SA Quant has identified ten highly Quant-rated stocks that score highly across Factor Grades with “Strong Buy” Quant recommendations. Factor Grades rate investment characteristics on a sector-relative basis. Each stock offers solid aggregate characteristics that consider growth, profitability, momentum, value, and EPS revision grades. Notably, eight of the stocks featured were selected for Seeking Alpha’s exclusive Alpha Picks portfolio. Alpha Picks is a service, with additional strict parameters, that recommends Seeking Alpha’s Top Quant recommendations. In addition to these criteria, the following metrics were also applied to the stock screen:

-

1. Market capitalization > 500M

-

2. Stock price >$2.00

Stocks in this article are listed in the order of their overall Quant ratings, which are calculated on a sector-relative basis and represent a blend of sectors and industries to give investors a diverse set of picks.

Top Rated Stocks for A September Dip Performance

Top Rated Stocks for A September Dip Performance (SA Premium)

1. Taiwan Semiconductor Manufacturing Company Limited (TSM)

-

Sector: Information Technology

-

Quant Sector Ranking (as of 9/9/2024): 3 out of 556

-

Quant Industry Ranking (as of 9/9/2024): 1 out of 65

-

Market Capitalization: $742.81B

-

Quant Rating: Strong Buy

Top 10 lists in 2024 would only be complete with a semiconductor play. TSM is the top Quant-ranked semiconductor company and one of the most valuable companies in the world and has the gains to show for it, delivering 81.67% over the past year. TSM is a critical link in the AI supply chain, producing chips for computing devices from smartphones to major AI systems. TSM’s key customers include tech giants Apple (AAPL), Nvidia (NVDA), and Qualcomm (QCOM). The company’s main challenges have been around capacity constraints, with demand for semiconductor chips outpacing supply. TSM has been rapidly addressing capacity concerns with the construction of three new manufacturing plants in Arizona and the recent acquisition of a Taiwan-based plant, among other planned expansions.

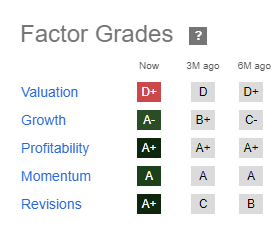

TSM Stock Factor Grades

TSM Stock Factor Grades (SA Premium)

The company’s measures of profitability are exceptional, with an EBITDA margin of 67.18% and a net income margin of 37.85%. ROE is currently 26.45%, while ROA is 15.43%. TSM’s robust growth is evidenced by its year-over-year and forward revenue growth of 9.44% and 13.32%, respectively. Value is hard to come by in the semiconductor space, however the company is still trading at a discount to the sector in terms of both price-to-earnings as well as price-to-cash flow. TSM has committed $30-32B of its capital budget for capex spending on advanced processing technologies, which could put pressure on margins, yet, create a runway for substantial growth. TSM’s dominant position in the space, coupled with its solid fundamentals, make this a top stock for investors looking to capitalize on the AI revolution. TSM even possesses a better valuation than Nvidia on its forward PEG Ratio at 0.94x vs 1.03x, respectively. In regards to Cash Per Share, TSM also has a whopping $2.13 vs. NVDA at on $0.35 per share. In markets like this, ‘Cash is King’.

2. General Motors (GM)

-

Sector: Consumer Discretionary

-

Quant Sector Ranking (as of 9/9/2024): 1 out of 502

-

Quant Industry Ranking (as of 9/9/2024): 1 out of 29

-

Market Capitalization: $52.98B

-

Quant Rating: Strong Buy

GM still stands as the top Quant-rated automaker since its addition to the Top 10 Stocks for H2 2024 back in June. The company has posted 10.77% in returns in the last month and has delivered 43.63% on a trailing 1-year basis. Despite the significant gains, the stock is still graded an ‘A+’ in terms of valuation, trading at 5.17x forward earnings, which is nearly a 70% reduction compared with the sector median. GM scores very well across the majority of its valuation metrics and offers a modest forward dividend yield of 0.99%

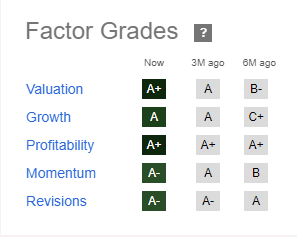

GM Stock Factor Grades

GM Stock Factor Grades (SA Premium)

Outside of valuation, GM boasts “A” range ratings across all factor grades. Profitability and growth characteristics stand out. The company’s TTM net income margin and forward revenue growth are 6.22% and 4.53%, respectively, exceeding sector medians by large margins. GM has received a whopping 22 positive EPS revisions, with only three downward revisions in the last 90 days. The company’s strong balance sheet and growth positioning more than warrant its place among top stocks to buy for a September dip.

3. Green Brick Partners (GRBK)

-

Sector: Consumer Discretionary

-

Quant Sector Ranking (as of 9/4/2024): 5 out of 502

-

Quant Industry Ranking (as of 9/4/2024): 1 out of 24

-

Market Capitalization: $3.30B

-

Quant Rating: Strong Buy

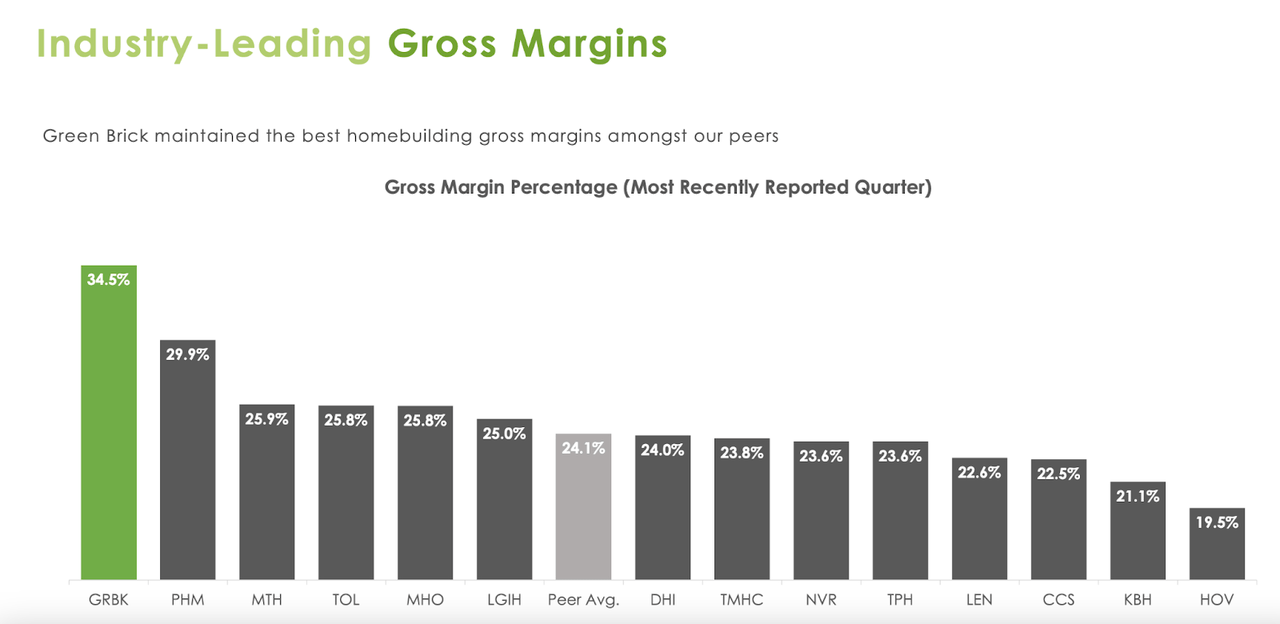

Green Brick Partners is a top Quant-ranted homebuilder that specializes in the acquisition, development, and sale of residential properties, primarily in the Sunbelt. The stock has performed strongly in 2024, delivering 61.97% on a trailing one-year basis. GRBK led peers in gross profit margins in Q2 while also leading the industry with the lowest debt-to-capital ratio of 17.7%. The company’s financial and operational stewardship has resulted in $133M in cash on hand and $360M in lines of undrawn credit at the end of Q2.

Green Brick Partners’ Q2 2024 Investor Presentation (Green Brick Partners)

In addition to profitability, GRBK is trading at 2.19x its forward book value, which is a -13.56% reduction to the sector median. Forward and TTM P/E ratios of 9.03 and 10.36 represent a -46.73% and -42.46% reduction to the sector median, respectively. In Q2, the company delivered a positive earnings surprise in excess of $57M and experienced three positive EPS revisions in the last 90 days. GRBK is well-positioned in a high-growth region as millennials enter the peak homebuying years in a soon-to-be cycle of monetary easing. The company’s growth prospects and solid fundamentals make it a potential winner for September.

4. Blue Bird Corporation (BLBD)

-

Sector: Industrials

-

Quant Sector Ranking (as of 9/9/2024): 10 out of 628

-

Quant Industry Ranking (as of 9/9/2024): 2 out of 39

-

Market Capitalization: $1.50B

-

Quant Rating: Strong Buy

BLBD, a leading manufacturer of school buses, has been a Quant “Strong Buy” mainstay since December 2023. Since the start of the new year the company has posted a 70.14% return. The company has made bold moves, accelerating the manufacturing of alternative fuel source vehicles, including EVs, which has been a significant growth driver for the company.

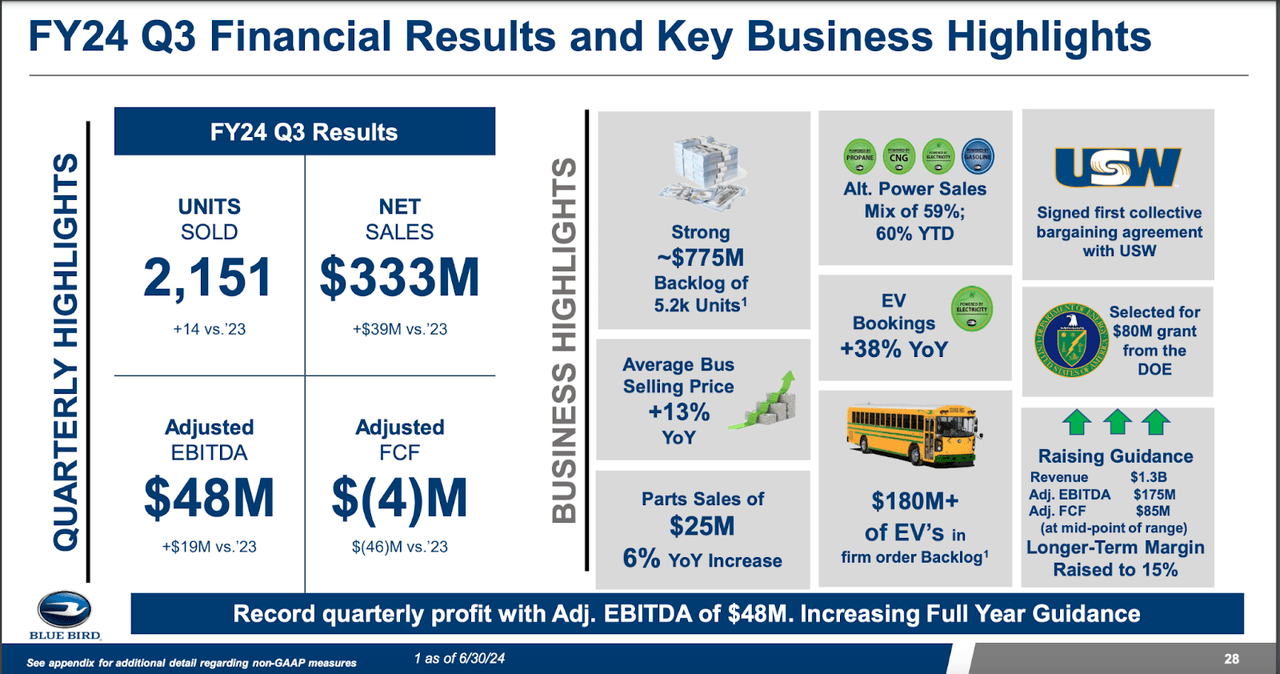

Blue Bird Corporation Q3 Investor Presentation (Blue Bird Corporation)

BLBD’s key Q3 financials show a strong increase in year-over-year net sales, resulting in an adjusted EBITDA of $48M, a $19M increase from 2023. Other strong profitability metrics include a TTM ROE of 134.71% and a TTM ROA of 21.26%.

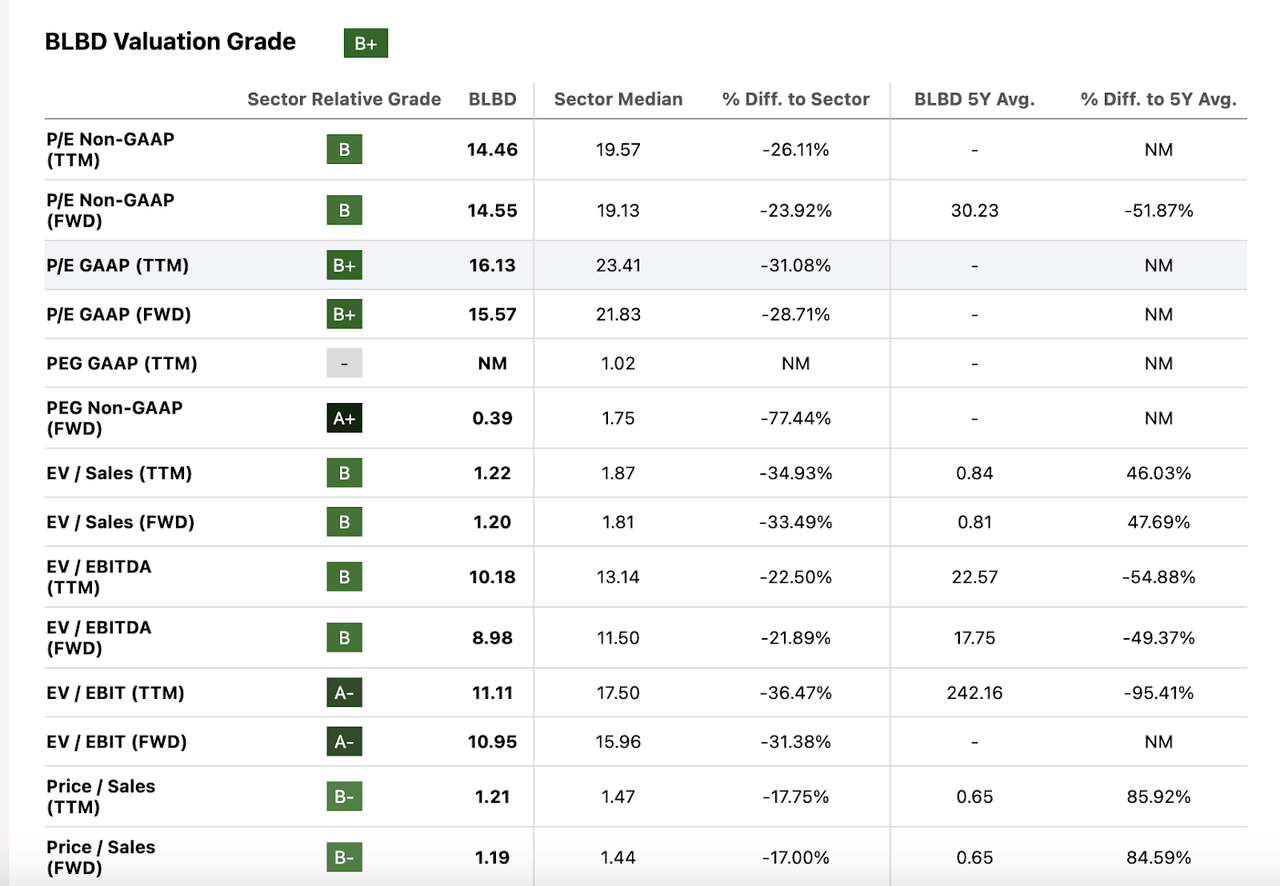

BLBD Valuation Grade (SA Premium)

The company’s enormous price momentum in the last year has not diminished the value it can offer investors. BLBD’s current forward price-to-earnings ratio of 15.57 is a nearly 30% reduction to the sector median, while its price-to-sales ratio of 1.19 beats the sector mean by almost 18%. BLBW’s solid positioning has earned it four upwardly revised EPS estimates in the last 90 days. In addition to solid fundamentals, BLBW’s positioning as the school bus hegemon, with an eye towards the clean energy transition, suggests the stock could still have room to run and make it well qualified for this list.

5. SkyWest, Inc. (SKYW)

-

Sector: Industrials

-

Quant Sector Ranking (as of 9/9/2024): 12 out of 628

-

Quant Industry Ranking (as of 9/9/2024): 1 out of 27

-

Market Capitalization: $3.03B

-

Quant Rating: Strong Buy

SKYW is the Quant-ranked passenger airline that has returned 73.32% in the last year. The regional carrier, based out of Utah, has benefitted from a surge in demand for regional flying, particularly to underserved locations, since the end of the pandemic. SKYW reported a year-over-year increase in revenue of 19%, totaling $867M and beating consensus estimates by $40.52M. Year-over-year EBITDA growth stands at 35.24%, which outstrips the sector median by 447.80%.

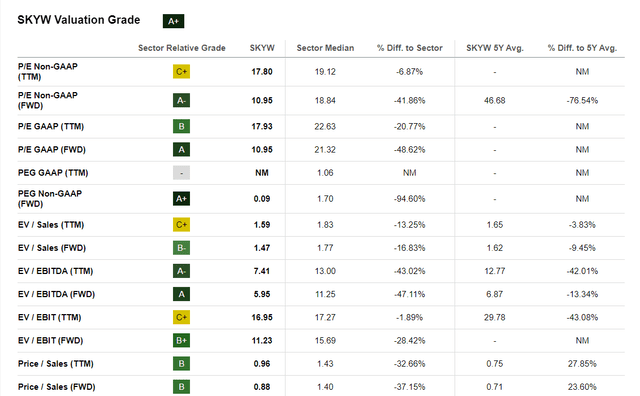

SKYW Stock Valuation Grade

SKYW Stock Valuation Grade (SA Premium)

SKYW also scores well in terms of profitability. Its TTM EBITDA margin is 21.41%, which beats the sector median by 55.06%. Even though SKYW has been rated as a buy or strong buy since September 1st of last year, the company is very attractively valued, banking an overall “A+” valuation grade and scoring above average for most valuation metrics. The company has seen improvements with respect to the industry-wide challenge of pilot attrition, and expects to employ over 5,000 pilots by year-end, coupled with an expected full utilization rate of E175 fleet by year-end suggests SKYW has a further runway for positive performance.

6. Synchrony Financial (SYF)

-

Sector: Financials

-

Quant Sector Ranking (as of 9/9/2024): 41 out of 680

-

Quant Industry Ranking (as of 9/9/2024): 7 out of 38

-

Market Capitalization: $18.74B

-

Quant Rating: Strong Buy

Synchrony Financial is a top Quant-ranked consumer finance company specializing in lending programs for retailers and healthcare providers, including store and co-branded credit cards and savings products. The company has delivered an exceptional 51.96% return on a trailing 1-year basis, outperforming both the broader financial sector and the S&P 500.

SYF Price Performance vs. S&P 500 and Financials Sector (XLF)

SYF Price Performance vs. S&P 500 and Financials Sector (XLF) (SA Premium)

Key growth figures include a 10% increase in consumer deposits, an 8% increase in loan receivables, and a 7% rise in net interest income year-over-year.

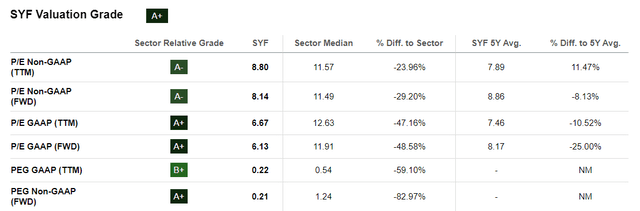

SYF Stock Valuation Grade

SYF Stock Valuation Grade (SA Premium)

Despite SYF’s explosive growth, it has retained substantial value for investors, with a TTM P/E of 8.14x and a forward PEG ratio that crushes the sector median at a -82.97% reduction. Synchrony offers a 2.11% forward dividend yield and has demonstrated commitment to shareholder value. SYF’s strong financials and growth have captured the attention of Wall Street analysts, and the company has seen ten upward revisions in the last 90 days. Although potential headwinds from a reduced interest rate environment could negatively impact net interest margins, SYF is poised for continued growth and has the potential for further upside.

7. Royal Caribbean Cruises Ltd. (RCL)

-

Sector: Consumer Discretionary

-

Quant Sector Ranking (as of 9/9/2024): 14 out of 502

-

Quant Industry Ranking (as of 9/9/2024): 3 out of 36

-

Market Capitalization: $42.08B

-

Quant Rating: Strong Buy

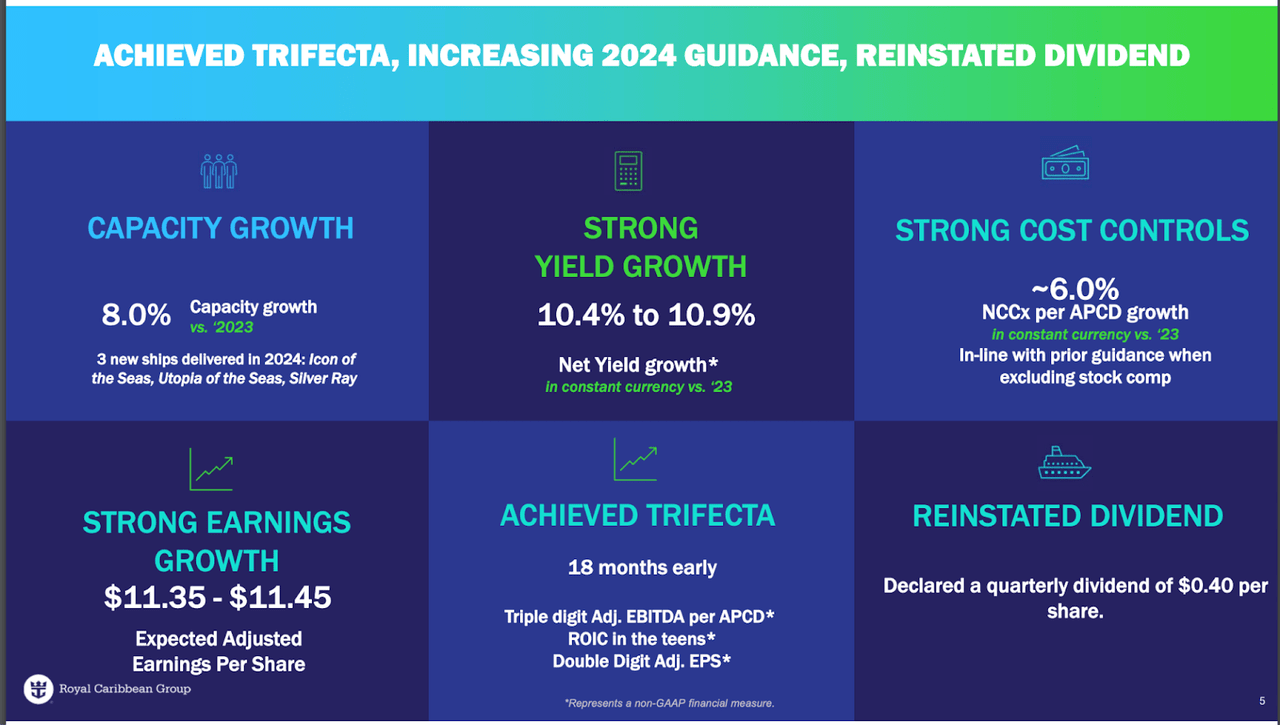

Cruise lines have enjoyed large gains in 2024, with booking demands exceeding pre-pandemic levels for the first time since the onset of COVID. RCL is no exception; the company has delivered 23.50% in returns YTD and 64.10% on a trailing 1-year basis. The company is focused on a strategy of moderate increases in capacity and yield, which is a measure of the revenue generated per cruise day, as well as cost discipline to deliver shareholder value.

Royal Caribbean Cruises Q2 2024 Investor Presentation (Royal Caribbean Cruises)

This strategy has translated to key metrics in growth and profitability. RCL has a TTM EBITDA margin of 33.99% and cash from operations at $4.68B. This success has allowed RCL to reinstate its dividend, which will begin paying in October. Optimism about RCL has permeated to Wall Street; the company experienced 19 upwardly revised EPS estimates in the last 90 days. While RCL is stretched from a valuation perspective, it still scores well on some key metrics, like its forward price-to-earnings ratio, representing a -16.11% reduction to the sector median. Strong booking trends through the end of 2025, coupled with expansion in capacity, could position RCL to continue its current positive trend and make it a top stock for September.

8. Powell Industries, Inc. (POWL)

-

Sector: Industrials

-

Quant Sector Ranking (as of 9/9/2024): 23 out of 628

-

Quant Industry Ranking (as of 9/9/2024): 2 out of 66

-

Market Capitalization: $1.80B

-

Quant Rating: Strong Buy

Powell Industries designs and manufactures custom-integrated solutions to control and manage electricity in facilities across industries, such as oil and gas, transportation, and utilities. Their products include computerized control systems, electrical switches, and safety infrastructure for electrical hazards. Powell also offers extensive servicing capabilities for its solutions to ensure reliability.

The company’s share price has soared YTD, +75.80%. In July, POWL reported a 50% year-over-year revenue increase and a net income of $46.2M, which doubled when compared to 2023. Much of this growth was driven by its oil and gas and petrochemicals segments. Powell is positioning itself to capitalize on trends in the clean energy transition opportunities, as well as automation to drive future growth.

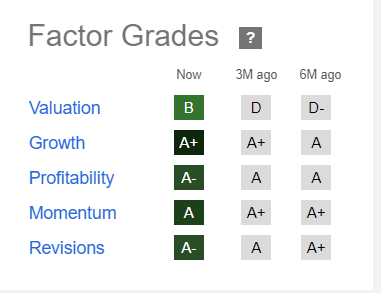

POWL Stock Factor Grades

POWL Stock Factor Grades (SA Premium)

In addition to growth, POWL scores highly across several other factor grades, in particular in terms of momentum and revisions. The company beat consensus EPS estimates by $1.63 and experienced a positive revenue surprise of $65.99M in Q2.

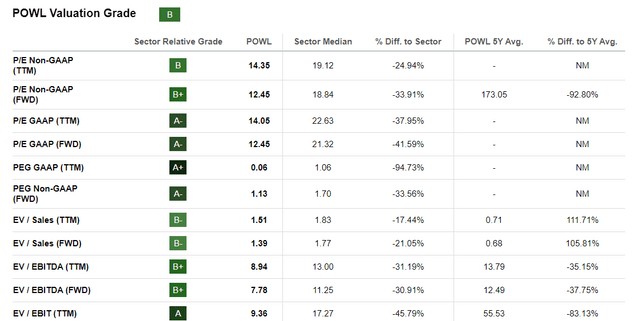

POWL Stock Valuation Grade

POWL Stock Valuation Grade (SA Premium)

POWL remains attractively valued despite its recent share price gains. The company is trading at 12.45 forward earnings, which is a -41.59% reduction relative to the sector median. POWL’s bargain status, exceptional growth, and momentum characteristics make it a solid offering for investors looking for potential upside in September.

9. Abercrombie & Fitch, Co. (ANF)

-

Sector: Consumer Discretionary

-

Quant Sector Ranking (as of 9/9/2024): 24 out of 502

-

Quant Industry Ranking (as of 9/9/2024): 2 out of 37

-

Market Capitalization: $6.69 B

-

Quant Rating: Strong Buy

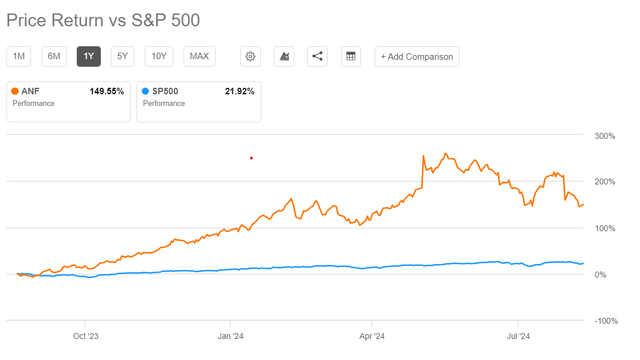

Millennial retail favorite Abercrombie & Fitch has experienced outstanding momentum over the last 18 months. In an era of explosive e-commerce growth, more traditional apparel retailers like ANF have needed to evolve to keep pace with shifting consumer trends. ANF has invested heavily in improving customers’ digital experience and targeting an older, post-collegiate demographic. The company’s trailing 1-year return totals 149.55%, and it is the top-performing stock on this list for the same period. The chart below illustrates the magnitude to which ANF has outperformed the broader market in the last year.

ANF Price Performance vs. S&P 500

ANF Price Performance vs. S&P 500 (SA Premium)

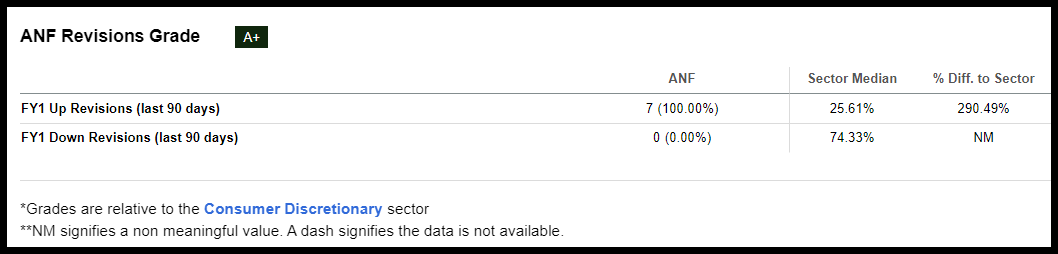

Strong fundamentals undergird ANF’s hype. In addition to an enormous gross profit margin of 64.60%, the company posts 21% yoy revenue growth and forward EBITDA growth at 55.13%. This strong positioning has helped drive seven upwardly revised EPS estimates by Wall Street analysts and zero downward revisions.

ANF Revisions Grade (SA Premium)

While ANF’s value grade has weakened as a result of its sustained reign as a top-rated apparel retail stock, it still offers a favorable forward P/E ratio of 12.75. There are tailwinds for consumer discretionaries on the horizon, with interest rate reductions and the holiday season coming into view. These catalysts could help lift the sector for the remainder of the year, and ANF could stand to benefit.

10. Kirby Corporation (KEX)

-

Sector: Industrials

-

Quant Sector Ranking (as of 9/9/2024): 27 out of 628

-

Quant Industry Ranking (as of 9/9/2024): 2 out of 23

-

Market Capitalization: $6.63B

-

Quant Rating: Strong Buy

Kirby is a key player in US maritime infrastructure, operating tank barges and towing vessels in inland waterways and coastal regions of the US. The company’s revenue is generated from two segments: marine transportation of bulk liquids such as fuel oil and agricultural chemicals, as well as the distribution and servicing of diesel engines and parts used for a number of industrial applications. The marine transportation segment has seen revenues increase 14% year-over-year, while distribution and servicing experienced a revenue decrease of 3% in the same period. This combines to an overall revenue growth of 6.41%, which is a 55.67% increase relative to the sector median.

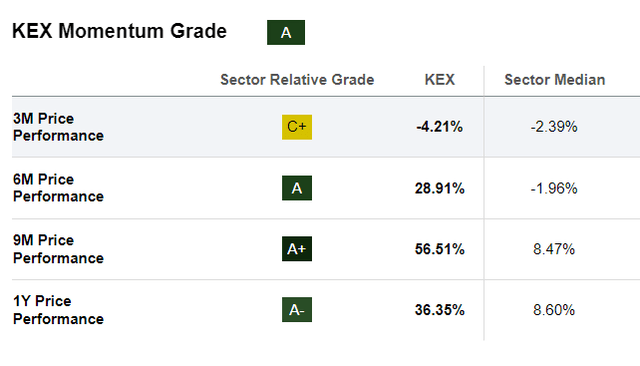

KEX Stock Momentum Grade

KEX Stock Momentum Grade (SA Premium)

Despite a 3M price momentum slowdown, KEX scores well across all other periods. The company beat EPS estimates in Q2 by $0.11 and has received six EPS revisions in the last 90 days, with 0 downward revisions. KEX’s share price appreciation has brought down the company’s overall value grade. However, it still sports favorable forward price-to-book and price-to-cash flow ratios, which are 2.01 and 10.98, respectively. Kirby is vulnerable to weather events and supply chain constraints, however, its dominant market position and diversified customer base across industrial segments provide a margin of safety for the company. KEX is positioned to continue on its positive trajectory, showcasing why it was selected as a top pick for September.

Concluding Summary

September is a historically challenging month for equity markets. This September is no exception. Pessimistic economic data, recession fears, possible lower-than-expected interest rate reductions, and ongoing presidential election news can fuel market volatility and catalyze a potential sell-off in markets in September.

This article spotlights 10 top Quant-rated stocks that have recently pulled back and may present a potential opportunity. These stocks score highly on Seeking Alpha’s Factor Grades and are rated as quant “Strong Buys.” Each of the ten stocks have experienced strong outperformance on a trailing one-year basis, are in differentiated sectors and industries, and based on Quant ratings, have the potential to outperform market movements in September.

We have many Top stocks with strong buy recommendations, and you can filter them using stock screens to suit your specific investment objectives. Consider using Seeking Alpha’s ‘Ratings Screener’ tool to help find stocks that achieve diversification into desired sectors you like. Alternatively, if you’re looking for a select number of Quant Strong Buy recommendations every month, you might want to explore Alpha Picks.

Read the full article here