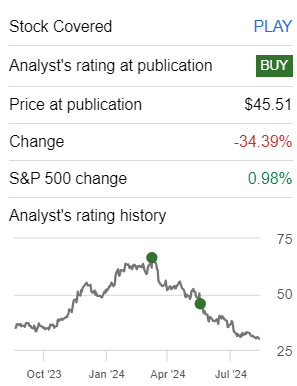

Investment Thesis

Dave & Buster’s (NASDAQ:PLAY) delivered fiscal Q2 2024 earnings results that saw investors cheer, driving the stock higher by more than 10% after hours.

But as we look through, I’m not blown away by its near-term prospects. Even though I had been bullish on this stock for the past 6 months, and in hindsight, I clearly made a bad call being bullish, today, I’m not asserting this stock with a BUY rating.

I’m moving to the sidelines, as I turn neutral on this stock. Yes, the stock is clearly cheap, but I don’t see a path for the business to reach the profitability levels I was expecting.

Rapid Recap

I made a terrible call on PLAY. Here’s what I said in my previous analysis,

I maintain that Dave & Buster’s comparables will naturally improve starting fiscal Q2, which will overshadow its lackluster and unclear strategy. In 90 days’ time, I’m inclined to believe that its share price will be higher than $50 and climbing higher.

Author’s work on PLAY

Today, including the after-hours jump, the stock is at $33 per share. An unquestionably bad call on my part.

And these latest results don’t convince me that its underlying prospects are so enticing and worth doubling down. Therefore, I’m neutral.

Dave & Buster’s Near-Term Prospects

Dave & Buster’s is a dining and entertainment company that combines food, drinks, and arcade-style games under one roof. It operates venues that offer a wide array of interactive games, events, and food and beverage options, catering to both casual visitors and event-based bookings.

The company has a focus on enhancing guest experiences through strategic initiatives such as remodeling stores, improving its menu offerings, and implementing loyalty programs. Recently, Dave & Buster’s has also expanded its footprint with new store openings and remodels, aiming to drive traffic and revenue growth.

In terms of near-term prospects, as discussed on the earnings call, Dave & Buster’s is seeing positive early results from its remodeled stores and expects these to contribute to revenue growth in the coming quarters.

Additionally, its enhanced menu and beverage offerings, along with digital marketing and pricing strategies, are likely to strengthen its top-line performance.

The company also plans to open more stores domestically and internationally, which should further support growth.

However, despite some near-term headwinds, management remains confident that these initiatives will drive same-store sales growth in the near-term.

And yet, same-store sales were down 6.3% y/y. This was due to a challenging macroeconomic environment with weakened consumer spending.

The company acknowledged these pressures in the second quarter, and while it has implemented cost-saving measures to protect margins, it faces uncertainty in the broader economy.

As discussed on the call, there’s a cautious consumer base that continues to weigh on its top-line growth rates.

Given this balanced context, let’s now discuss its fundamentals.

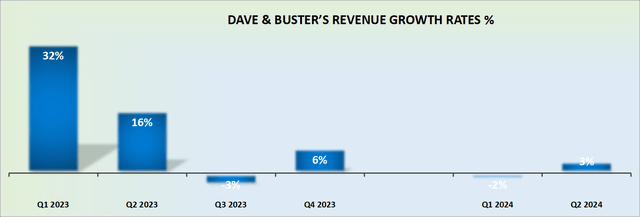

Revenue Growth Rates Will Continue to Improve

PLAY revenue growth rates — author’s work

This has been my thesis throughout 2024:

Author’s work

I’ve been consistent in my analysis of Dave & Buster’s that I believe the company will deliver at least mid-single-digit CAGR in 2024.

Given that we are not even in its easiest comparable quarter of this fiscal year, namely fiscal Q3, and already Dave & Buster’s is reporting very close to mid-single-digits, I’m reassured that my estimate for its topline to grow by mid-single-digits is the right ballpark.

This is clearly a bullish consideration that investors are likely to welcome. But the thesis isn’t very straightforward. After all, there’s an aspect that muddles up this investment thesis, and that’s what we discuss in the next section.

PLAY Stock Valuation — 2x EBITDA

In my previous analysis, relating to fiscal Q1 2024, I said:

[Dave & Buster’s] EBITDA margins this quarter stood at 27.1%, which further supports my previous argument that there’s a high likelihood that Dave & Buster’s will deliver 26% EBITDA margins this year. After all, despite the tough environment, Dave & Buster’s is already reporting 110 basis points higher than my previous estimate.

[…] I remain confident that Dave & Buster’s will deliver at least $620 million of EBITDA this year. This puts the stock priced at less than 3x EBITDA.

And now, for its recently reported quarter, fiscal Q2 2024, Dave & Buster’s EBITDA margins stood at 27.2%. Not only is PLAY tracking ahead of my previous estimate for 26% of EBITDA for 2024, but in fact, it actually improved relative to fiscal Q1 2024’s EBITDA margin of 27.1%.

And yet, although this is clearly a positive aspect, I’m not convinced that Dave & Buster’s is able to “deliver at least $620 million of EBITDA this year” as I previously estimated.

Here’s my back-of-the-napkin calculations. H1 2024 has delivered approximately $311 million. Next, if we assume that fiscal Q3 delivers a slight improvement relative to the same period a year ago, it may deliver approximately $88 million. Hence, this leaves a massive burden for fiscal Q4 2024 to deliver $220 million in the holiday quarter.

Put more starkly, I don’t believe that Dave & Buster’s has enough in its tank to suddenly grow its bottom-line EBITDA by anything more than 10% to 15% y/y in fiscal 2024.

And no way as much as the 44% increase relative to Q4 of the prior year required to reach my original forecast.

Most likely, Dave & Buster’s will deliver this year about $570 million. This, of course, is cheap. Nobody is disputing otherwise. And certainly not me. But I’m not sure that cheap is enough of an argument to get investors pounding their chest to buy this stock.

After all, practically equaling its market cap, investors also have to contend with a debt stack that also equals about $1.3 billion.

Therefore, I’m neutral on this name.

The Bottom Line

In conclusion, while I had previously been bullish on Dave & Buster’s, it’s clear in hindsight that I made a bad call.

The stock has underperformed my expectations, and despite its current low valuation, I don’t see a clear path for it to meet the profitability levels I had anticipated.

With uncertainties around same-store sales growth, a challenging macroeconomic environment, and a significant debt load, I believe the best course of action now is to move to the sidelines. Although PLAY may seem cheap, I’m not eager to play with this stock at this point.

Read the full article here