Thesis

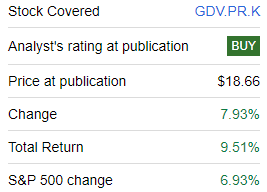

In our CEF research and analysis, we sometimes write about the preferred shares issued by Clefs, which are a form of leverage. One of those securities is represented by the Gabelli Dividend & Income Trust (GDV) preferred equity, namely the preferred Series K (NYSE:GDV.PR.K). We covered this name earlier in the year when we re-iterated our ‘Buy’ rating on the name, highlighting how the preferred shares represented a rates play. As the yield curve shifted lower, the Series K delivered a high total return:

Returns (Seeking Alpha)

GDV.PR.K is up over 9.5% on a total return basis since our rating, outperforming the S&P 500 in the process. The shares are perpetual, thus exhibiting a high duration, which have made them very sensitive to interest rates in the past.

In today’s article, we are going to re-visit the name, and highlight for retail investors why we believe the securities no longer offer an attractive entry point, but are a robust name to hold (we own and are holding the name).

Analytics – perpetual preferred equity

The preferred shares are perpetual, with a first call date in October 2026. Given their low coupon of 4.25%, we are of the opinion the shares will not be called in 2026, and in fact they will remain outstanding for the foreseeable future. That aspect translates into a high duration figure, which we estimate at around 7 years. If we look at the pricing for the shares, they have been moving with a high correlation to the equivalent Treasuries ETF iShares 7-10 Year Treasury Bond ETF (IEF):

Correlation to Treasuries (Seeking Alpha)

We can notice from the above chart (courtesy of Seeking Alpha) the very high correlation between the two instruments in the past year. While GDV.PR.K is up 6.3% now from a price perspective, IEF is up 5.5%.

The high duration was punitive when rates were moving up, but has helped the preferred shares outperform as the curve has shifted lower. As a reminder, a 7-year duration translates into a +7% gain when the equivalent node in the yield curve moves lower by 100 bps. And this is exactly what we have witnessed.

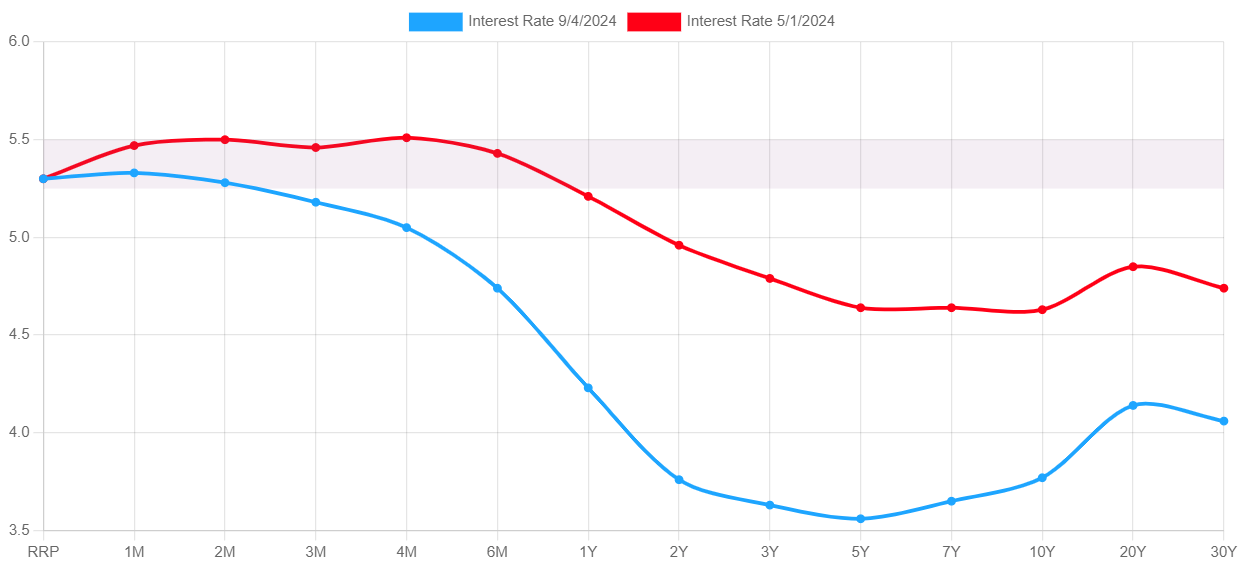

The yield curve has shifted significantly lower

In the past four months, the yield curve has shifted significantly lower:

Yield Curve (USTreasuryYieldCurve)

We can see from the above graph that the intermediate portion of the yield curve has shifted by as much as 100 bps lower. Those are seismic shifts, and account for the massive rally in GDV.PR.K. The preferred shares have a credit component as well, but they are mainly driven by rates. As rates moved lower, the share price moved higher.

We are of the opinion that the main part of the move is now behind us, with the curve close to where it should be from a term premium perspective. If the new neutral rate is somewhere between 2.5% and 3%, then the concept of term premium dictates that the intermediate portion of the curve should be roughly 100 bps wider. With the 10-year rate close to 3.66% as we are writing this article, we are hard-pressed to see treasuries rallying significantly more from here.

Mind you, the market is still pricing a soft landing base case, where the rates’ normalization will be gradual and not driven by a market crash. That means that rates and the curve will settle within normal historic mechanics, thus no need for over-shooting on the downside.

Still an attractive current yield to hold

Despite the duration-driven capital gains for the ticker being behind us, we still believe the name offers an appealing current dividend yield of 5.3% in today’s macro environment. The shares offer a spread over risk-free rates given the credit component embedded in the CEF, thus making it more appealing than outright treasuries.

An investor can go to the ‘Dividends – Dividend Yield’ tab on the Seeking Alpha platform to see the historic levels offered by the name. Going forward, a holder in the name will clip the current yield, while also being able to get more capital gains if we do get a recession and thus a more pronounced shift lower in yields.

Risk factors

The biggest risk factor for holding this name is a re-emergence of an inflationary environment. If the Fed cuts before inflationary pressures are fully quashed, we will get a scenario where the CPI will re-accelerate higher, thus forcing the Fed to stop cutting and the market to start pricing Fed hikes. This situation would see the yield curve shift up, thus generating a loss in the securities via their duration component. We find this scenario to be remote at this juncture, but it is something to consider while holding the name.

Conclusion

GDV.PR.K are preferred shares issued by the Gabelli Dividend & Income Trust. The shares are perpetual, and we do not expect them to be called in 2026. Their high duration accounted for steep losses in 2022, but has now helped holders to record attractive gains as the yield curve has shifted lower. We have seen a 100 bps of tightening in yields in the past months, and we believe we are close to a neutral level in a soft landing base case scenario. With the bulk of the capital gains behind us, we no longer find GDV.PR.K attractive to buy, but consider the shares an attractive hold. We own this name and continue to hold after the spectacular total returns recorded in 2024.

Read the full article here