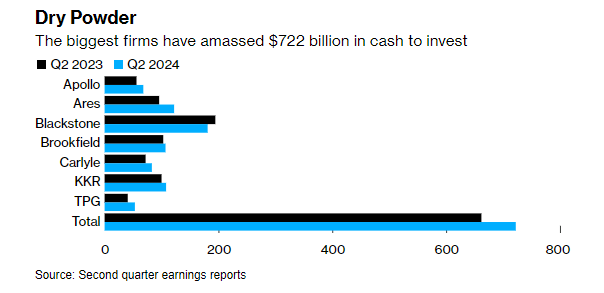

We see increasing evidence that deal flows for private equity asset managers are improving as the U.S. economy enters into a new monetary easing cycle. According to a recent report published by the Financial Times, four of the largest U.S. private capital groups, including Ares (ARES), Apollo (APO), Blackstone (BX), and KKR (KKR), have deployed a combined US$162bn in Q2 alone. Earnings data compiled by Bloomberg also indicate that seven of the world’s largest private equity asset managers collectively have as much as US$722bn in dry powder to invest as of June 2024.

Bloomberg

With the Federal Reserve widely expected to make its first-rate cut at its FOMC meeting next week, asset managers will be looking to accelerate the deployment of capital in a bid to outmanoeuvre the competition for cutting the most lucrative deals. Anecdotally, many asset managers also reportedly mentioned that their investment teams are looking at an increasingly larger number of opportunities as deal flows have picked up meaningfully in recent months.

Carlyle Group (NASDAQ:CG), which has been lagging behind its peers in expanding its private credit portfolio, has also announced several billion-dollar deals. This includes winning the bid with KKR for a US$10bn student-loan portfolio from Discover Financial Services that was announced in June and acquiring Advance Auto Parts Inc.’s Worldpac unit for US$1.5bn. Carlyle has also successfully raised JPY430bn this year for its fifth Japan buyout fund, which is 70% larger than the previous fund raised in 2021 and the largest Japan-focused buyout fund ever raised.

Quality Versus Value

Within the group of alternative asset managers, we like Blackstone (BX) specifically for its concentrated exposure to opportunities in residential REITs, data centres, and energy transition themes. In terms of portfolio quality, manager skill, and track record, Blackstone remains our favourite pick among private market asset managers. Therefore, we have recently upgraded our rating on BX to “Strong Buy.”

But in terms of valuation, we think Carlyle Group is the most attractive of the lot and by a significant margin. We first initiated coverage of Carlyle with a “Buy” rating back in November 2023, when we identified the company as a great value pick versus its more expensive peers. Carlyle was only trading at a forward P/E multiple of 9.7x then. We later took profit on our bullish position following a sharp rally in the stock, locking in a lucrative 43% gain in less than two months. Carlyle’s forward P/E multiple had improved to around 12.9x when we issued our “Sell” rating.

More importantly, we reminded readers then that we were not taking profit on Carlyle due to deteriorating fundamentals. Instead, we still like Carlyle’s long-term fundamentals and strategic shift to diversify into private credit and secondaries. But we saw an opportunity to recycle capital and redeploy those gains into other attractive value opportunities. Furthermore, the growing risk of a pullback in the S&P 500 index at the time also weighed on our decision to take profit on the stock.

Today, Carlyle is once again trading at a compelling forward P/E multiple of just 9.9x versus its peers, which are trading at much more demanding multiples of 15-30x. This makes Carlyle an ideal candidate for a more conservative or value-oriented portfolio. Despite Carlyle being the smallest within the group by market capitalization, the company has produced the second-highest 5-year average ROE of 30.6%.

| Market Cap | TTM Rev | TTM P/E | FWD P/E | TTM ROE | 5Y Avg ROE | |

| APO | 61.5 bn | 26.0 bn | 15.5 | 15.4 | 49.2% | -21.7% |

| BX | 167.5 bn | 9.9 bn | 34.4 | 30.0 | 28.4% | 32.1% |

| KKR | 103.2 bn | 26.6 bn | 29.5 | 25.0 | 19.1% | 15.3% |

| CG | 13.3 bn | 2.8 bn | 10.6 | 9.9 | -7.2% | 24.9% |

Source: Seeking Alpha. APO 5Y Avg ROE is negative due to outlier losses and a merger with Athene Holding in 2022.

Long-Term Fundamentals Remain Intact

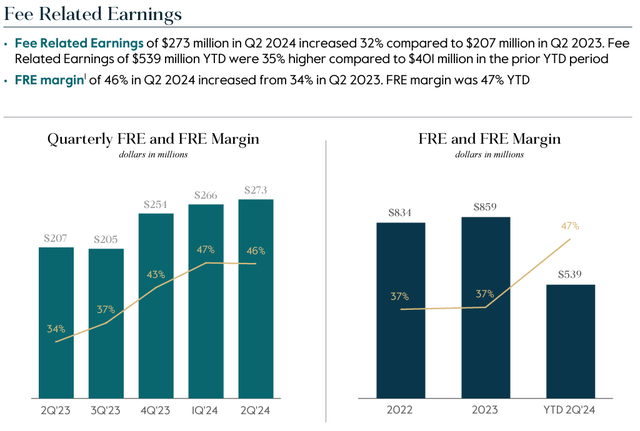

We believe that Carlyle’s long-term fundamentals and brand reputation remain intact. Moreover, fee-related earnings have also been growing at a robust pace in recent quarters, and we think earnings should remain on an uptrend. Carlyle has raised US$18bn in new funds year-to-date, and management is confident that the company remains on track to meet its target of raising US$40bn for 2024.

Carlyle Presentation Slides

Carlyle’s recent performance generally reflects the broader recovery in sentiment towards private markets that we have been witnessing lately. This reinforces our view that Carlyle should continue to perform well as we see more activity and deal flows coming back to the private equity market. Although Carlyle’s recent expansion into private credit and secondaries is rather late compared to its peers, we still think it will provide a decent boost to future earnings performance. Thus, we see little reason to justify why Carlyle should trade at such a deep discount compared to its peers.

Not only do we view Carlyle as the safer bet because of its compelling valuation, but we also think that Carlyle provides the most upside potential, given that we are just starting to see activity pick up in the private equity market.

Risk To Outlook

To be clear, we acknowledge that Carlyle is an underperforming company, which explains its heavily discounted valuations compared to those of its peers. Due to Carlyle’s concentrated portfolio, which focuses heavily on the private equity market, the company has been struggling to realize investments and cut new deals due to the high interest rate environment in recent years.

The company’s late push into the private credit and secondaries market also explains why it is lagging behind its peers in terms of earnings. In short, Carlyle had the wrong portfolio composition at the wrong time.

Bloomberg

The biggest risk to our bullish view of Carlyle would be a weaker-than-expected recovery for the IPO market, which is crucial for realizations for private equity funds.

As we have seen in the previous 2009–2021 private equity market boom, near-zero interest rates were a key factor driving the kind of supercharged returns witnessed during the period. Not only was leverage cheap due to low-interest rates, but the stock market was also booming, driving investor appetite for pricey IPOs.

Although the Fed is embarking on a new rate-cut cycle, we do not expect interest rates to return to zero unless there is another economic crisis. Thus, there is some uncertainty as to how private equity funds will perform if the Fed pauses and keeps rates on hold at a neutral of around 3.5%.

Nonetheless, we believe that the deep discount on Carlyle’s stock more than compensates investors for these risks.

In Conclusion

Accordingly, we are upgrading our rating on Carlyle from “Sell” to “Strong Buy” to capitalize on the deep discount on Carlyle’s share price relative to its peers. We expect this valuation gap to close quickly and anticipate a forceful rebound in Carlyle’s share price over the coming weeks.

Read the full article here