Introduction

Against the backdrop of the recent events surrounding Spire Global (NYSE:SPIR), I decided to write a short update putting the developments over the last three weeks into perspective laying out what this could mean for present and future shareholders. For a more comprehensive analysis, readers should refer to my previous article about this small satellite firm.

Admittedly, not being able to file quarterly results on time always generates fear amongst the investment community, even more so if the company in question has a SPAC history and already suffers from a disastrous share price performance. In the small-cap universe, you cannot expect retail investors to “see through things” and fully grasp the effects of this accounting issue, but I was a bit surprised by the reaction of one of the main sell-side firms covering the stock, namely Raymond James. Even though they acknowledge that “these restatements have no impact on Spire’s cash flows”, the firm decided to partially suspend its coverage, no longer offering a target price – I mean, these analysts always talk about their sophisticated discounted cash flow models. They “believe this will be a continued overhang, particularly with investors not having the correct go-forward financials in hand”, and “find it hard for Spire shares to outperform in that period”. Having read their entire report, it seems they are struggling to understand the accrual-based accounting (i.e., GAAP) and are unwilling to form a view on the potential impact of a restatement of the past financial accounts.

To be fair, Stifel, on the other hand, sees no material impact on Spire’s share price despite this imminent revenue restatement and maintained its buy rating, accompanied by a price target of $20.00/share.

However, I still think a more comprehensive analysis is warranted, which I will attempt to provide in the following report. In my opinion, investors with a decent risk appetite might want to seize this opportunity to build a stake in a rapidly growing satellite company with highly attractive unit economics.Finally, it needs to be mentioned that I had some exchange with the company since these events started to unfold, and many findings/ statements contained in this report have been confirmed by them – notwithstanding the fact that I view the current management team very critically.

Much noise about nothing – or what happened exactly?

Before delving into the intricacies of the arcane world of accrual-based accounting, a depiction of the sequence of events over the past few weeks is probably warranted.

The whole story started on August 14 after market close, when Spire was expected to release its Q2 earnings, as had been announced by the company about three weeks prior. Instead, exactly when investors were awaiting the 10-Q filing, it published a Form 12b-25 stating that they were unable to file their quarterly report for the quarter ended June 30, 2024, on time. The reason for the delayed earnings release was explained as follows (emphasis added by author):

The Company is in the process of reviewing its accounting practices and procedures with respect to revenue recognition related to certain contracts in its ‘Space-as-a-Service’ business (the ‘Contracts’) under applicable accounting standards and guidance. The re-evaluation relates to the potential existence of embedded leases of identifiable assets in the Contracts and the related recognition of revenue for pre-space mission activities. […] While the Company’s review is ongoing, at the time of filing this report, the type of Contracts that the Company has identified for re-evaluation resulted in recognized revenue of approximately $10 to $15 million on an annual basis.

In addition, Spire mentioned in the release that “depending upon the results of this review, it may be required to restate or revise its previously issued financial statements.” Not surprisingly at all, the statement also contained a reference to its sole lender, Blue Torch Capital, saying that the company believes it is not in compliance with the leverage ratio financial covenant under the financing agreement as of the end of June (apart from its failure to deliver financial information on time).

I believe it was not so much the actual risk of a potential restatement of between $10 and $15 million p.a. of previously recognized revenue, which would be proportionally spread over the next three to four years in a worst case scenario, that spooked investors and triggered a sell-off in the company’s stock of close to 40% over the subsequent two days, but rather the mention of another covenant breach under the loan agreement. For those unfamiliar with the history of the firm, this might have seemed like a serious threat, putting the survival of Spire at risk. I will explain later in this article as to why long-term followers of the stock should have known better.

Interestingly enough, many followers probably missed an obvious yet important aspect in the company’s statement: namely that the re-evaluation of its revenue recognition will not impact its statements of cash flows for any period. The cash flow effect will also be covered later in this article.

About two weeks later, on August 27, the company provided an update regarding the review of the discussed space service contracts and the related revenue recognition. In a nutshell, in coordination with its auditor PwC, Spire concluded (emphasis added by author):

that its accounting for [certain contracts in the Company’s ‘Space-as-a-Service’ business], including primarily revenue and cost recognition timing for pre-space mission activities, need[s] to be revised to remove certain previously recorded pre-space mission activity revenue from the period in which pre-space mission activities were performed under the Contracts, and instead, record that revenue over the period in which data is delivered.

This means, effectively, that the financial statements for the fiscal years 2022 and 2023, as well as for the first quarter of 2024, which are the affected periods, will need to be restated. In this release, the company confirmed once again that (i) the annual recognized revenue up for discussion amounted to $10 to $15 million and (ii) the annual cash flows would not be impacted by the new accounting treatment – no big surprise here.

Two days after this press release, on August 29, Spire announced that it had entered into a waiver and amendment to its current financing agreement with Blue Torch Capital – again, no big surprise here. In summary, both parties agreed on the following aspects:

- Blue Torch waives its rights under the financing agreement arising from the two covenant breaches

- Amendment of the financial covenants to provide immediate covenant relief

- Spire must pay (paid-in-kind) an amendment fee of 3.5% of the outstanding principal

- In addition, it also needs to pay off $10 million of its outstanding term loan

Though I hadn’t expected a much different outcome, I believe it’s quite noteworthy that Blue Torch required only minor compensation for the waiver and amendments – less than $4 million (approx. $105 million times 3.5%) – and the agreement even allows for a reduction under certain refinance or pre-payment scenarios in the future. Hence, we can conclude that Blue Torch is either a very generous debt provider or they view this upcoming restatement of the financial accounts and the correspondingly lower EBITDA figures in the short term as a big nothing-burger.

Following up on this assessment (or do we all have a do-gooder worldview?), the next section is intended to provide some – perhaps illustrative – guidance as to how the income statement will be impacted as a result of this different accounting treatment.

What does this all mean in the accounting arena?

One might ask as to why this accounting issue has arisen now, specifically for an interim report, and apparently also at short notice – after the company has undergone two annual audits for the affected periods. Obviously, I cannot answer this question, but perhaps the company will comment on this matter at some point.

Before delving into my financial model, I believe a bit of background information is probably warranted.

In addition to providing data solutions for customers in the maritime, aviation and weather segments based on its proprietary constellation of multi-purpose nanosatellites, Spire also offers “Space-as-a-Service” through its space services solution. Revenues derived from its own satellite constellation represent subscription fees and are recognized over time, with individual contracts generally ranging from one to two years. In contrast, customer arrangements in the space services segment typically include the delivery of specific performance obligations. As stipulated in the revenue recognition standard ASC 606 (Revenue from Contracts with Customers), for the space services business, the company has recognized revenue as project-based deliverables are completed during the pre-space portion of the contract. This approach to revenue and expense recognition has also been comprehensively described in the last 10-K:

Certain of our contracts contain multiple project-based solutions and services promised to a customer over various phases (e.g., scoping, development, manufacturing, testing, launch, and/or satellite operations), which we assess at contract inception to determine which of the solutions and services promised in a contract are distinct in order to identify individual performance obligations. […] The relative standalone selling price (“SSP”) of each obligation […] is generally estimated using cost plus a reasonable margin based on value added to the customer.For certain project-based performance obligations, we recognize a portion of our revenue over time using the output method, specifically contract milestones, which we have determined to be the most direct and reasonable measure of progress as they reflect the results achieved and value transferred to the customer.

Now, the discussion centers on whether some of these large space service contracts contain a specific lease component (“embedded lease”) that would require a different accounting treatment than stipulated under ASC 606. According to ASC 842, “an arrangement includes an embedded lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration. A customer has the right to control the use of an identified asset if it has both (a) the right to obtain substantially all of the economic benefits from use of the identified asset and (b) the right to direct the use of the identified asset.”

Without defending management here, even PwC concludes that embedded leases continue to be a topic of discussion as companies still face complexities with identifying, recognizing and accounting for embedded leases. I was told by the company that the contracts under review address certain payloads for specific space services satellites and that a potential change in the contract language might be the way forward without adversely affecting the customer’s economic position.

The following analysis assumes that the contractual assets in question will be classified as an operating lease according to ASC 842 – a conservative but likely outcome – which should result in the following principal effects on the financial statements (in contrast to ASC 606):

- During the construction phase (i.e., pre-space phase), no revenue is recognized as the customer does not derive any benefits until the asset is completed and operational

- Costs incurred during the manufacturing process will be capitalized as an asset under construction and not expensed

- Cash flow will be unchanged, and the respective contractual payment obligations will lead to a deferred revenue position on the balance sheet

- Once the data provision phase begins, the former pre-space revenue will be treated as lease income and recognized on a straight-line basis over the remaining contract term, in addition to the ordinary (unchanged) revenues stemming from the company’s data provision and satellite hosting services

- The previously recognized asset, i.e., costs to build and launch the customers’ satellites, will be depreciated over the lease term

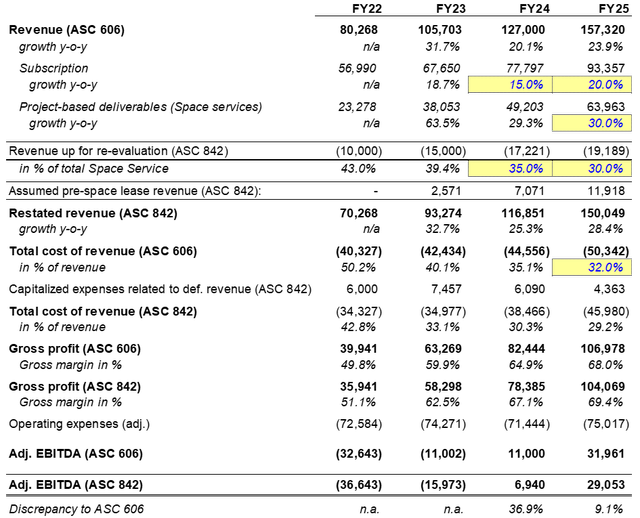

The following income statement aims to illustratively contrast the – presumably – prospectively applicable standard ASC 842 for the contracts under review with the previously applied revenue recognition approach under ASC 606.

As we have been given a range for the historically recognized revenue of $10 to 15 million annually on the contracts under review, the lower bound is used for FY22 and the higher one for FY23. In addition, my model assumes that the contracts in question will generate growing revenues over time, more specifically in FY24 and FY25. Next, expenses relating to the previously recognized pre-space revenue are capitalized and only expensed when the corresponding revenue is recognized. My model assumes a gross margin of 40% for this revenue portion, based on the company statement that gross margins are significantly higher during the data provision phase and that they aim to price their contracts in the 70% gross margin range.

To determine the timing of revenue recognition concerning these pre-space milestones within the large contracts, an evenly distributed order flow on a quarterly basis over the observation period has been modeled. More specifically, it is assumed that each project requires five quarters to design, construct, and launch the satellites, followed by a data provision phase spanning 3.5 years. The results are reasonably robust irrespective of my assumptions about timing and the number of individual projects.

Source: Own calculation based on 10-Q and 10-K filings from Spire Global

The financial projections for FY24 are based on the mid-point of the management guidance published with the Q1 earnings release. At the mid-point, Spire expects to grow its revenues by roughly 20% to $127 million. The total cost of revenue is assumed to grow by the previous year’s rate of 5% – rather conservative given that revenue growth is expected to decelerate by a third. This would implicitly mean that adjusted operating expenses would come in at $71.4 million, representing a y-o-y decrease of nearly 4%. This looks quite achievable if you consider Spire’s Q1 results – total operating expenses adjusted for stock-based compensation decreased by nearly 17% in the first quarter of FY24.

Combining my assumptions with this year’s mid-point management guidance, the new adj. EBITDA for FY24 would be around $7 million, as opposed to the projected $11 million based on the original accounting treatment. Assuming a growth rate of 20% and 30% for the subscription segment and the project-based business, respectively – keeping in mind, management intends to grow annually at over 30% over the next couple of years – my financial model projects an adj. EBITDA for FY25 of approx. $29 million. Assuming the company will be free cash flow positive beginning this summer, as management has continuously mentioned over the last few months, an investment in Spire, which has a market cap of slightly more than $200 million, looks quite appealing.

Finally, I believe it should be highlighted that the discrepancy resulting from the potentially new revenue recognition will be almost immaterial from FY25 onwards regarding the adj. EBITDA – due to the phasing effect of this change.

But what about NorthStar, Blue Torch Capital, or cash flow in general?

The following section is intended to clear up some common misconceptions surrounding this accounting issue.

1) The much-talked-about NorthStar incident is entirely unrelated to the current accounting review (or the likely restatement of prior financial accounts) – and yes, this has been confirmed by the company. Regarding the publicly available article describing NorthStar’s attempt to get a court injunction to stop Spire from shutting off the flow of data, I tried to get some feedback from the company. However, given that this is an ongoing legal proceeding, they couldn’t share much detail with me. Having said that, readers should be reminded that this article only describes the position of one party trying to argue its case. Nonetheless, this report shows that there has been an ongoing dialogue to negotiate a commercial solution. Additionally, there are a few noteworthy insights that need to be highlighted:

- Spire earned $14.5 million in up-front fees for the building and launch of four satellites; and theoretically sees a revenue potential of around $200 million with NorthStar, based on the firm’s own plans for an expanded constellation

- Even at a rate of 25% of the originally intended performance, the retrieved data was good enough to continue NorthStar’s R&D efforts and satisfy its customers, including the U.S. Department of Defense

- In principle, Spire is committed to replacing the defective satellites, but it would take longer (up to two years) than stipulated in the agreement; perhaps it is currently busy building other satellite constellations – wouldn’t that be a good thing?

Ultimately, giving all parties the benefit of the doubt here, I still believe they will come to an amicable arrangement allowing for further collaboration.

2) Admittedly, the terms – i.e., interest rate and covenant regime – stipulated in the original loan agreement with Blue Torch Capital hadn’t been very favorable for Spire. However, this management team agreed to these conditions back then – it takes two to tango. Following the commencement of this contractual relationship, Blue Torch has tolerated many missteps (i.e., covenant breaches) by continuously amending the covenants and waiving its rights under the financing agreement. As a result of these repeated covenant breaches and the related remedies, Blue Torch currently owns more than one million warrants at an exercise price of $5.44 per share. Hence, Spire’s only debt provider is virtually also among the largest shareholders of the company. I believe the interests of debt and equity providers cannot be more aligned than this. That’s why I have consistently mentioned that there was never a serious bankruptcy risk here. In addition, Blue Torch – what I like to call the adults in the room – has also grown its influence within the firm, as evidenced by Spire cutting back its SG&A expenses significantly over the last few quarters, alongside a subtle strategy shift towards larger projects at the expense of smaller tickets and less valuable customers.

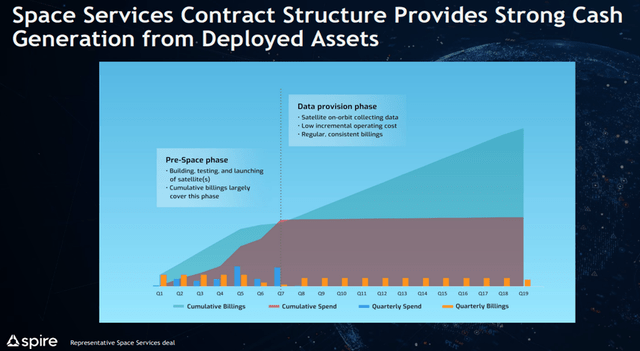

3) The last aspect that needs to be addressed relates to the cash flow topic. It goes without saying that an accrual-based accounting standard doesn’t impact the characteristics of the individual customer contract. Hence, space service customers will still have to pay based on the contractually agreed billing intervals, and the total payments will still amount to the total revenues to be recognized – irrespective of any future accounting treatment. As far as I remember, a proper discounted cash flow valuation is supposed to incorporate future cash flows, or in other words, “Cash is king” as the proverbial saying goes. Finally, I would like to bring the readers’ attention to a slide that was shared during the Q4 earnings call at the beginning of the year. It depicts the cash flow profile of an illustrative space service contract (billings shouldn’t be confused with recognized revenue, just to be clear). This slide showcases that Spire’s space service customers must finance all the manufacturing and launch costs occurring during the pre-space phase in advance. Thus, these customer contracts are cash flow positive at each point in time – a rare case in the world of long-term customer contracts, as far as I can tell. Obviously, the exciting part begins with the inception of the data provision phase, where the incremental cash expenses are quite low.

Source: Company presentation – Q4 2023 Investor Update

Can this be a transformational deal?

Now, let’s get to the interesting part of this article. In June, Spire announced that it would join forces with Thales and European Satellite Services Provider (ESSP) to develop a satellite constellation and offer new space-based surveillance services for Air Navigation Service Providers. In this potentially transformational deal, Spire will be responsible for the development of the space segment, including system design, building the 100+ satellite constellation and payloads, ground control, and data collection, leveraging their nearly decade of expertise in developing and operating ADS-B payloads in space. To allow for a true end-to-end system that fulfills all the rigorous requirements set by the International Civil Aviation Organization, Thales – one of the largest defense & security companies in Europe – will provide the ground air traffic management system and the service supervision infrastructure, while ESSP will manage the certification and delivery of the service for air traffic surveillance purposes.

The first phase of this project has been funded and has already kicked off to determine mission and system-level requirements for the space segment. Typically, in these larger projects, there are three main phases: a) design & development, b) building & launch of the satellites, and c) operation & data provision. Their objective is to have the service operating by 2027, so satellites would need to be built and deployed by that time.

As there haven’t been any award values disclosed, I followed up with the company regarding this project. They directed me to look at what Aireon spent on payload development and hosting costs on the Iridium constellation to help size the scale of this opportunity. According to two public articles, Aireon paid:

i) Harris nearly $115 million to build the ADS-B payloads,

ii) Iridium a hosting fee of $200 million for the integration and launch of the ADS-B payload, and

iii) Iridium another approx. $300 million over 15 years for recurring data communications service fees.

The company confirmed that these efforts would be of a similar nature (ADS-B payloads and having the payloads in space) as to what Spire is providing. That would mean this project might generate a recurring revenue stream of around $40 million per year ($615 million / 15 years). As the constellation’s satellites are designed to be replenished every five years, ensuring the system offers the latest and most advanced technology, there is likely a timeframe in which there is some overlap between the data provision portion of the first constellation and the pre-space phase of the second constellation, resulting in additional revenue upside beyond my simple calculation.

Now the question is: how many deals of this type – outside of the field of weather forecasting – are potentially out there? In this respect, I would like to highlight that there is also the EURIALO project, where the European Space Agency has awarded Spire a €16 million phased contract to develop the preliminary design for a global space-based aircraft surveillance system aimed at geolocating planes independent of “jammable” GPS technology. The economic significance of this project – assuming it reaches the final phase – has already been addressed in a previous earnings call.

Conclusion

Potential investors need to make up their minds whether they want to get carried away by a new set of accrual-based accounting rules that affect a small portion of the business or, alternatively, focus on the cash flow generation capability of this company and the massive – yet somewhat abstract – untapped potential that may lie ahead. Even though some time will likely pass before the company releases its restated financials, I believe investors who are willing and able to navigate the intricacies of the accounting universe are presented with a highly asymmetric bet where the potential rewards substantially outweigh the risks. Finally, investors shouldn’t forget that Spire was able to raise approx. $30 million – representing 15% of its current market cap – from institutional investors at a price of $14/share in March 2024.

Read the full article here