Procept Biorobotics (NASDAQ:PRCT) has been one of the strongest performers in the medical device space over the past year. The company has a novel product providing relief to older men suffering from BPH – benign prostatic hyperplasia. The minimally invasive procedure is seeing strong growth as both system sales and procedures grow significantly. I wrote about the company in May 2023 when it traded at $31.40 – a 142% gain since. Procept still has good potential with a new and improved system named HYDROS now FDA approved, allowing for another leg of growth in the quarters to come. While PRCT has good potential, it is still at a small scale and trading a premium valuation, giving it high risk into 2025. Let’s dive into the recent results and new approval potential for Procept.

Improved AI-powered Hydros System approved

The company took their time working on the system, with knowledge gained in 50,000 procedures to improve any point points a doctor may have. The product has AI powered FirstAssist technology to create a procedure plan. The image has been improved, and the steps have been streamlined to make it easier for physicians to use effectively. The FDA approved the platform on August 21st allowing the company to begin seriously selling the product. Unfortunately, we don’t have exact release details since the approval was after the recent earnings call in August. However, you would hope the launch would be rolling significantly in 2025 and help significant 2025 revenue growth. Current estimates are for 40% revenue growth in 2025, which is already a high bar to clear in a difficult operating environment. However, Hydros could allow for upside to this number, with 2026 likely to see even stronger growth as a result.

At the Wells Fargo conference on September 4th, management pointed out the significant improvements in features. The launch will not have a negative impact on gross margins. The initial strategy is to focus on 2700 greenfield hospitals in the US that do therapy and not replace older systems. 860 of those hospitals do 70% of the volume, and PRCT expects to be in almost all of those hospitals in the coming years. The system will cost $380,000 in the second half of 2024 with that to increase potentially in 2025. New surgeons should be willing to come onboard over the first system due to the improvements, helping to improve usage. Q3 will have some small disruption as sales reps are trained on the new system with Q4 mostly at full speed of sales. Overall the improved system will mostly be a big tailwind to 2025 with most of the legacy systems to remain in place with growing usage.

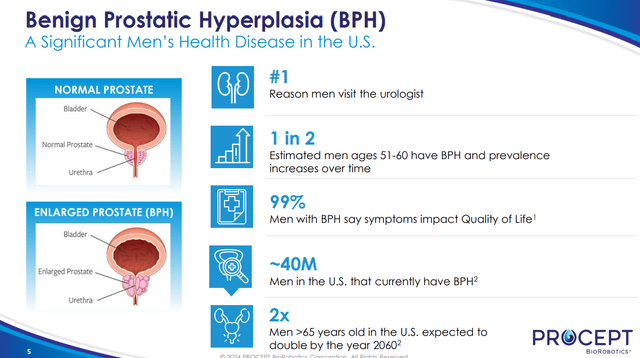

BPH in Men (PRCT IR)

Q2 – Continued hypergrowth

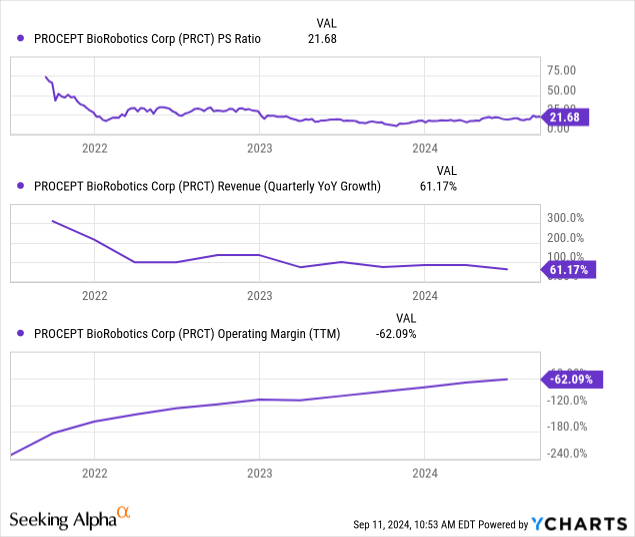

Procept has continued to scale its business quite quickly, with impressive revenue growth. They continue to sell their current Aquablation system with a strong cadence, with 47 sales of new systems in the quarter. The placement of systems is essential to the higher margin sales of handpiece revenues, making it the best leading indicator of future growth. Last year, they sold 40 in Q2, for a growth rate of 17.5% y/y in new systems. Consumable revenue was up 101% y/y, but the base is still quite small with $27.3m revenue. 8000 hand pieces were shipped in Q2, with a 15% increase in system utilization y/y. This should improve drastically with HYDROS as newer physicians will be drawn to the easier to use interface, superior technology and ease of use through AI assist. As procedure volumes at each system placement increase, revenue will continue to scale along with margins. Total gross margin is up to 59%, up from 56% from 2023 on the improved mix of procedures versus system deployments. On the downside, due to the continuing ramp of sales and marketing, the company is making significant losses with -62% operating margin improving over time. Long term, the company is attempting to treat prostate cancer, with potential for a big market there if they can succeed in their current clinical trial on their older Aquablation system.

Risks

Procept is small with only one area of expertise at the moment with its BPH products focusing on large unmet need. The large TAM with many men experiencing issues with their prostate gives the company significant runway in this first indication. However, after that, the next area for the company remains unclear and will remain so for several years. Also, the company is still making sizable losses as it grows its research and sales organizations to support future growth. The company has $214m in cash on hand, with a 2024 loss expected to be $97.5 million. However, some of that is dilution through stock-based compensation to a reasonable number of employees to fuel growth. A future equity dilution to raise additional cash is possible, especially with the high cost of a debt issuance for a smaller company right now. This does put a potential damper on shares at some point in 2025 as a possibility.

Hold – Procept shares fairly valued

Procept shares saw a significant boost after HYDROS was approved, with excitement from the street on the next leg of growth. The long-term potential could improve if prostate cancer ends up a potential market down the road. Shares are now trading near all-time highs with a price of $76 pricing in strong growth in 2025 of 40%. Hydros adoption should give potential upside to the guidance next year, but sales changes could cause disruptions as well in coming quarters. However, long-term scaling of the business is the biggest question, and the current valuation does not leave much room for error at the current price. We have seen other companies in the medical technology space see their multiples contract significantly once they reach the $300 to $500 million mark. Thus, I have the shares at a hold at the current time, until a pullback occurs to give investors a more favorable entry price.

Read the full article here