I last covered FS KKR Capital (NYSE:FSK) back in early March after the stock had dipped quite sharply. At the time, I asked and answered the question of whether it was worth buying the dip, and my conclusion was yes. Since then, the stock has returned 6.63% to shareholders, slightly outperforming the S&P 500, which delivered 5.48% over that period of time, thereby validating my buy call. In today’s article, I am going to revisit the FSK thesis and compare it to the leading BDC sector blue chip, Ares Capital (ARCC), to see which one of these is worth buying right now.

FSK Vs. ARCC: Investment Portfolios

When it comes to their investment portfolios, FSK is more defensively positioned with 58.1% in 1st lien senior secured loans and 6.6% in second lien secured loans, whereas ARCC has just 50% in 1st lien senior secured loans and 12% in second lien senior secured loans. This gives FSK greater total exposure to senior secured loans as well as a greater focus on first lien loans. On top of that, FSK has 14.4% invested in asset-based finance loans, which are arguably an even more conservative position in the capital stack than first lien senior secured loans. Moreover, its 9.8% invested in joint ventures is almost entirely conservatively positioned investments, with 76% of it in first lien loans and 3.8% in second lien senior secured loans, while an additional 12.9% is invested in asset-based finance loans.

As a result, when you combine its senior secured loans and its asset-based finance loans, nearly 90% of its portfolio is invested in these secure, more defensive areas of the capital stack, whereas with ARCC, only 62% is invested in first and second lien senior secured loans with no asset-based finance loans to speak of. It also has 8% invested in Ivy Hill Asset Management, which likely has some senior secured exposure in it, but even if you count all of that towards senior secured loans, its overall senior secured/asset-based investment composition in its portfolio is much lower than FSK’s.

Both BDCs are also very well diversified and have large portfolios, with FSK’s investments spread across 208 individual investments and ARCC’s spread across well over 500 companies. The median leverage ratio with companies in their portfolios is 6x for FSK and 5.7x for ARCC, indicating that ARCC’s counterparties are a bit stronger financially, but not by much. In terms of interest coverage ratio, both have 1.6x, which, though on the weaker end of their historical averages, remains adequate and does not indicate an impending spike in non-accruals for either of them. Speaking of non-accruals, FSK’s have seen an improvement recently, sitting at 1.8% of fair value, whereas ARCC’s remain quite strong at 0.7% of fair value.

FSK Vs. ARCC: Management Quality

It is important to keep in mind when assessing the forward outlook for the businesses that both are backed by some of the top alternative asset managers in the world, as ARCC is backed by Ares Management (ARES) and FSK is backed by KKR (KKR), giving both significant teams and resources for conducting underwriting, recoveries, and workouts on their investments.

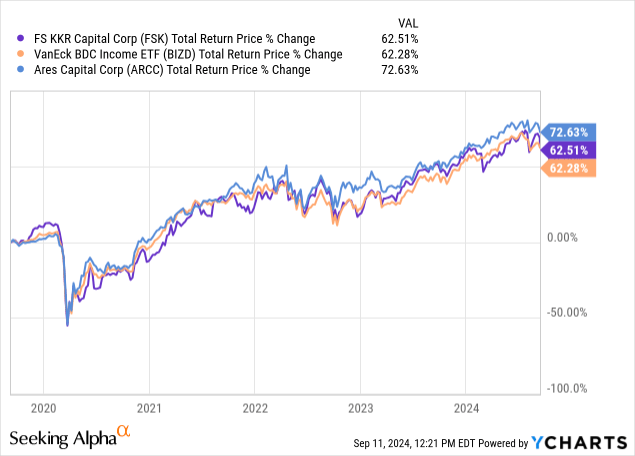

ARCC’s track record is one of the strongest in the public BDC space (BIZD) as it has crushed the sector and S&P 500 over time, whereas FSK’s total return track record was very poor prior to KKR taking over the fund and has been mediocre since. However, it is important to note that the vast majority of FSK’s non-accruals and underperforming investments have been due to investments made under the prior manager, as the investments underwritten by KKR have actually performed quite well on average. Still, ARCC’s superior track record does earn it some points, but it is also worth noting that over the past five years, while ARCC has meaningfully outperformed the broader BDC space, FSK has still kept pace and even slightly outperformed the broader BDC space over that time period.

FSK Vs. ARCC: Interest Rate Sensitivity

When it comes to their exposure to interest rates, both are expected to suffer 7.5% headwinds to net investment income if the Federal Reserve cuts interest rates by 100 basis points. So, both are fairly in the middle of the pack compared to many of their peers in terms of sensitivity to fluctuations in short-term interest rates.

When it comes to their balance sheet strengths, both have a meaningful amount of debt maturing through the end of 2025, though both are fairly well-positioned with the vast majority of their debts maturing in 2026 and beyond. Both also have enormous amounts of liquidity, as FSK has $4.7 billion in liquidity, and both have billions of dollars in liquidity. FSK’s net debt-to-equity ratio was 1.09x as of the end of the last quarter, while ARCC’s was 1.06x, putting them at virtually identical levels.

FSK Vs. ARCC: Valuations

When it comes to the fee structure, both of them have 7% performance fee hurdle rates, but their fee structures are somewhat different. Both businesses have 1.5% base management fees, but FSK has a 17.5% performance incentive fee that kicks in after the 7% hurdle rate is crossed. Meanwhile, ARCC has a 20% income-based fee that kicks in after the 7% hurdle rate is crossed, as well as a 20% capital gains fee. This makes ARCC’s fees overall meaningfully higher than FSK’s during periods of strong returns.

In addition to ARCC’s management fees being higher than FSK’s, when the comparison comes down to valuation, this is where FSK shines relative to ARCC. For the next 12 months, FSK is expected to pay a 13.8% dividend, whereas ARCC is expected to pay just a 9.4% dividend. On a valuation basis, ARCC trades at a 5% premium to its net asset value, whereas FSK trades at a nearly 20% discount to its net asset value. Historically, FSK has traded roughly in line with its net asset value. This indicates ARCC is overvalued, despite entering a period in which credit underwriting and interest rate cuts are likely to provide headwinds to the sector, whereas FSK has been deeply discounted due to its checkered past performance. This discount seems to ignore the positive impact that KKR is having on the performance of the portfolio, the outsized dividend yield it offers, as well as its lower fees compared to ARCC.

FSK Vs. ARCC: Investor Takeaway

Overall, I would say ARCC’s track record is significantly better, and its portfolio is performing a little better than FSK’s, while FSK’s portfolio is more defensively positioned against a material economic downturn, and its overall underwriting performance is improving as KKR continues to work through the issues in the legacy portfolio from the previous manager and underwrite more loans of their own. Both ARCC and FSK are similarly positioned in terms of balance sheet strength and sensitivity to potential interest rate cuts by the Fed.

Keep in mind that FSK has outperformed the broader BDC space over the past five years, so to suggest that it deserves to trade at such a deep discount to NAV, despite having pretty average management fees for the sector, a well-diversified and fairly defensively positioned portfolio, and a very attractive dividend yield, does not make sense.

As a result, I rate FSK as a strong buy right now and ARCC as a hold.

Read the full article here