Note: I previously covered Teekay Tankers (NYSE:TNK). My 1Q24 article discussed Aframax/Suezmax market dynamics, TNK fleet, and company financials.

I liked TNK’s clean balance sheet, LTV below 10%, Aframax/Suezmax fleet, and reasonable valuation at 89% PNAV. One drawback is fleet age; TNK ships are 14.7 years old. Dividend yields are not impressive compared to other tanker owners. In summary, TNK’s strengths compensated for its weaknesses, and the company found a place in my portfolio.

The company’s share price peaked at $73.8/share in May but retraced to $52.1/share in the following months. This was due to the seasonal weakness of day rates. Anyway, TNK is not part of my portfolio anymore. I consider VLCC ship owners a better proposition considering market fundamentals. In today’s article, I discuss 2Q24 results and TNK rating.

Introduction

Teekay Tankers has the best balance sheet in the tanker game. Currently, the company has 4% LTV. Minimal debt is great, yet it comes with its price—an aging fleet. TNK’s average fleet age is 14.7 years, way higher than its competitors. Another drawback is the lack of scrubbers. None of the TNK vessels have EGCS, a glorified name for the scrubber, which means Exhaust Gas Cleaning System.

The last company’s report is neither bad nor good. TNK reported $3.11 EPS in 2Q24 vs. $4.23 in 1Q24. On the other hand, operating and FCF increased by $17 million and by $7.0 million QoQ. Another positive change is TNK’s fleet updates. The company has sold two vessels built in 2005 and purchased one built in 2021.

Macro tailwinds are still supporting the tanker thesis. Nonetheless, not all tankers are equally appealing. The VLCC segment brings more growth potential than Suezmax and Aframax.

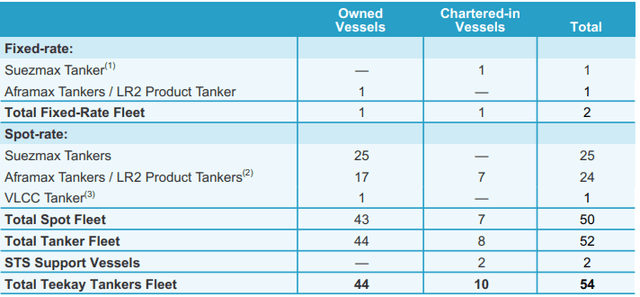

Fleet

TNK fleet consists of 25 Suezmax tankers and 17 Aframax. Additionally, the company owns 50% of VLCC Hong Kong Spirit. 96% of the fleet is employed under spot contracts.

The table below from the 2Q24 report shows TNKs’ fleet status.

TNK 2Q24 report

2Q24 fleetwide figures: $44,758/day TCE, $8,523/day OPEX, and $15,000/day breakeven cash flow.

Despite its aging fleet, TNK keeps its daily operating expenses competitive. For comparison, NAT (a Suezmax-only company with a fleet average age of 12.7 years) reported $9,000/day OPEX.

TNK excels in breakeven cash flow, $ 15,000/day is significantly lower than most companies in the crude tanker segment. Frontline Plc (FRO) reported $25,700/day 2Q24 breakeven cash flow, and DHT Holdings (DHT) $23,600/day. The reason for that stark contrast is TNK’s balance sheet. The company has 3.8% Total Debt/Equity and 4% LTV. For reference, DHT has 21% LTV and FRO 48% LTV.

TNK also operates charted-in vessels. I am not a big proponent of chartering additional ships, especially in a market with not-so-good fundamentals like the Suezmax and Aframax segment. In my opinion, hiring extra ships works best in markets with apparent deficits like the VLCC or Capesize segments. In those cases, the chartered-in ships add extra leverage.

The company has seven chartered-in Aframax/LR2 tankers and one Suezmax. Aframax vessels have a dual purpose. They can carry clean and dirty oil cargo, which means they follow different market dynamics compared to VLCC and Suezmax.

TNK sold two 2005-built tankers, one Aframax and one Suezmax, for $64.8 million in gross proceeds. The vessels are expected to be delivered to the buyer in 3Q24. TNK reported a realized gain of $27 million from both sales. In June 2024, TNK agreed to purchase one 2021-built Aframax vessel for $70.5 million.

In summary, the TNK fleet is competitive, given its daily OPEX and breakeven-free cash flow. Plus, a fleet upgrade is a step in the right direction.

TNK 4Q23 report

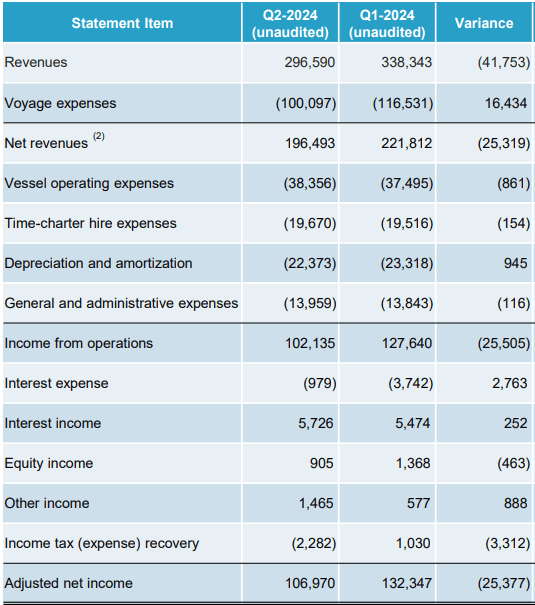

The following table shows 2Q24 results.

TNK 2Q24 report

In 2Q24, TNK reported $296 million in revenues, 12% lower than in 1Q24. Vessel operating and charter-in expenses remained nearly unchanged. In 2Q24, TNK realized $102 million in operating income, compared to $127 million in 1Q24. EPS was disappointing. 2Q24 EPS is $3.11/share vs $4.23/share in 1Q24.

Now, the good news. TNK reported QoQ rising operating and free cash flows. For 2Q24, the company realized $146 million in operating cash flow and $136 million in FCF.

Below is a quote from 2Q24 presentation about company’s FCF generation abilities:

As a reminder, for every $5,000 increase in tanker rates above our free cash flow breakeven of $15,000 per day, we expect to generate approximately $2.36 of annual free cash flow per share.

TNK reported $426 million in cash and $287 million in undrawn credit facility. The company has $63.7 million total debt, so interest expenses are almost non-existent, resulting in a net interest income of $4.7 million for 2Q24.

Impressive numbers. The question is what the company will do with its spare firepower. It has a few options: boost dividends, start buybacks, renew its fleet, or do nothing. Given that TNK stocks trade below 100% PNAV, I would like to see proactive share buybacks.

Fleet upgrades are another viable option for allocating capital. At that point in the tanker cycle, purchasing a few-year-old vessel delivered in a few weeks/months is better than purchasing a brand-new one with an expected 12–18-month delivery. The second-hand tanker will start generating cash flow immediately, plus inflation will do its magic, increasing the company’s NAV. Otherwise, the shipowner must commit massive front payments to a shipyard with the hope that when the ship is delivered, the market will be strong.

TNK pays dividends with a 5.52% LTM yield, which is mediocre compared to other tanker owners. For 2Q24, the dividend payment is $0.25/share, resulting in a 15% LTM payout ratio.

As pointed out, TNK generates massive FCF and maintains an impressive balance sheet. So, boosting dividends or starting a share repurchase program would attract more investors. I would focus on share buybacks. In that way, the company boosts dividend yields simply by cutting the number of outstanding shares. More fleet upgrades would be nice, too.

TNK Valuation

To estimate TNK NAV, I use data from Fearnley’s weekly reports. Inputs for the NAV equation are:

- Fleet replacement value: $1,628 million

- Current assets: $689 million

- Total Liabilities: $184 million

- Total Debt: $63.7 million

TNK’s market capitalization is $1,890 million, while its net asset value is $2,133 million. Hence, TNK trades at 89% P/NAV.

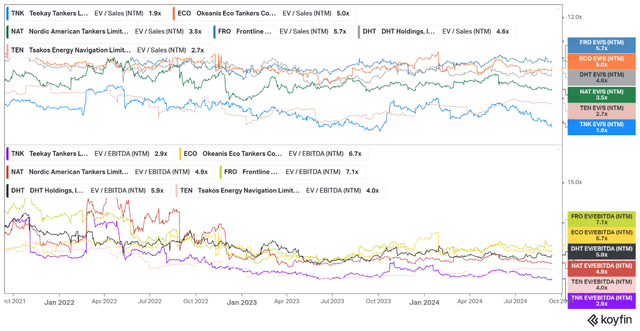

TNK is the bottom fish among large-cap tanker stocks. It is even cheaper than Tsakos (TEN). To be precise, TEN is not a crude tanker-only company. It owns 98 vessels, including crude and product tankers, bulk carriers, containers, and LNG carriers.

Koyfin

TNK trades at 1.9 EV/Sales and 2.9 EV/EBITDA, which is dirt cheap for a company with a 4% LTV and $15,000/day breakeven cash flow. However, TNK has an old fleet and pays dividends with a mediocre yield.

TNK’s strengths are already priced. For share revaluation, we must see an improved shareholders’ return policy and more fleet upgrades. If that becomes a fact, TNK’s shares might reach DHT multiples of 4.6 EV/Sales and 5.9 EV/EBITDA. This means 100% upside potential.

Low multiples are not enough to stay invested. ECO and DHT already offer all I need: top-spec fleets, attractive dividends, and VLCC exposure. Moreover, considering PNAV, TNK is not really cheaper than DHT. The latter trades at 94% PNAV. Meanwhile, ECO trades at higher PNAV and EV multiples, but it brings more value for the price paid.

Investors takeaway

I still like TNK. The company has deleveraged over the past several quarters, started upgrading its fleet, and it trades at low single-digit EV multiples. Yet, this is not enough.

Every company has advantages and disadvantages, and TNK is no exception. Its unattractive dividend yield compared to other tanker operators is a prime reason to change my mind. Plus, I see more growth potential in the VLCC segment than in Suezmax and Aframax. This means that investing in TNK comes with the opportunity cost of not investing in VLCC-focused ship owners.

As investors, we must consider the risk-reward and opportunity cost of every trade. TNK’s opportunity cost outweighs the risk-reward, so I prefer to park my cash with ECO and DHT. In conclusion, I give TNK a Hold rating.

Read the full article here