I last wrote about Organigram (NASDAQ:OGI) here almost three months ago, calling it a great deal. The stock has increased a lot since then, rising from $1.525 to $1.86, a gain of 22%, but I still like it a lot despite outpacing the market. The New Cannabis Ventures Global Cannabis Stock Index has declined 1% since that article, and the Canadian Cannabis LP Index has dropped to a record low, falling 12%.

Organigram represents 12.2% of my Beat the Global Cannabis Stock Index model portfolio that I share with subscribers to 420 Investor. In this follow up, I explain why I still hold it in such a large portion of the model portfolio. I begin with a look at the chart, review the fiscal Q3, which was reported last month, discuss the estimate changes and assess the valuation.

Organigram Has a Great Chart

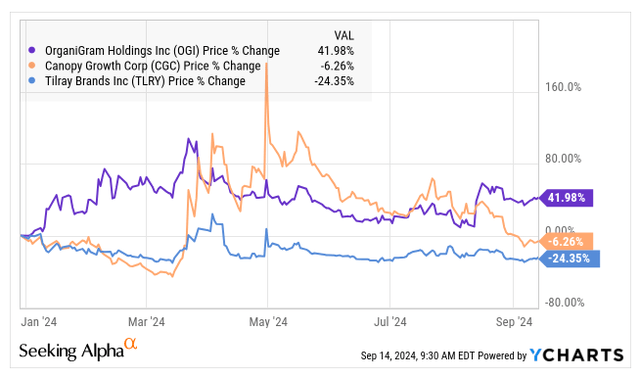

Organigram is up 42% in 2024, which is a lot better than most cannabis stocks. The Global Cannabis Stock Index, of which it is one of the 28 stocks currently qualifying for inclusion, is up just 5.1%. The Canadian Cannabis LP Index has dropped 17.5%. I think that many investors and traders look negatively at stocks that have outpaced their peers. While I don’t generally like stocks that have done so much better than others and prefer to find stocks that have declined more than the market, my three largest positions in the model portfolio are all up more than 31% year-to-date. These stocks currently total 47% of the model portfolio.

The two most popular Canadian LPs are stocks I don’t care for at the current prices, Canopy Growth (CGC) and Tilray Brands (TLRY). These stocks may be weighing on OGI:

YCharts

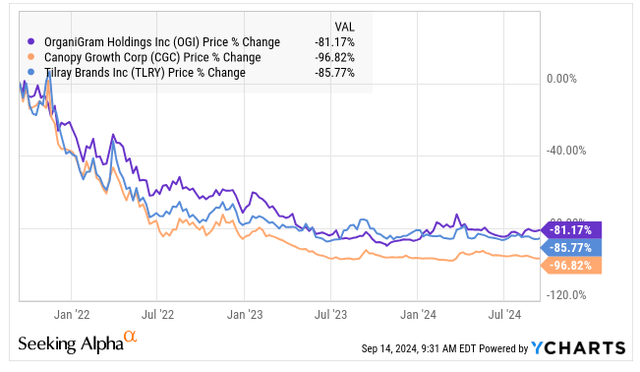

Taking a longer perspective, they are all down a lot over the past three years:

YCharts

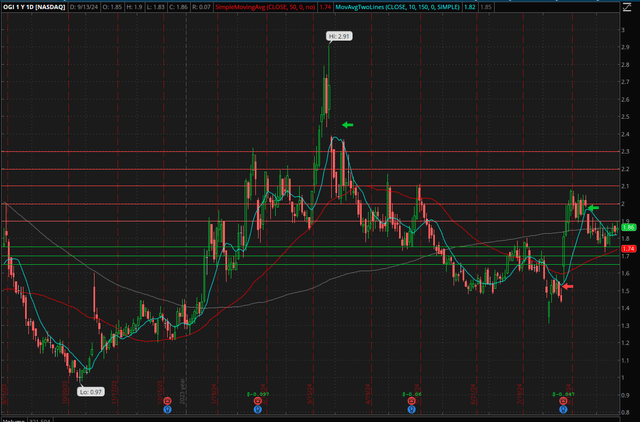

I think the chart for Organigram is very promising. Here is the past year:

Schwab Thinkorswim

The low below $1 almost a year ago was the low of the downturn since early 2021, but it was not an all-time low. The stock shot up in early November last year when its investor, British American Tobacco (BTI) announced it was buying more at a much higher price (directly from Organigram, spread out over time). I had a very large position that I cut in half that day in my model portfolio on the big rally. I did not expect it to fill that gap, though it did. I ended up rebuilding my position as it dipped.

Sometimes it’s better to be lucky than smart, and I was very lucky to have totally exited the name in my model portfolio in late March of this year. The stock plunged on an equity sale, and that gap is still open. I added some back and used the very large dip to rebuild the position. There was a gap up on August 13th due to the earnings report that day, and this gap remains open. More recently, when the DEA announced the December hearing regarding rescheduling, the stock plunged and left a gap that also remains unfilled.

I think the stock is cheap, as I discuss below, and I also am excited by this chart. I think that the gap from 8/27 will get filled, though this isn’t a large percentage gain at this point. I also think that the gap from the capital raise will get filled. I do see resistance at $1.90 and several levels above that price. In fact, this was one of the reasons that I reduced my position in the model portfolio on Friday. I currently see support at $1.75 and a few levels below.

The Organigram Q3 Was Fine

The fiscal Q3 report was expected to yield revenue of C$38 million with adjusted EBITDA of breakeven. Organigram reported revenue of C$41.1 million, up 25% from a year earlier. Adjusted EBITDA was also above what had been expected, as it was C$3.5 million compared to -C$2.9 million a year earlier.

Revenue soared, and the gross margin expanded. There were lower operating expenses (excluding the impairment charge from a year earlier), but there was still a small operating loss. The company burned a little cash in its operations during the quarter and has consumed C$5.0 million through its first three quarters. This is a great improvement from a year earlier, when it used C$21.8 million to fund its operations.

What I like about the company is that it is doing very well in adult-use in Canada, where quarterly revenue net of the high taxes was C$36.5 million, 89% of net revenue. It grew 42% from a year ago. Year-to-date, it is up 12.5%. Almost all of the rest of the revenue is from international operations, as its medical sales in Canada are very small. The international sales expanded at 40% in fiscal Q3 from a year earlier.

Not only were the financials better than the analysts had projected, the cash level was much higher than at the end of fiscal Q2. The company reported cash and short-term investments of $80.1 million, up 136% from its year-end. The press release mentioned a pro forma level of $173 million, adjusting for future payments for stock purchases by British American Tobacco. It did receive C$41.6 million in early September, and it is scheduled to receive another payment in February.

The cash-rich and debt-free company has a tangible book value now of C328.6 million. The current ratio at the end of Q2, now higher, was quite high at 4.3X.

The Analysts Remain Optimistic About Organigram

Ahead of the Q3 report, analysts, according to AlphaSense, were projecting FY25 revenue of C$165 million and adjusted EBITDA of C$5 million, a margin of just 3.3%. Subsequent to the report, they are now looking for revenue to increase 10% to C$176 million. Adjusted EBITDA is also projected higher than ahead of the report, as it is expected to increase 62% to C$9 million, a margin of 5.0%.

The consensus for FY26 has improved for adjusted EBITDA too. On flat revenue, the estimate has increased from C$18 million to C$19 million, a margin of 11.0%. This seems low to me, as revenue could be higher and so could the adjusted margin.

The stock should be trading higher than tangible book value, which is a bit above the current level, and I think that adjusted EBITDA could be 7% of the projected revenue in FY25, which would be C$12.3 million. I am expecting revenue to increase at least 10% in FY26, which would be C$194 million, and for the adjusted EBITDA margin to expand to 15%, which would be C$29 million.

Organigram Has A Decent Valuation

I have been discussing how cheap OGI has been for a while. It was a lot cheaper, but it is still attractively valued. It was trading at a big discount to tangible book value, and it now trades at a small one of 0.9X. I think this is good for a cash-rich and debt-free company that is earning positive adjusted EBITDA!

That metric, price to tangible book value, is more of a defensive measure. Comparing the valuation to the adjusted EBITDA is a better gauge. Ahead of the report, I shared with my subscribers a target for year-end of $1.67 (based on C$2.32, which was an enterprise value to projected adjusted EBITDA for a year ahead of 15X).

With the higher projected adjusted EBITDA and the same ratio, which may be too low, I now get a target for the end of this year of C$2.45 (US$1.80). Again, though, I think that the sales and adjusted EBITDA for FY25 and FY26 could be higher than expected currently. My target is based on the higher numbers I shared above and works out to C$3.07 (US$2.26). $2.26 would represent a gain of 21% by year-end.

A year from now, the current estimates at an enterprise value to projected adjusted EBITDA of 15X works out to C$3.39 (US$2.49), up 34%. If my higher estimate for FY26 ends up being correct, the price would be C$4.64 (U.S. 3.41). While this level seems high and would have to get through the potential exercising of the warrants issued earlier this year at C$3.65, it would fill that gap left behind last March. This price would be below the price near the beginning of 2023 and way below the initial price that British American Tobacco paid for a large stake in early 2021.

Conclusion

Organigram is up a lot year-to-date. The gain is above the index I used to track the cannabis sector, and it stands out relative to other Canadian LPs too. I think that this impedes more from buying the stock, as they fear it could give up some or all of those gains. Of course, like all stocks, OGI could decline. Still, it seems very attractive relative to its peers.

While I like it, OGI is not my favorite cannabis stock right now. It is not even my favorite Canadian LP. Village Farms (VFF) is my largest position in my model portfolio despite rising a bit since I wrote about it in early July, explaining why I like it so much again.

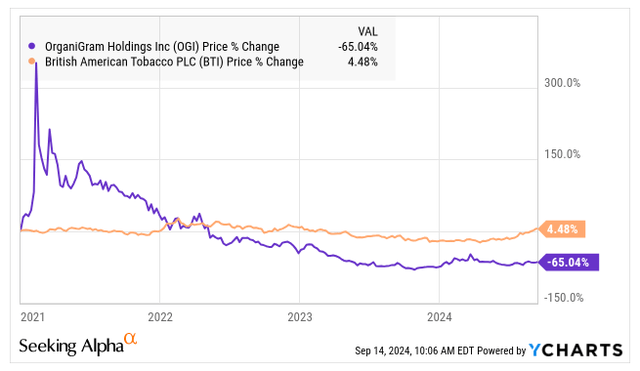

There are some good things that could happen to Organigram that I didn’t cover above. First, and this would be good for all Canadian LPs, Canada could change its horrible taxation on cannabis cultivation. It is a fixed price per unit, and there is talk of moving to a flexible price. The other thing would be directly beneficial for OGI: a buyout from British American Tobacco. I don’t know why it didn’t already to so, instead opting to acquire more of it at a large premium. I do believe that BTI is very happy with OGI, that there is no legal restriction on them buying the company, and that BTI stock has rallied a lot from its recent lows. Here is the chart of OGI and BTI since the end of 2020, just ahead of the first investment:

YCharts

I am not predicting that BTI will buy OGI, but it sure seems to make sense. The third positive that I didn’t discuss above is that Organigram is set to participate now in the growth of cannabis outside of Canada. And, they are setting themselves up to be involved in the U.S. in the future if the laws change.

So, a reasonably cheap stock with a nice chart, potential rule favorable changes, a global cannabis expansion possibly and perhaps being acquired excite me. I am sticking with Organigram!

Read the full article here