We expressed our bearishness on the PIMCO Dynamic Income Fund (NYSE:PDI) three months ago due to its 12.41% premium at the time, which seemed quite rich. Moreover, Howard Marks of Oaktree had warned that the loans in which PDI primarily invests are probably at the lowest quality they have seen in many years. Meanwhile, Ares Capital’s (ARCC) CEO had just warned that defaults in the industry were likely going to increase this year with liquidity getting tighter and tighter. The fund’s high leverage and its 1.92% management fee combined to make it a potential disaster waiting to happen. Since then, the fund has held up fairly well, delivering a total return of 2.52%. While this has trailed the S&P 500’s 4.18% return over that period and lagged our own portfolio’s performance considerably, it is still a better return than our sell rating would have implied.

However, our call was based on a much longer-term outlook, and by and large, the economy has hung tough over those three months. We think that over the next several years, the risk-reward outlook for the economy’s health is much weaker, as we will outline in this article. As a result, given that its premium to NAV has only increased over that period to now 13.28%, and its portfolio composition remains extremely risky with a heavy weighting on sub-investment grade and even non-rated loans that are heavily leveraged at 38.56%, we think that it is a very unattractive investment on a risk-adjusted basis.

Why PDI Is Facing Severe Macroeconomic Headwinds

The macroeconomic signals that imply trouble ahead for a portfolio filled with low-quality, junk, and non-rated loans include the following:

1. The yield curve model indicates a very high risk of recession.

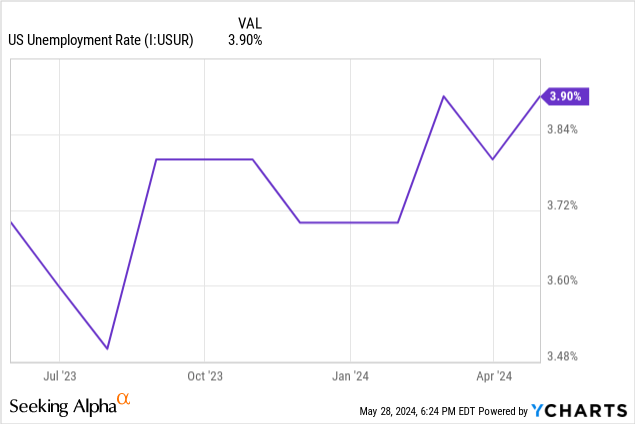

2. The US unemployment rate has ticked up significantly over the past year, particularly since last August, rising from about 3.5% to 3.9%.

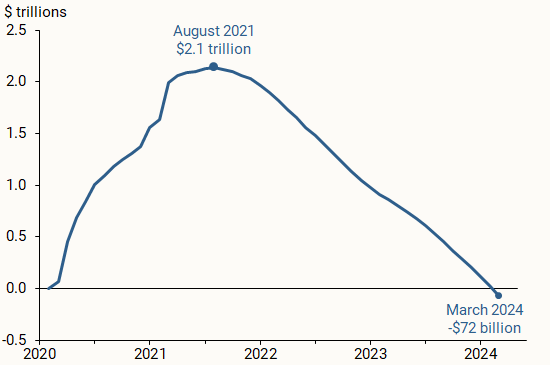

3. Inflation has remained stubbornly high, preventing the Fed from having the flexibility to cut interest rates. The longer interest rates remain high, the more middle-market companies and other smaller, lower-quality businesses to which PDI tends to lend will have a hard time meeting their interest obligations, especially with their profit margins being pinched by persistent inflation. This means that PDI could very well begin to see a spike in defaults in the near future. Additionally, these companies will likely have a hard time growing as they have in the past, since the $2.1 trillion pandemic-era excess savings in August 2021 have now turned negative to $72 billion.

Cumulative pandemic-era excess savings (San Francisco Fed)

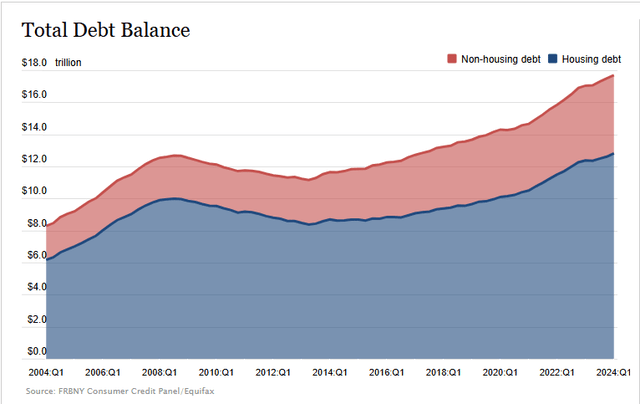

4. Moreover, both non-housing and housing debt continue to push to new highs, with non-housing debt rapidly approaching $18 trillion and housing debt at nearly $13 trillion.

FRBNY

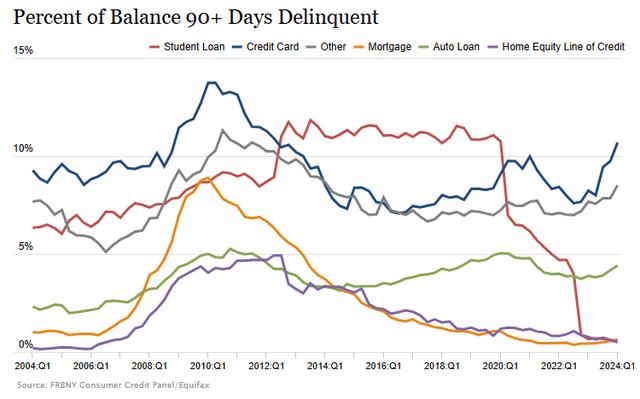

5. Additionally, the percent of balances 90 days plus delinquent have spiked higher across several categories, including credit card debt, which is now well over 10% delinquencies, auto loan debt, which is rapidly approaching 5%, and other categories which are pushing north of 8%.

FRBNY

As the San Francisco Fed puts it, consumer spending, which has until recently been a strong driving force for the US economy, could face major headwinds from the high levels of consumer debt combined with the lack of excess savings and higher for longer interest rates. This is especially concerning when combined with the rising unemployment rate. As a result, while household debt increased by a whopping $184 billion in Q1 and delinquency transition rates have increased across all debt types recently according to the Federal Reserve Bank of New York, this could just be a sign of things to come, potentially leading to a perfect storm for the economy.

Given that PDI already trades at a large premium to NAV and during times of more bearish sentiment, including even in the last 52 weeks, it can trade at meaningful discounts to NAV, which it most certainly would in the event of an economic downturn where defaults spike and its NAV plunges, we see PDI at a high risk of significantly underwhelming investors from a total return standpoint. When you factor in its very high leverage, the risks are even greater. Meanwhile, the upside potential is fairly weak as we see few catalysts that would prompt its valuation multiple to expand from here, and its expense ratio will also weigh on returns.

Investor Takeaway

As a result of these macro headwinds and the valuation headwinds and high leverage and fees at the fund level, we rate PDI a Sell and prefer to steer clear of the low-quality lending space at the moment. If we were to invest in it, we would prefer investing in BDCs that have quality underwriting teams, offer even better dividend yields, and trade at steep discounts to NAV, such as FS KKR (FSK).

Read the full article here