Co-authored by Treading Softly

Have you ever “hedged your bets?”

It’s a common turn of phrase that means to take actions that account for multiple possible outcomes. Often “hedging” involves betting the opposite of what you think will happen. For example, you might pay for extra insurance or for an extra warranty for an event you consider improbable.

Going “all in” can result in tremendous success but also abject failure. Hedging is often a more common choice as it softens the blows we feel in daily life. Hedging has a negative financial impact if everything goes according to plan. It will have a positive financial impact when it doesn’t, offsetting some or all of your financial losses.

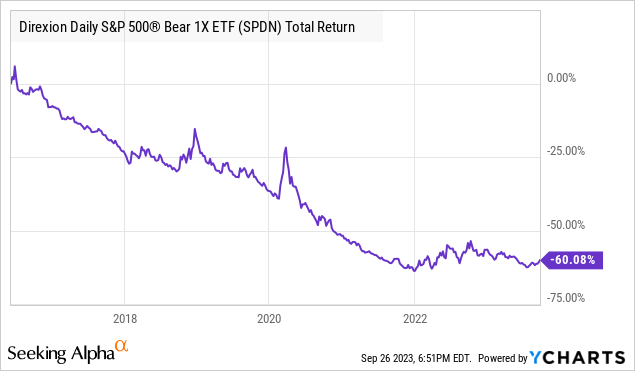

When it comes to the market, I get asked many questions based heavily on assumptions, such as “When there is a recession, every stock goes down in price – that is common knowledge, right?” I am frequently asked whether investors should short the market or buy ETFs that short the market. While it is tempting to hedge your portfolio, the problem is that if you are shorting the market, you better be right about your timing. Long-term, shorting the market is a decidedly losing proposition:

That is exactly why we invest so much in the market. It tends to go up more often than not. An inverse ETF can be a good option if you think you know the market will crash in a few months, but if you are longer than that, you can quickly lose more money shorting than you would have lost on the dip; worse, you aren’t getting it back. At least when the stock market crashes, patient investors will see their value come back in the future, as long as they don’t panic and sell.

One Strong “Hedging” Idea

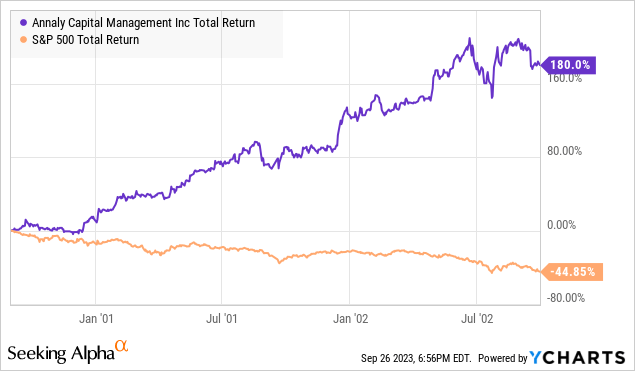

There is a way to “hedge” your portfolio against a recession and get better results while you wait. It is very rare to find an investment that is truly countercyclical, but Annaly Capital Management, Inc. (NYSE:NLY), yielding 13.8%, is one of them. Dot-coms are busting? The S&P 500 started falling in September of 2000 and reached bottom in September 2002:

The S&P 500 fell over 40% before reaching bottom and starting its recovery. Meanwhile, NLY produced a total return of 180% during the same period.

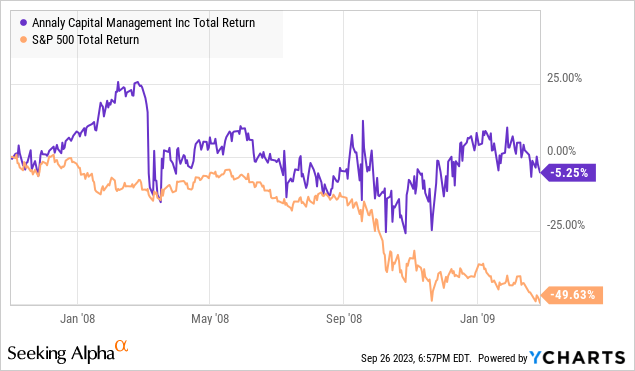

The GFC (Great Financial Crisis) was the worst recession since the Great Depression. Things need to be quite bad to earn the term “Great”. The market peaked and started falling in November 2007 and bottomed in February 2009, losing nearly 50%. NLY had a modest loss of 5% during the same period.

Interestingly, NLY saw its dividend nearly double from $1.04 to $2/quarter during this period, but investors feared that the “agency guarantee” would not be honored. Investors who feared were proven wrong and missed out on a lot of dividends.

NLY doesn’t always outperform the market. Since IPO, its outperformance has been modest. According to YCharts, an investment of $10,000 in NLY at IPO would be worth $82.19k today, compared to $74.04k for the S&P.

Investors are always more influenced by the recent past – like a 10-year-old kid who thinks the world started when they were born and has “always” been that way, many investors assume that what they remember experiencing is everything they need to know.

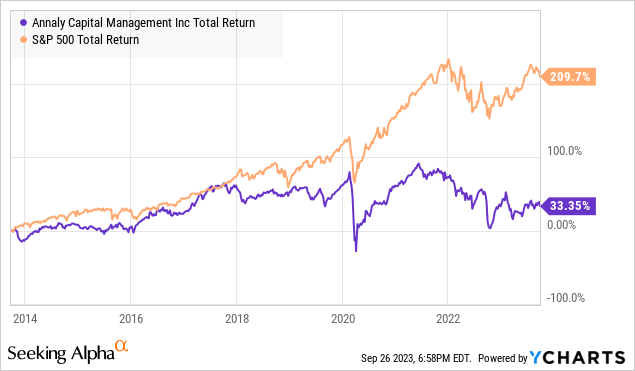

Among these investors, I often get comments about how NLY is a “loser” or that it is a “trading stock”. The past decade has, in fact, been a mediocre one for NLY, and it has trailed the S&P, which has had a very good ten years.

How good has the past decade been for the S&P 500? Well, since 1993, the S&P’s average 10-year rolling return has been a CAGR of 8%. Over the past decade, it has experienced a CAGR of 13.4%, a solid 167% above average.

Now if you are a student of the markets, that alone might set off an alarm bell. Is the market likely to maintain such an above-average pace? Not forever. The S&P 500 is trading at a price/earnings valuation that is well above its historical average. In 2021, the high valuation was blamed on low interest rates. The theory was that investors were buying equities because interest rates had been so low for so long that they had no other options. I’ve seen versions of this theory even before COVID in 2018/2019 when valuations were surging to levels not seen since before the dot-com bust, and some were starting to call it a bubble. Well, today, interest rates are much higher, but valuations are still higher than they were in 2019, and even after 2022 took some of the air out of a lot of companies.

I don’t know when it will fall; it could be next quarter, it could be next year, and I know that bubbles can sometimes last a lot longer than is rational, or it could be longer. But I do know valuations are going to come down, there will be a recession, and the stock market will crash, the same way that I know a hurricane is going to hit Florida at some point in the future. It will happen; it is a question of when.

NLY is a great income stock. It pays a relatively high dividend all of the time. It also has a history of sometimes outperforming the market by a lot. As part of my portfolio, the key benefit that NLY provides is when it outperforms. NLY isn’t likely to be my best holding when the economy is great, the S&P is surging, the sun is shining, and investors feel great. NLY outperforms when unemployment is rising, equities are crashing, bankruptcies are making the news, and everyone knows the economy is terrible. When most stocks in my portfolio might be falling in price, and the risk of dividend cuts is high in many sectors, NLY has historically started hiking its dividend, and its price has held up or even climbed.

The reason is simple. NLY is a leveraged investment in agency MBS (Mortgage-Backed Securities). NLY buys MBS and collects the coupon. Since the principal is guaranteed by the agencies, there is no credit risk, which allows NLY to use a fairly high level of leverage. Since agency MBS is very liquid and has no credit risk, it is most popular among institutions and other investors during recessions. A recession starts, and institutions lend less and plow money into zero-risk assets. Some investors and hedge funds will do the same. NLY is positioned to be a major winner as demand for MBS rises, while at the same time, the Fed responds to a recession by cutting interest rates to 0%, reducing the cost of leverage that NLY has to pay. The result is that NLY enjoys higher book value and higher cash flow.

Conclusion

This is why I believe NLY is an essential part of a balanced portfolio. I don’t know when the next recession will start, but I do know that I want to have a healthy position in NLY and other agency mortgage REITs when it does. While I wait for the next recession, a 13% yield is nothing to sneeze at!

When it comes to retirement, you don’t want a portfolio based on going “all in” on trying to time the market. I see a lot of commenters or writers claiming great success in their timed trades – good for them! I also have been writing and investing long enough to see them come and go. I don’t want a fairweather portfolio or method. So, I designed my Income Method to be as simple, sustainable, and income-generating as possible. So when a recession does come, I’ll have holdings like NLY, which will shine. When the economy is blossoming and thriving, I’ll have other holdings taking the spotlight. I find the best time to add to my portfolio is when others declare, “this is a terrible time to buy!” – it helps me get great additions at rock-bottom prices. This way, I can be out enjoying my hobbies when they all decide to flock back in.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Read the full article here