Co-authored with Hidden Opportunities.

Real estate has always been an integral part of human evolution. In the earliest days of civilization, humans built homes for shelter and cultivated land to feed themselves. As societies evolved, so did the concept of home and land ownership. A basic necessity transformed into an asset that eventually became a utility for wealth creation and preservation.

Today, real estate is a highly favored investment by people of all age groups. However, physical real estate ownership comes with the challenges of high initial investment, income concentration, leasing, tenant management, property maintenance, and tax complications. This is why Real Estate Investment Trusts provide a more passive approach to real estate, allowing individuals to invest in these tangible assets without the hassles of direct ownership. REIT investors have the benefit of regular income through dividends and capital appreciation, while enjoying liquidity and a professional team of experts to run the day-to-day show.

Over 42 countries recognize and have adopted REIT legislation, and there are over 940 listed REITs globally with a total market cap exceeding $2 trillion. As the global population grows and urbanization accelerates, nations need to attract new sources of capital to construct and maintain real estate assets, and REITs are an important vehicle for providing access to local and global capital.

In the current environment, REITs are facing less stress and enjoying greater operational flexibility than ever before. Source.

Nareit

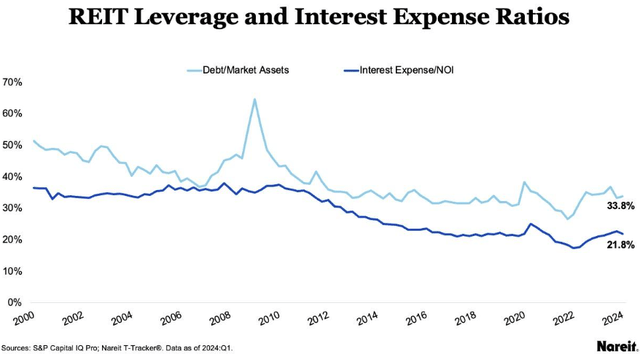

Since the peak during the GFC (Global Financial Crisis), the average leverage ratio of REITs dropped considerably (nearly 50%) to 33.8% in Q1 2024. This level matches that of lower-risk private real estate investments. In the same vein, the average interest expense ratio shows a similar downward trend, reaching 21.8% as of Q1 2024, indicating greater flexibility amidst the Fed’s quantitative tightening.

With banks maintaining tighter lending standards and reducing their risk profiles, new developments are limited, creating a tight supply situation. Except for the office sector, leasing activity across the REIT sectors remains strong and despite concerns of a possible recession, landlords worldwide passed through rent increases to their tenants.

The tight supply situation has the potential to benefit the industry when the economy rebounds with rate cuts. This is, after all, a dividend-friendly sector, so as we await those tailwinds, we sit back and collect healthy income.

Let us now review two REIT-oriented investments to collect large paychecks from the expertise of seasoned professionals.

Pick #1: NNN – Yield 5.4%

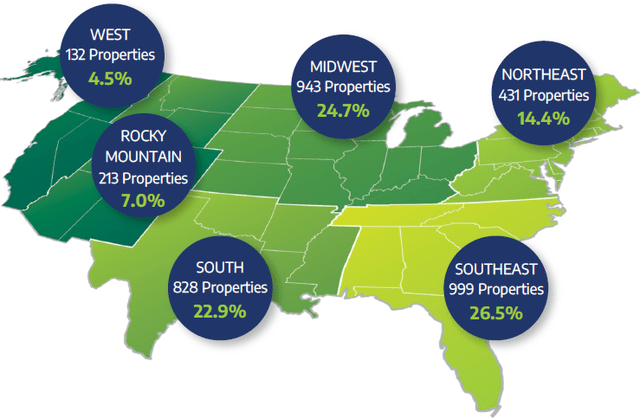

As the name goes, NNN REIT, Inc. (NNN) is a triple-net-lease Real Estate Investment Trust whose tenants are responsible for operating expenses, taxes, and capital expenditures associated with properties. NNN operates 3,546 properties leased out to 400 tenants across 37 lines of trade. The REIT has geographically diverse operations with real estate assets in 49 U.S. states. Source.

May 2024 Investor Presentation

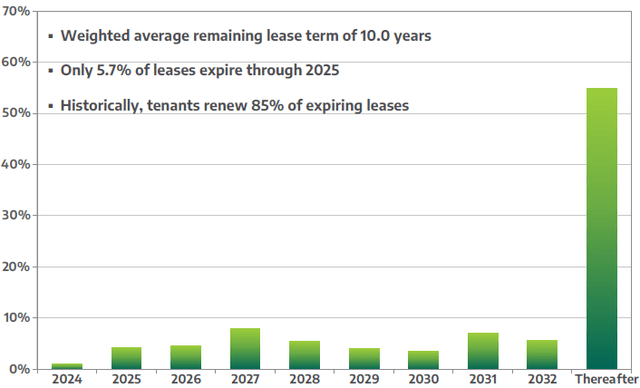

NNN has been a public company since 1984. As of Q1 2024, the company establishes long-term lease agreements with a 10-year weighted average remaining term. Only 5.7% of the leases are set to expire through 2025, and according to the REIT’s operating history, about 85% of the tenants renew their leases.

May 2024 Investor Presentation

NNN maintains higher exposure to single-tenant retail tenants who typically renew their lease at the end of the term. As a result of its steady leasing and diligent screening process, the REIT has typically experienced lower earnings volatility from overall higher occupancy. NNN’s occupancy has never dropped below 96.4% in the past two decades and ended Q1 2024 at 99.4%.

NNN maintains a strong investment-grade BBB+ balance sheet with mostly fixed-rate debt, 100% unencumbered assets, and 11.8-year weighted average debt maturity, positioning it well in this elevated interest rate environment. During Q1 2024, NNN reported adjusted funds from operations (“AFFO”) of $0.84/share (up 3.8% YoY), placing its common stock dividend payout ratio at 67%, an impressive number by REIT standards. This left ~$50.6 million of FCF for the quarter (after all expenses and dividends), placing it on track to achieve $194 million for FY 2024. NNN has delivered 34 consecutive annual dividend increases, and its current $0.565/share quarterly payment calculates to a 5.4% annualized yield. We are confident of seeing the REIT deliver another raise at the announcement of its next dividend to keep up with its industry-leading dividend stewardship.

Pick #2: AWP – Yield 12.7%

abrdn Global Premier Properties (AWP) is a CEF providing investors diversified access to the best global REITs to fuel our income. AWP’s global exposure makes it different from other REIT-focused funds we hold. Approximately 40% of the fund’s assets are deployed into non-U.S. REITs.

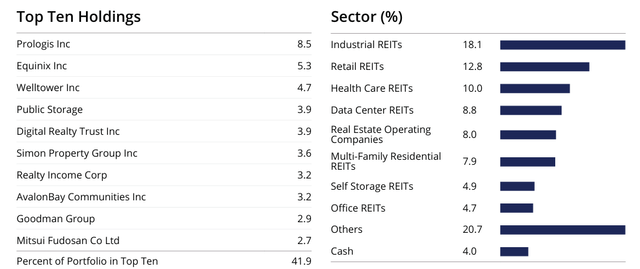

AWP’s top holdings are some of the prominent and fundamentally sound REITs globally. NAREIT estimates that industrial, retail, and residential REITs will achieve significant YoY FFO growth in 2024. This positions AWP right in the opportunity, as the CEF has its highest allocations in these REIT subtypes. Source.

AWP Fact Sheet

AWP operates with a modest 17% leverage to boost returns from its active management strategy. We note that AWP came under Abrdn in May 2018 following the firm’s acquisition of assets from Alpine Woods Capital Investor. Following the transition and initial distribution adjustments, AWP has maintained its payment levels through the global pandemic. Source.

Portfolio Visualizer

Today, AWP’s yield is well above the average levels for the CEF since the transition, presenting an attractive opportunity for investors to lock in the monthly income amidst depressed REIT valuations from elevated interest rates.

During FY 2023, 94.2% of the distributions were Return of Capital, and the remaining comprised ordinary dividends. This provides much-needed deferred tax treatment on the distributions for eligible shareholders.

We note that many of the non-US REIT holdings are structured as partnerships. With such PFICs (passive foreign investment companies), AWP pays the tax at the fund level, so to the investor, it is ROC because the taxes were already paid. Thanks to favorable laws, many U.S. REITs will have 20-30% ROC annually. For U.S. investors, AWPs’ post-tax yield is higher since a substantial portion of your distributions are tax-deferred and ultimately taxed as long-term capital gains.

AWP currently pays $0.04/share per month, a 12.7% annualized yield, and the CEF trades at a 2% discount to NAV, providing a bargain to tap into global real estate.

Conclusion

To benefit from the income and capital appreciation potential of real estate, it is no longer necessary to invest thousands of dollars to buy a single property or have lawyers on your payroll to help you with your leasing and evictions. The beauty of fractional shares allows you to seize the power of real estate with just $1.

In the current market conditions, REITs are being ignored despite operating with solid fundamentals. REIT sector dividends continue to rise as the companies grow their FFO and NOI, while managing their balance sheets conservatively. NNN presents an attractive investment for those seeking exposure to single-tenant retail properties managed by an experienced team with a proven track record. AWP, on the other hand, makes a good investment for those seeking high current income from a highly diversified global real estate exposure.

Our Investing Group specializes in identifying passive income opportunities in the financial markets. Our “model portfolio” holds REITs, MLPs, royalties, and much more, targeting a +9% overall yield. We focus on investments that let us benefit from the expertise of seasoned professionals, ensuring steady and regular cash returns without the hassle of hands-on management. This is the essence of income investing for a stress-free financial future.

Read the full article here