Co-authored with Hidden Opportunities

Summer is my favorite season of the year. It is the time I get to pursue one of my most anticipated hobbies — gardening. I work to transform my lawn into a vibrant, vegetable-producing system. I enjoy the process of sowing seeds, fertilizing, watering, and caring for my plants as I witness the incredible progress of growth and development. As the summer progresses, my garden will begin providing a bounty of fresh produce for my family to relish.

In the financial world, the stock market provides an ecosystem like my backyard. My savings are the seeds, and research and analysis are the nourishments needed to grow and safeguard my income. With the objective to generate income while I sleep, these are my top considerations.

-

Dividend Safety and Consistency: The investments I hold must make regular and repeatable payments. These dividends must be a non-discretionary component of the company’s operations and, barring catastrophic conditions, should keep flowing into my account. Preferred securities fit this requirement, as they are higher up in the issuer’s capital structure, and companies are heavily incentivized to stay current on payments to maintain their credit standing and their reputation among consumers and institutions.

-

Dividend Coverage: The dividend should be substantially covered by the company’s operations. In fact, the dividend expense towards my held securities should represent a very small fraction of their bottom line. With preferred, you often have the common stock dividend, which is several times larger than the preferred dividend, thereby acting as a cushion for your income stream.

- Financially Strong Companies: I choose companies that maintain comfortable liquidity and debt maturities and consistently generate profits in excess of the shareholder commitments. Looking at past catastrophic events, we saw the GFC adversely impact the U.S. banking industry, while the COVID-19 pandemic brought the global travel industry to its knees. Yet, we saw one company from each of these sectors maintain their preferred dividends through major headwinds. Let us now review these high-quality preferreds:

Pick #1: USB Preferreds — Yields Of Up To 7.2%

U.S. Bancorp (USB) is the fifth-largest bank in the U.S., with $684 billion in assets under management and $523 billion in deposits. USB maintains a strong footprint in the U.S. with 2,256 branches and over 11 million clients in the consumer and business banking segments.

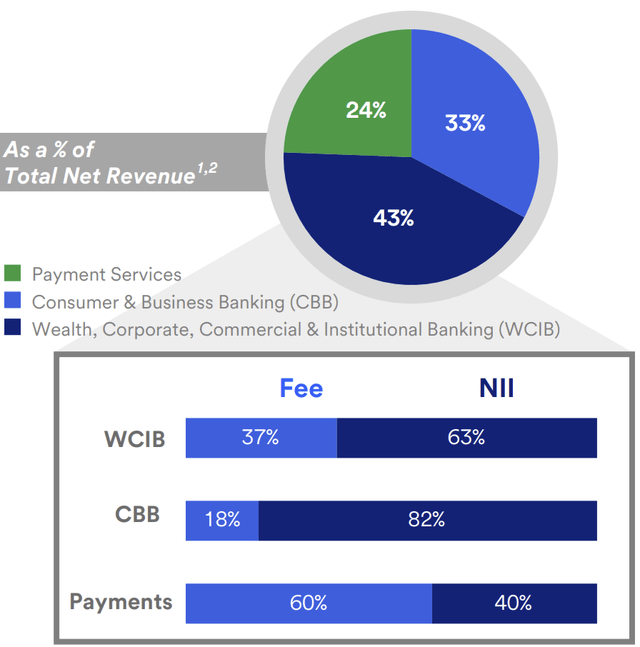

While USB’s Q1 report was disappointing, the bank delivered a better-than-expected Q2 with $4.05 billion in NII (Net Interest Income), beating analyst estimates. USB reported healthy deposit growth, and continued momentum in its diversified fee income platform. Notably, 41% of the bank’s total net revenue comes from highly diversified and sustainable fee revenue streams, which improves the predictability of cash flows and minimizes the effects of interest rates on its profitability. The bank has reaffirmed NII between $16.1 and $16.4 billion for FY 2024. Source

July 2024 Investor Presentation

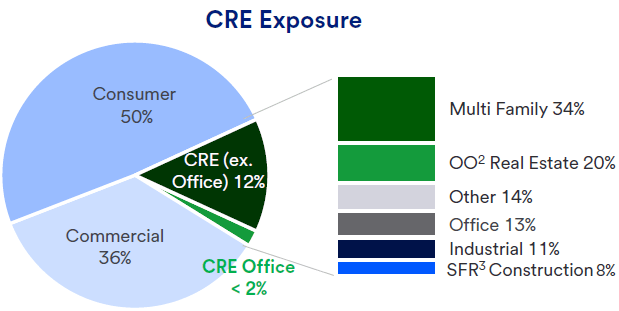

USB’s CRE (Commercial Real Estate) exposure is rather limited. It represents 14% of its loan portfolio, and office properties constitute less than 2% of all loans.

May 2024 Investor Presentation

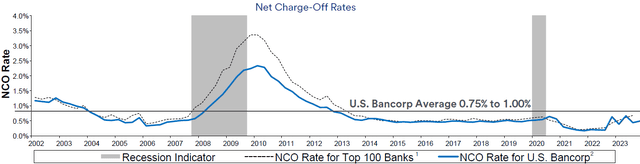

USB has a strong track record of consistently maintaining charge-offs below industry peers through a tough economic climate.

May 2024 Investor Presentation

But we are less interested in USB for its common stock. The preferred securities present significantly better risk-reward in the current economy.

-

Fixed-to-Float Series A, Non-Cumulative Perpetual Preferred Stock (USB.PR.A) — Yield 7.5%

-

Float Rate Series B, Non-Cumulative Perpetual Preferred Stock (USB.PR.H) — Yield 7.2%

-

5.50% Series K, Fixed Rate Non-Cumulative Perpetual Preferred Stock (USB.PR.P) — Yield 5.8%

-

3.75% Series L, Fixed Rate Non-Cumulative Perpetual Preferred Stock (USB.PR.Q) — Yield 5.6%

-

4.00% Series M, Fixed Rate Non-Cumulative Perpetual Preferred Stock (USB.PR.R) — Yield 5.6%

-

4.50% Series O, Fixed Rate Non-Cumulative Perpetual Preferred Stock (USB.PR.S) — Yield 5.5%

We don’t have USB’s 10-Q for Q2 yet, so we will review the breakdown of shareholder commitments from the Q1 filing. During Q1, USB spent $76 million on preferred stock dividends (up from $67 million in Q1 2023 due to the presence of floating-rate preferreds). This is just 10% of the amount ($770 million) the bank spent on common dividends. USB reported a quarterly net income of $1.3 billion for Q1 (and $1.6 billion for Q2), adequately covering its common and preferred equity commitments. The preferreds, in particular, enjoy 17x coverage from net income. We note that USB maintained its preferred dividends through the Great Financial Crisis despite making cuts to its common stock dividend.

USB has several quality preferreds at deeply discounted prices. For example, USB-Q, USB-R, and USB-S present excellent opportunities for large total returns, with +5.6% current yields and ~50% upside to par. We expect these to realize significant capital gains with even modest interest rate cuts.

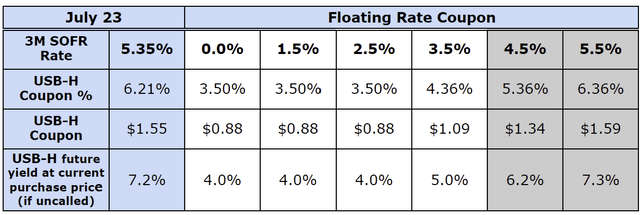

The focus remains on USB’s floating-rate preferreds, notably USB-H, which offers a 7.2% current yield and ~15% upside to par. The coupon for this security is recalculated every quarter based on 3-month SOFR rates (the recent determination date was July 11). With rates projected to stay elevated and diminishing possibilities of steep rate cuts, USB-H offers an attractive proposition for CD-beating income, considering its high base coupon and tax-advantaged qualified dividends.

Author’s Calculations

Pick #2: RLJ-A — Yield 7.8%

The outlook for travel is strong in 2024. Americans have begun hitting the road this summer. Amidst elevated inflation and economic slowdown, travelers come from different demographics, purposes of travel, and varying budgets. Even the outlook for business travel is strong, with projections to grow to nearly $1.8 trillion globally by 2027, according to a report by the Global Business Travel Association.

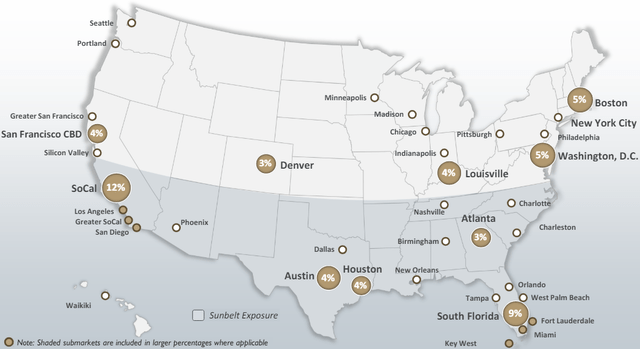

RLJ Lodging Trust (RLJ) is a hotel REIT with a portfolio of 96 properties with a high footprint in the sunbelt states. 66% of its EBITDA comes from urban areas, positioning the company well to cater to business and leisure travel. Source

RLJ June 2024 Investor Presentation

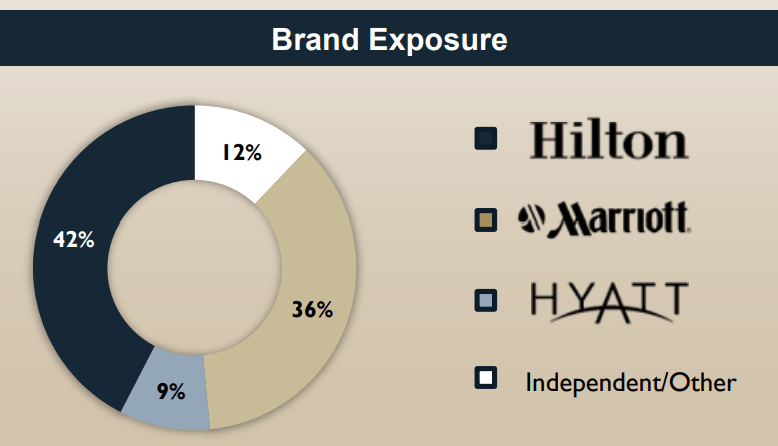

The REIT maintains excellent exposure to popular hotel brands like Hilton (HLT), Marriott (MAR), and Hyatt (H) and has a modest portfolio of independent collection properties.

RLJ June 2024 Investor Presentation

RLJ continues to ride the post-pandemic recovery in domestic travel by delivering strong operating metrics. During FY 2023, RLJ delivered a 4.5% YoY growth in Average Daily Rate to $197, a 9% YoY growth in Revenue Per Available Room to $141, and an 8.5% YoY growth in the Adj. EBITDA/key. During Q1, the company completed the purchase of the 304-room Wyndham Boston Beacon Hill for $125 million cash. This property sits in an A+ location within Boston’s Beacon Hill neighborhood and is surrounded by Massachusetts General Hospital, which is currently undergoing a $1.8 billion expansion.

RLJ is not just recovering from the pandemic and its impact on the travel industry; it is doing so rapidly while delivering returns to shareholders. The REIT repurchased $77.2 million worth of common shares in FY 2023 and doubled the common dividend.

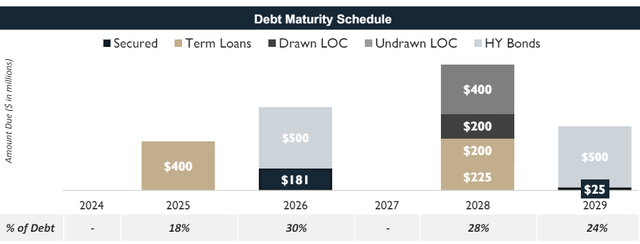

The company’s $0.40/share annual dividend enjoys adequate coverage from its operations, as seen from the FY 2023 AFFO/share of $1.66. Since 2018, RLJ’s total common stock repurchases have reached $300 million, representing ~13% of the float. During the first quarter, RLJ also addressed all its 2024 debt maturities and reported adj. EBITDA of $79.6 million, and adjusted FFO of $51.8 million. The REIT ended Q1 with a low-leveraged balance sheet with over $1 billion in liquidity, including $350 million of cash. 82% of RLJ’s debt is fixed or hedged, and the portfolio carries a weighted average interest rate of 4.29%. Overall, the company is well-positioned to handle its 2025 maturities and beyond.

RLJ June 2024 Investor Presentation

RLJ has non-callable preferred security, making it an excellent source of perpetual cash flows from a well-managed hotel REIT. (RLJ.PR.A) cannot be redeemed by the REIT but can force conversion to common stock only if RLJ trades at or above $89.09 for 20 out of 30 trading days. As such, for the preferred to become convertible, the common stock has to surge 825%. We consider this highly unlikely, making RLJ-A a busted convertible that will pay dividends for the foreseeable future. We note that this preferred does not have a par value, so investors should not assume $25 to be some sort of price ceiling for RLJ-A. This security has traded as high as $29 during the post-COVID yieldless market.

RLJ-A currently yields 7.8%, presenting an attractive yield to lock into for the long term. This preferred dividend costs RLJ $6.2 million every quarter, or $25 million annually. The company spends $12.9 million on quarterly common stock distributions (factoring in the raise in FY 2023). The REIT generated over $20 million in cash from operating activities during Q1 and maintains ample liquidity to manage the preferred and common stock commitments.

Of adults in the United States (over 212 million people), 82% are planning to travel this summer. In The Vacationer’s yearly summer travel and trends survey, 57% of the respondents mentioned their plan to travel domestically to explore the U.S. With RLJ-A in your portfolio; you get your cut from every traveler’s budget.

Conclusion

This summer, I am growing tomatoes, beans, zucchini, and cantaloupes in my backyard. It took quite some work to clean the tools, clear the weeds, prepare the soil, source the seeds, and transplant the saplings onto the garden bed. I believe the hard part is over, and it gives me a lot of joy to watch them grow on their own as I perform routine maintenance.

Along with those vegetables that I look forward to growing and harvesting, I am also growing my income this summer by leveraging interest rate uncertainties to my advantage. I am scooping up deeply discounted preferreds with high yields. This article discusses two preferred families from high-quality businesses with ample liquidity to support their operations through a strained economy. Our Investing Group is a big proponent of fixed income in these precarious times, as we seek steady income higher up in the corporate capital structure. Our model portfolio has over 50 individual securities and diversified funds focusing on this asset class and targets +9% overall yield. This defensiveness ensures we receive our paychecks while we are hiking, camping, cruising, or sleeping it off. This is the beauty of income investing.

Read the full article here