Co-authored with Hidden Opportunities

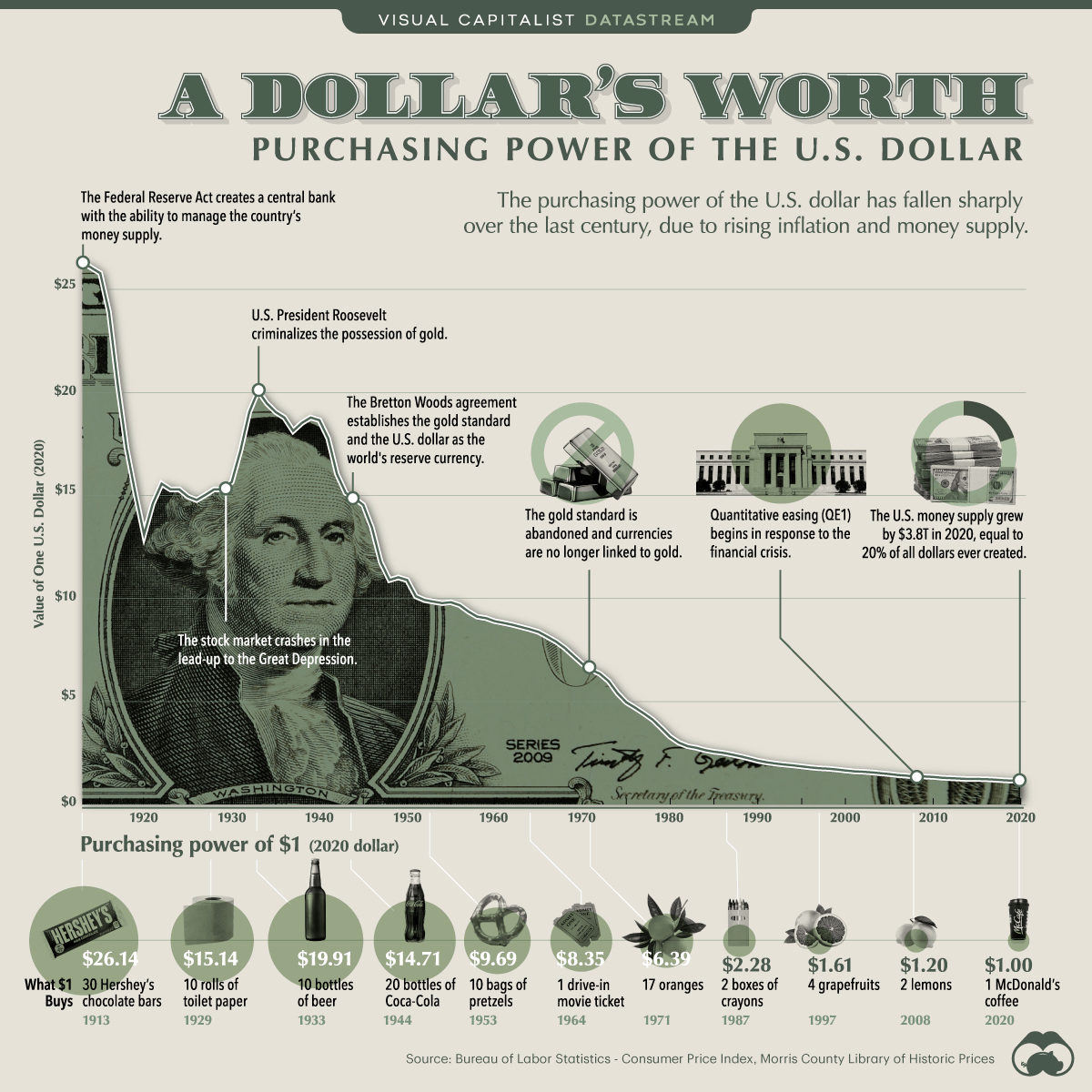

When the economy faces turbulence, it is a good idea to bolster your portfolio defenses. This doesn’t mean selling everything and going into cash. The idea of staying in cash may sound appealing and make you feel secure, but this is one of the worst things you can do with your money. Money by itself is the worst defense against inflation. According to data from the U.S. Bureau of Labor Statistics, the dollar has lost about 98% of its value since 1924. This means that what could be bought for $1 in 1924 would cost around $25-30 today, reflecting a dramatic decrease in purchasing power.

Visual Capitalist

Instead, defensive investing is a strategy for minimizing portfolio risk by choosing stable investment products. This could include securities that have proven themselves over the years, companies that offer non-discretionary products or services, or securities that are placed higher up in a company’s capital stack, such as preferred stock or bonds. Altogether, we are focusing on buying cash flows, to provide the dual benefits of inflation resistance and protection against a recession.

The Federal Reserve is hurting the economy by keeping rates elevated, but as fixed-income investors, we see this as a generational opportunity to buy cash flows.

“When life gives you lemons, make lemonade”

Preferred stock at current prices presents an excellent opportunity for big total returns with high yields and significant capital upside to par value. Moreover, we are able to secure high yields while maintaining high credit quality, which isn’t a common occurrence. Without further ado, let’s dive into our top picks.

Pick #1: Athene Preferreds — Up To 7.4% Yields

Athene Holding Ltd. is a wholly-owned subsidiary of Apollo Global Management (APO) and a market leader in retirement services. The company holds a leading market share in the U.S. annuity markets, including pension plans. Despite being under APO, Athene maintains a separate capital structure to issue senior debt, subordinated debt, and preferred stock.

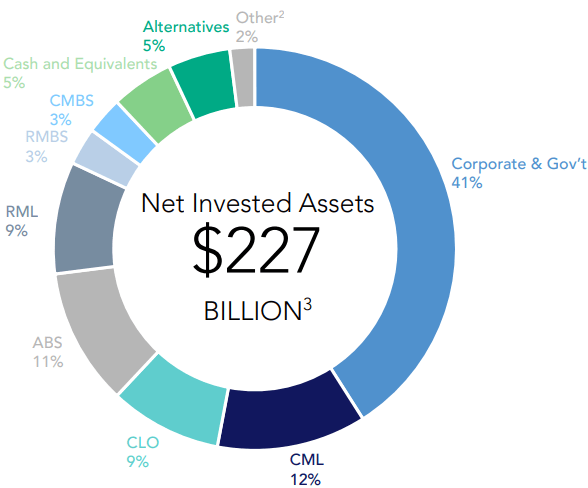

With $293 billion in invested assets, Athene is only behind MetLife and Prudential in the retirement services business. AM Best recently upgraded the company’s balance sheet to A+. The credit agency disclosed its assessment of Athene’s balance sheet as very strong, complemented by its strong operating performance, favorable business profile, and appropriate enterprise risk management.

Amidst high interest rates, Athene has been pursuing high-grade and low-risk investments, with 95% invested in fixed income and 97% of the portfolio deployed into investment-grade securities. Source

May 2024 Investor Presentation

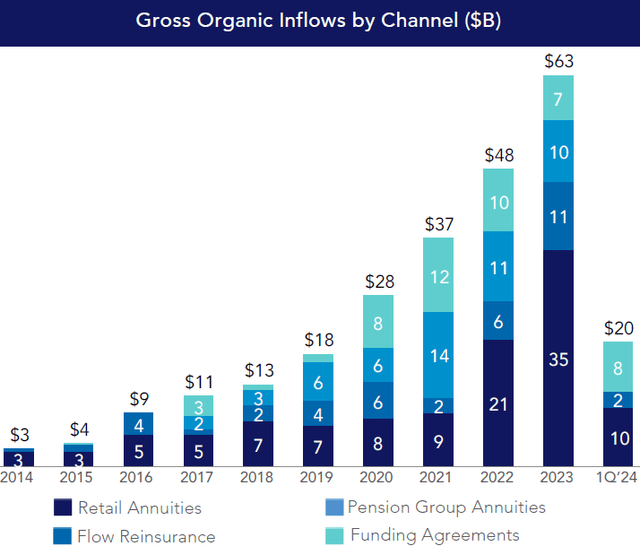

Athene has a track record of consistently positive earnings driven by favorable earning spreads and operating profitability, despite rising competition. Notably, the company achieved $20 billion in gross inflows across all product offerings in Q1 2024, exceeding the total for 2019, and well-positioned to set new records this year.

May 2024 Investor Presentation

Athene ended Q1 with $3.6 billion in excess regulatory capital and $81 billion in available liquidity, including $10 billion in cash assets. After factoring in the $45 million spent on preferred dividends, Athene generated $1.1 billion in net income in Q1 2024, indicating substantial coverage for the income from these securities.

Athene has five preferreds, offering an interesting combination of current income, call date, capital upside, and interest-rate dependencies. Athene preferreds carry investment-grade BBB ratings from S&P.

-

6.35% Fixed-to-Float, Non-Cumulative, Series A Redeemable Perpetual Preferred (ATH.PR.A) — Yield 6.5%

-

5.625% Fixed Rate, Non-Cumulative, Series B Redeemable Perpetual Preferred (ATH.PR.B) — Yield 6.5%

-

6.375% Rate Reset, Non-Cumulative, Series C Redeemable Perpetual Preferred (ATH.PR.C) — Yield 6.3%

-

4.875% Fixed Rate, Non-Cumulative, Series D Redeemable Perpetual Preferred (ATH.PR.D) — Yield 6.4%

-

7.750% Rate Reset, Non-Cumulative, Series E Redeemable Perpetual Preferred (ATH.PR.E) — Yield 7.4%

ATH-C offers a 6.3% yield and has the potential to have a much higher coupon after its September 2025 call date. This security resets to 5-Year T-Bill + 5.97% every five years, and this massive base coupon almost guarantees the post-call coupon to be higher than the present value. It makes ATH-C a likely candidate to be redeemed at the first opportunity available, and offers a generous 6.8% YTC at current prices.

ATH-D’s low coupon makes it a rather unlikely candidate for redemption anytime in the near future, despite its call date of December 2025. As such, this security offers a 6.4% qualified yield and a massive 31% upside to par.

ATH-E is a good option for those seeking big qualified yields for a few years. This security comes with a high base coupon, presenting a 7.4% qualified yield and ~3% downside upon redemption. After December 2027, the security will experience a rate reset, and it is likely that ATH-E will reset to a lower yield than the present.

Athene preferreds make an excellent fit for those seeking high qualified dividends from a robust insurance company for the foreseeable future.

Pick #2: PFFA — Yield 9.4%

For a more diversified approach to preferreds, Virtus InfraCap U.S. Preferred Stock ETF (PFFA) is a rare gem for income investors. Born in mid-2018, PFFA maintains an objective to generate current income by actively managing a portfolio of preferred securities issued by U.S. companies with a market cap of over $100 million. Since its inception, the ETF has delivered $11.0725/share in total distributions to date. Just these payments constitute a 44% return on the ETF’s $25 IPO price, and today’s discounted prices present an attractive bargain to lock in a higher yield.

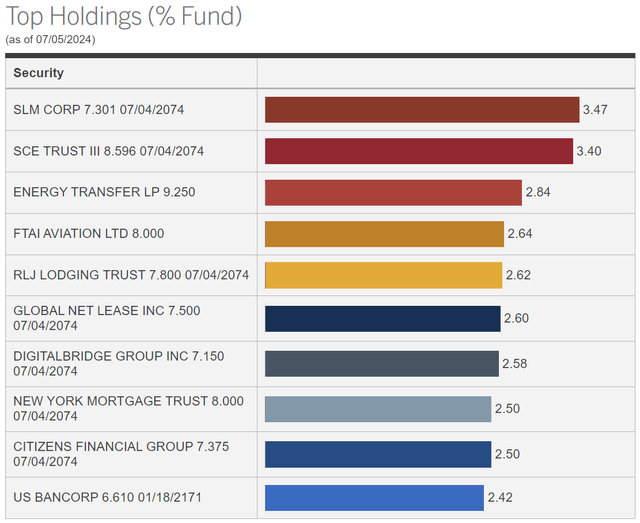

Management provides an updated view of the top holdings nearly every week, and it is not unusual to see changes in the allocation or even the security composition itself in each new release. Source

Virtus Website

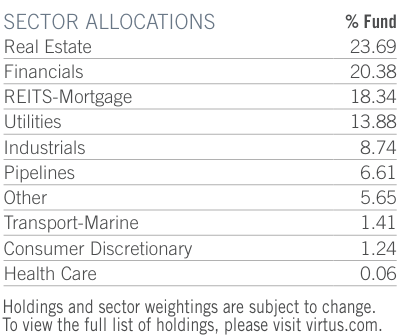

The ETF’s highest allocations are in two asset classes that present the steepest discount in today’s market. REITs and Utilities typically operate with higher levels of debt than other sectors and have been beaten up by the hawkish interest rate policy. However, given the inflationary environment, property prices and utility costs have soared, and these companies have successfully passed on the elevated costs to their customers through rent and rate hikes. mREITs are undervalued because of the volatility in mortgage securities due to the uncertainty over interest rates. But, these counter-cyclical investments provide proven recession defense and are well-positioned for tailwinds through rate cuts. Lastly, following the bank failures last year, the markets have decided to throw the baby out with the bath water, resulting in the preferreds of several well-managed banking institutions sporting high yields and discounted prices. We have also discussed several of them issuing new preferreds at coupons we haven’t seen in decades. PFFA’s allocation to the preferreds from these undervalued sectors represents 76.3% of the total assets. By investing in the preferred securities of undervalued sectors, PFFA is protected from market sentiment at a business level and becomes a play for discounted high yields from asset classes well-positioned for recovery. Source

Fact Card

PFFA is actively managed and utilizes leverage in its investing strategy, making it quite comparable to a CEF (Closed-End Fund) in many ways. In its annual report for FY 2023, the ETF describes having significantly benefitted from its allocations to Hersha Hospitality Trust and DigitalBridge preferreds, which resulted in big double-digit capital gains in addition to the dividends paid all along.

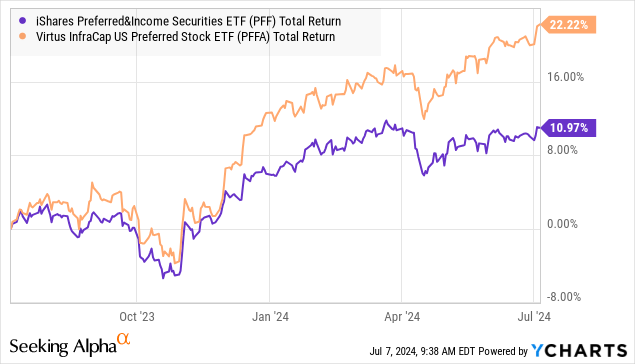

Similarly, the ETF has a higher allocation to SCE’s floating rate preferred (SCE.PR.H), which offers an 8.596% yield, and quality regional bank preferreds, including our recently discussed M&T Bank (MTB). PFFA’s strength lies in active management, moving into the best opportunities to lock high YTC and deliver returns to shareholders. This is seen from PFFA’s outperforming total returns since the Fed stopped hiking rates when measured against the unleveraged benchmark preferred index follower, the iShares Preferred and Income Securities ETF (PFF).

In the past five years, on average, 68% of PFFA’s distributions were supported by NII (Net Investment Income), and ~40% came from realized gains. On average, ~5% of the payments constituted ROC (Return of Capital), and the ETF ended FY 2023 with over $17 million in unrealized gains, representing ~31% of the net distributions paid during the fiscal year. With the fixed-income market set for a robust recovery fueled by at least a few rate cuts in the next six months, we continue to see a terrific income opportunity in PFFA.

Conclusion

Cash is a depreciating asset. The longer you keep it idle, the lesser your buying power. So think twice before hitting that sell button in fear of a recession.

“Well, cash is always a bad investment. When people say ‘cash is king’, that’s crazy. It is sure to go down in value over time. It is like oxygen, essential in sufficient amounts for security but unproductive and depreciative when stockpiled. All you know is that the dollar is going to be worth less 10, 20, 30 years from now” — Warren Buffett.

Our Investing Group is dedicated to acquiring meaningful assets for reliable cash flow generation. We have adopted a strategy we fondly call The Income Method, to collect dividends and interest payments from a highly diversified portfolio. Economies are cyclical, and by holding over 45 securities from across asset classes and sectors, some experience tailwinds and deliver dividend raises while others go through headwinds and pursue dividend cuts. This diversification ensures our portfolio remains steady through market fluctuations, and by focusing on income, we continue to get paid nevertheless. Our model portfolio targets an overall yield of over 9% to generate a lifestyle-supporting income stream.

Amidst this market uncertainty, we are boosting our preferred stock allocations, to generate lower-risk income and meaningful total returns through a recession. What are your plans?

Read the full article here