The REIT market (VNQ) is vast and versatile, and just because two companies share the “REIT” acronym does not mean that they have anything else in common.

To give you an example: you probably would agree that the fundamentals of an American farmland REIT are completely detached from those of a cell tower REIT operating in Africa or a Mexican industrial REIT.

Even then, REITs will often trade as a group as if their fair value were closely correlated with one another.

As you can imagine, this often leads to mispricings in the REIT sector, with some REITs being overpriced relative to others.

In what follows, I will highlight two overrated REITs that I would consider selling because they are overvalued relative to their close peers. I will also highlight better alternatives for you to consider:

Getty Realty (GTY) & NNN REIT (NNN)

GTY is the first overrated REIT that I will discuss.

I actually think that GTY is a relatively good REIT. The management is well-aligned with shareholders, they have historically followed an interesting strategy, and their portfolio/balance sheet should allow them to earn highly consistent cash flow for a long time to come.

Moreover, their 6.5% dividend yield is safe and likely to keep growing, albeit at a slow pace.

However, I just don’t see the point of buying it when you could buy close peers that are far better diversified and likely to grow at a faster pace at very similar valuations.

NNN REIT is a great example that’s underrated when compared to GTY.

GTY is actually a bit more expensive than NNN at the moment.

| GTY | NNN | |

| FFO Multiple | 12.6x | 12.5x |

However, NNN is superior from every perspective:

1) Stronger portfolio

Both are net lease REITs, but the portfolio structure of NNN is far safer.

GTY is highly concentrated on gas stations, which are considered to be riskier net lease properties. They typically trade at higher cap rates than other net lease properties because of two key reasons:

- The growth of EVs could materially reduce their profitability over the long run. Gas stations make money by attracting people to the pumps, and they then sell them high-margin products inside the store to earn money. But it will be far harder to attract EV drivers because they will charge their car at home most of the time, and even when traveling longer distances, they would rather charge at a restaurant where they will spend a lot of time rather than at a road side convenience store. The impact of EVs won’t be immediate, but already in 10-20 years from now, it could start to impact gas station, reduce their profitability, and put them in a state of oversupply.

- And the second problem is that redeveloping gas stations into other uses can be very difficult and expensive due to the environmental issues. Removing fuel tanks is very expensive and often requires soil remediation and/or removal and backfill, which is also very costly. Moreover, it is also a significant liability risk for the property owner. You may tear down the gas stations and build something new on top of them, but if there is a complaint in the future, you may need to destroy whatever you had built on top just to clean the soil.

Getty Realty

NNN, on the other hand, is much better diversified across different service-oriented categories of the net lease market.

NNN REIT

Therefore, even if you were neutral about the high exposure to gas stations, it still wouldn’t make sense to favor GTY over NNN. At the very least, you should get a lower valuation in order to be compensated for the higher risk and lack of diversification, but this is not the case here.

2) Better balance sheet

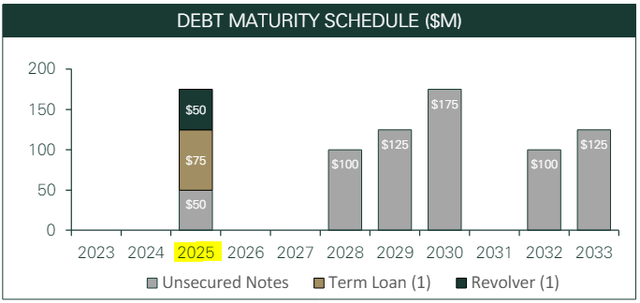

GTY has a 40% LTV, a 6-year average debt maturity, and it has big debt maturities occurring in a year from now.

Getty Realty

NNN has less leverage with a 30% LTV, and importantly, it has far longer debt maturities at 13 years on average. Therefore, it will be a lot less impacted by the surge in interest rates.

This stronger balance sheet is also reflected in its superior credit rating. NNN has a BBB+ rating, whereas GTY is only one notch above junk at BBB-. If any risk factor played out, GTY could quickly lose its investment grade rating.

3) Faster growth prospects

Finally, I would expect NNN to grow faster than GTY over the long run.

It has a stronger portfolio, a better balance sheet, and can access capital at a lower cost to keep growing. Moreover, it also retains a much larger percentage of its cash flow. Its payout ratio is just 68% vs. 83% for GTY.

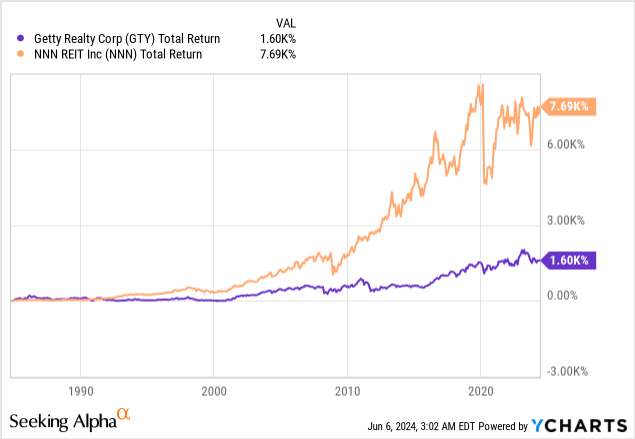

This faster growth has historically resulted in far higher total returns for NNN, and I don’t see why this outperformance would end anytime soon.

If anything, this outperformance could accelerate as GTY will be more heavily impacted by the surge in interest rates and will likely eventually start to feel the pain of EVs.

Therefore, I think that NNN offers much better risk-to-reward at this time.

GTY is overrated. NNN is underrated.

Boston Properties (BXP) & Alexandria Real Estate (ARE)

Once again, we have two REITs that trade at similar valuations, but one of them is clearly superior to the other. BXP may seem a bit cheaper relative to its FFO, but if you adjust for its higher leverage and the higher cap rate of its properties, then the multiples are actually very similar:

| BXP | ARE | |

| FFO Multiple | 9x | 11x |

In this case, Boston Properties is overrated and Alexandria is underrated in my opinion.

1) Stronger portfolio

Boston Properties owns mostly traditional office buildings. Its occupancy rates have been declining, and its new lease incentives have been increasing as the world moves to a hybrid work setting.

Alexandria, on the other hand, owns mostly life science properties. They are not heavily impacted by remote work because you cannot conduct lab experiments from home, let alone store and safeguard highly valuable lab equipment and intellectual property.

Alexandria Real Estate

Moreover, Alexandria’s leases are relatively long at 8 years on average and enjoy 3% annual escalations, protecting it from any near term impact from oversupply. Finally, its current rents are deeply below market, which provides a “bank of growth” as well as margin of safety. Historically, it has managed to hike rents by 20-30% as leases rolled over.

2) Better balance sheet

Boston has a 40% LTV, a 6-year average debt maturity, and it has big debt maturities occurring in a year from now.

Alexandria has less leverage with a 30% LTV, and importantly, it has far longer debt maturities at 13 years on average. Therefore, it will be a lot less impacted by the surge in interest rates.

This stronger balance sheet is also reflected in its superior credit rating. Alexandria has a BBB+ rating, whereas Boston is only one notch above junk at BBB-.

3) Faster growth prospects

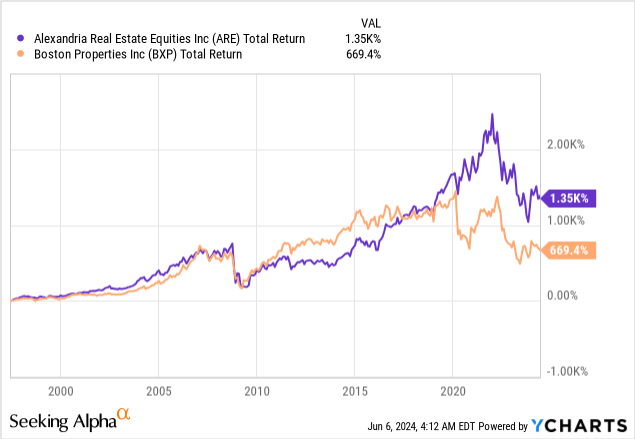

Again, Alexandria’s faster growth is well-reflected in its historic outperformance, and given that it owns better assets and has a stronger balance sheet, I don’t see why this outperformance would end any time soon:

If Boston was priced at an appropriate discount relative to Alexandria, then it would be different of course, but since it is not the case here, I am quite confident that Alexandria will continue to beat Boston going forward.

Read the full article here