Since August 1st, the S&P 500 has fallen 10%, essentially in a technical correction. Corrections are not fun to go through, but at the same time, they provide second chances on some high-quality stocks that are now trading at great valuations.

Patient investors are often presented with a few of these opportunities every year, and now looks like one of those opportunities.

In today’s article we are going to cover 5 of the Best stocks to buy that are not only trading at huge discounts, but also have some huge upside as well.

5 of the BEST Stocks To Buy In November 2023

November Stock #1 – RTX Corp (RTX)

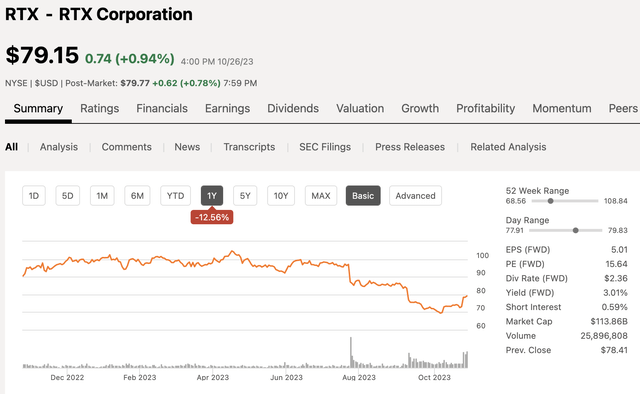

RTX Corp, formerly Raytheon Technologies, is one of the largest defense contractors here in the US. The company has a market cap of $114 billion and over the last 12 months the stock is down 12.5%.

Seeking Alpha

Since the end of July, the stock is down nearly 20%, and that is due to the fact that at that time the company announced an engine recall related to their Pratt & Whitney division. The stock fell 12% the day the issue was announced, shedding more than $10 billion in market cap off, which seemed extremely overblown at the time.

That pullback being overblown becomes even more likely due in part to the company recently announcing a $10 billion share buyback plan. A management team worried about the engine issues would not announce an accelerated share buyback plan of this magnitude.

The war in Ukraine as well as the war in the middle east shows the need to have some exposure to defense contractors in some degree and RTX is one of the best.

Analysts are expecting RTX to generate EPS of $5.46 per share which equates to a P/E ratio of 14.4x. For comparable purposes, over the past decade, shares of RTX have traded at an average earnings multiple of 18x.

Seeking Alpha

22 analysts cover the stock and the average 12-month price target is $91 suggesting 15% upside from current levels.

Seeking Alpha

In addition to 15% upside in the share price, RTX also pays an annual dividend of $2.36 per share which equates to a dividend yield of 3.0%. The company has increased their dividend for nearly 30 years and they have a five year dividend growth rate of more than 5%.

Seeking Alpha

November Stock #2 – Lowe’s Companies (LOW)

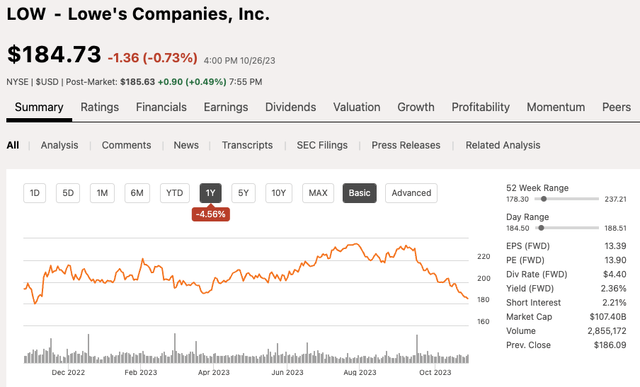

This second stock is one of my favorites as they are a dividend growth stock that offers both strong dividend growth, consistent dividend growth, and share price growth potential.

However, lately, the share price growth has been lacking, but that is fantastic for long-term investors. This is when you stack assets in high-quality positions like Lowe’s Companies as you do not know when things will turn around, but you know they will eventually turn around and you know this valuation is a fantastic opportunity.

Lowe’s currently trades with a market cap of $107 billion but over the past 12 months the stock has fell 5%. However, since September 1, shares of LOW have pulled back 20%.

Seeking Alpha

The recent struggles in the stock is largely due to higher treasury yields and high mortgage rates, which have now topped 8%, weighing on the stock. Lowe’s and its fellow competitor Home Depot (HD) often trade in the direction of the housing sector, which has not been a great sector of late.

However, housing and especially Lowe’s won’t be down for long so investors should take this as a gift and look to potentially add some shares of LOW here, I know I am.

Let’s take a look at how cheap shares actually are. Analysts are expecting LOW to generate 2024 EPS of $14.53 per share which equates to a P/E ratio of just 12.8x. For comparable purposes, over the past decade, shares of LOW have traded at an average earnings multiple of 20x, that is a sizable difference.

Seeking Alpha

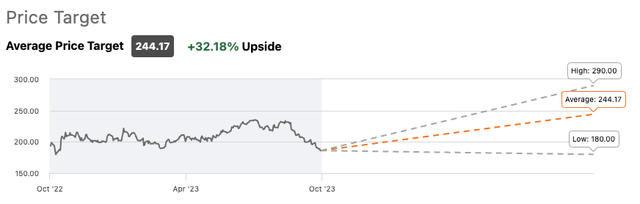

35 analysts cover the stock and have an average 12-month price target of $244 suggesting 32% upside from current levels.

Seeking Alpha

In addition to some major upside, the company is one of the most consistent dividend growers on the market today. In fact, Lowe’s is a dividend king for having increased its dividend for more than 50 consecutive years. The company currently yields a dividend of 2.4% and a five year dividend growth rate of nearly 20%, which is quite impressive.

Seeking Alpha

November Stock #3 – Merck & Co. (MRK)

Merck & Company is a pharmaceutical company that has actually been somewhat of a bright spot in what has been a rough 12 months for the health care sector as a whole. Over that period, the sector as a whole is down 4%.

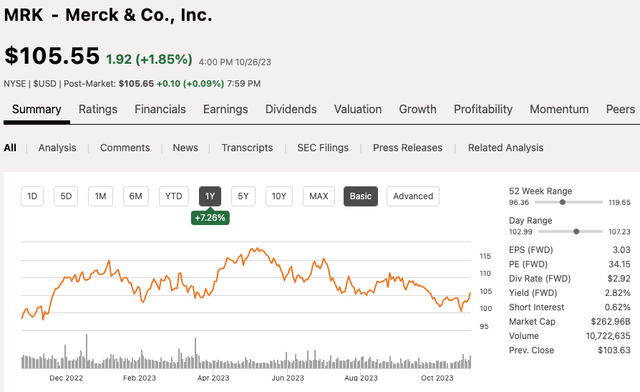

Merck & Co. has a market cap of $263 billion, making them one of the largest pharmaceutical companies on the market, and over the past 12 months shares of MRK have climbed 7%. However, similar to the other stocks we have already looked at, shares of MRK have given back more than 10% over the past 5 months.

Seeking Alpha

Merck recently reported their Q3 earnings which showed a beat on the top and bottom lines. Revenues grew 7% year over year lead by their top selling drug Keytruda which saw 17% growth year over year on $6.3 billion in sales. Based on the strong Q3 results, management also increased their full year guidance increasing both sales and EPS guidance.

Analysts are looking for MRK to generate 2024 EPS of $8.43 per share which equates to a P/E ratio of just 12.3x. For comparable purposes, over the past decade, shares of MRK have traded at an average earnings multiple of 15.3x, not quite the difference we see with Lowe’s but still a sizable difference nonetheless.

Seeking Alpha

28 analysts cover the stock and have an average 12-month price target of $123 implying 16% upside from current levels.

Seeking Alpha

Merck is also a dividend growth stock with a dividend yield of 2.8% and a five year dividend growth rate of 10%. The company has hiked the dividend for 12 consecutive years and counting.

Seeking Alpha

November Stock #4 – The Hershey Co (HSY)

The Hershey Company does not need much of an introduction as they are one of the largest candy companies in the world today. Hershey is a company that has been on my radar for quite a while now as the stock has been in a constant downtrend since the start of May.

Hershey has a market cap of $40 billion and over the past 12 months the stock is down nearly 20%. Since the start of May, shares have dropped more than 30%.

Seeking Alpha

Some of the pressures that have weighed on the stock has been high inflation, which has resulted in higher input costs, forcing the company to try and pass those onto consumers. Another major item that has weighed on the stock has been continued talk of these weight loss miracle drug that has many believing the US will all of a sudden become this extremely healthy nation, which is just bogus to me.

The company recently reported their Q3 earnings that beat on both the top and bottom line. Revenues rose 11% year over year and the company expecting full year EPS growth between 13-15%, which is actually pretty solid given the current environment, so a testament to the company’s management team.

Analysts are looking for HSY to generate 2024 EPS of $10.23 per share which equates to a P/E ratio of 19x. For comparable purposes, over the past decade, shares of HSY have traded at an average earnings multiple of 24.5x.

Seeking Alpha

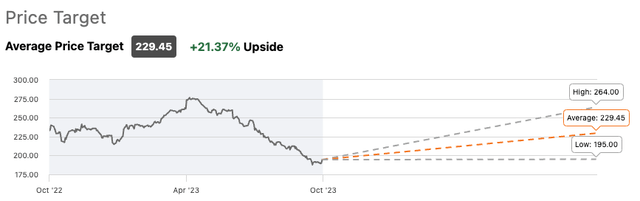

24 analysts cover the stock and have an average 12-month price target of $229 implying more than 20% upside from current levels.

Seeking Alpha

Hershey is another dividend growth stock that has a five year dividend growth rate of 10% and they have increased their dividend for 13 consecutive years. Shares of HSY currently yield a dividend of 2.5%.

November Stock #5 – Meta Platforms (META)

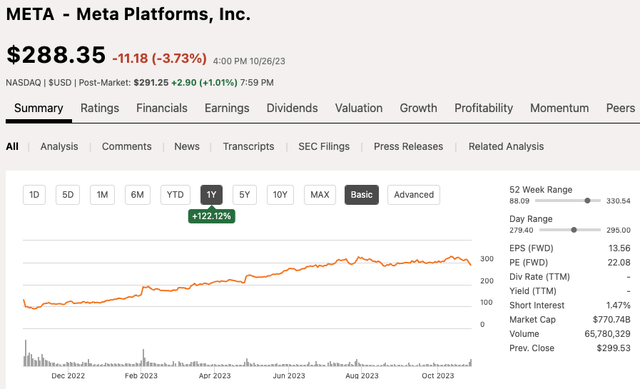

This final stock as you may know, is not a dividend stock and rather a growth stock. Meta Platforms is one of the best performing stocks of 2023, trailing only Nvidia who has returned 181% in 2023 alone. Meta on the other hand has a market cap of $771 billion and shares have climbed 131% in 2023 alone.

Seeking Alpha

META shares have held in tough for most of the year, with much of the pressures coming in recent days and weeks as the stock has fell 12% in the past few weeks. Now, this may not sound like that big of a deal for a stock that is up 130%, but believe it or not, valuation still looks quite intriguing.

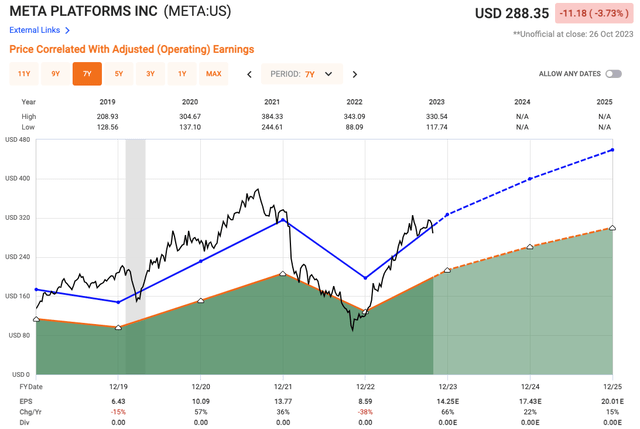

META recently reported quarterly results that beat expectations on both the top and bottom line. Revenue during the quarter grew 23% to more than $34 billion and profits nearly doubled to $11.6 billion.

2023 has been described as the “year of efficiency” as CEO Mark Zuckerberg labeled it, looking to manage costs more responsibly which has brought down spending and seen large amounts of layoffs to bring its labor force more in-line with expectations.

The quarter was largely a blowout, but management gave cautious guidance, suggesting advertising spend could slow, which is obviously a major part of Meta’s business model. We saw a similar fate for the likes of Alphabet (GOOG) (GOOGL), which is a close competitor of Meta’s, but that was more so due to a miss on cloud growth estimates.

So, how cheap could a growth stock like META actually be after posting a near 10 month return of 130% you might ask. Well, it is one of the few “value” plays when it comes to looking at mega cap technology stocks or as they are referred to now, the “Magnificent 7.”

Analysts are calling for META to generate 2024 EPS of $17.43 which equates to a forward P/E multiple of just 16.5x. Over the past five years, shares of META have traded at an average multiple of 23x and over the last decade closer to 28x. This is a company that is expected to generate EPS growth of 66% in 2023, and 22% growth in 2024. This gives META a PEG ratio of 0.75, suggesting shares are quite cheap for the multiple you are paying compared to the growth you are expected to receive.

Fast Graphs

56 analysts cover the stock and have an average 12-month price target of $370 implying nearly 30% upside from current levels.

Seeking Alpha

Investor Takeaway

All five of these companies are high-quality companies trading at great valuations. Now, that does not mean there is no further downside, as there certainly could be with volatility levels increasing of late, but what I do know is current valuations in these stocks are great.

It seems as if we have sidestepped a recession for the time being, but I also do not think that is out of the question entirely in 2024, which is why I want to remain in high-quality stocks that present great value.

Comment Below: Which of these 5 stocks do you like BEST?

Disclosure: This article is intended to provide information to interested parties. I have no knowledge of your individual goals as an investor, and I ask that you complete your own due diligence before purchasing any stocks mentioned or recommended.

Read the full article here