Academy Sports and Outdoors, Inc. (NASDAQ:ASO) is down after its just-reported Q1 earnings. The report was mixed, all things considered. That said, this is a trader’s stock. Just today we were asked about it in our investing group, and we reviewed the situation again. Our last buy call came in the 40s in November 2023. We believe the stock has retraced sufficiently to consider buying again.

Below, we are setting up a new trade for new money once again. The company continues its metered expansion, and has been working through inventory while controlling spend. Moving forward, we are looking for comparable sale to stabilize from here. We rate ASO a buy, but be prepared to leg in, as we do at our service.

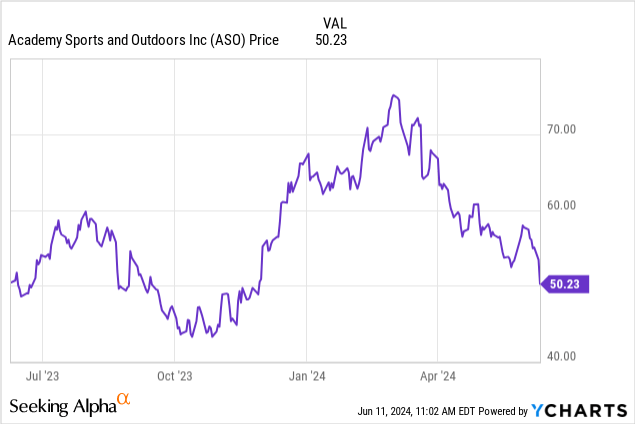

The gap up from $50 looks like it will close on this action, and it is an ok buy here at $53, but a good buy in the high $40s. Here is a suggested play.

The suggested play for new money

Target entry 1: $49.75-$50.00 (30% of position)

Target entry 2: $48.50-$48.75 (33% of position)

Target entry 3: $47.00-$47.25 (37% of position)

Short-term target: $56

Medium term target: $67.

Stop: $42

The above trade is precisely the type we lay out at our service for our highest conviction plays. The above is an example suggested play of how a trade can be considered.

Options consideration: Specific guidance is reserved for our members, but generally speaking, option players should consider selling puts for premium or to define entry here. Calls are also cheap with a low volatility environment right now.

Q1 performance reflects weak comps, again

The just-reported quarter, was below our expectations. We were looking for comps to be better, frankly, even if still down, though we were encouraged by positive comps in some of the newest stores. However, guidance was reiterated, which was positive. Chief Executive Officer Steve Lawrence summed it up nicely in the release:

As expected, our first quarter results reflect that our customers remain under pressure in the current economic environment. We will navigate through the remainder of the year by continuing to lean into our position as the value leader in our space, while also inspiring customers to shop through introductions and expansions of new and innovative products. We will also continue making strategic investments in our long-range growth initiatives. We are pleased that we drove a positive comp in our new stores and omnichannel business. Academy has the right elements in place to achieve our long-range goals: a well-established business model, an experienced leadership team and a strong balance sheet

Competition is tough in this space, and the consumer is definitely under pressure in this macro environment. You see, we have sky-high interest rates which have made housing, including rent, costs surge. Food inflation persists. Consumer debt is at highs. Student loans are being paid back. Gas prices are high. Taxes only seem to go up. And the value of the dollar has eroded badly. However, there is a lot of room for expansion as they are only in 18 states with just 284 stores.

Further, the balance sheet is healthy, and the management is shareholder-friendly, but the quarter was weaker than expected. While there are pressures, we are not taking these results as a sign that the sports and sporting goods market is at risk in any way. Academy has a growing online business and reaches customers with multiple distribution centers that it operates. But sales fell on the top line, missing estimates. Net sales in the quarter were $1.36 billion, which actually fell 1.4% from last year, compared to $1.38 billion. This was due to comparable sales falling 5.7%. It is worth noting the declines were better than the 7.3% decline from last year, but we were looking for 2-3% declines.

Margins have been under pressure of late, but are stabilizing in the 34.0% to 35% range. Gross margins in Q3 were $482.6 million, or 34.5% of the total net sales. This was down a touch from 35.0% of net sales in the prior year quarter. Before taxes, income was $129.9 million, which dipped from $169.9 million. This was largely due to the decline in sales, of course. So really, with the top line down on the back of weaker comps, stemming largely from an inability to move fall merchandise due to much warmer conditions, everything down line on the earnings print suffered.

On a per-share basis, we saw $1.08 compared to $1.30 per share, also missing estimates. Declining earnings is not growth, obviously, and this is a big reason shares have reset. However, we see it as a dip short-term and growth will resume as the company expands. The plan is to open another 100 stores in the next 5 years, growing the company by more than 30%. While the near-term outlook is murky, we like the long-term prospects. We think it is important to note that guidance was largely reiterated despite the weaker than expected quarter. There was one exception, and that was they RAISED the GAAP EPS estimates due to share repurchases.

For this fiscal year, net sales are seen at $6.07 billion to $6.350 billion. This will be because comps will be down 4.0% to up 1.0%. Given this quarter and the consumer pressures aforementioned, we think -2 to -3% is likely. The company sees EPS of $6.05 to $7.05, versus $5.90 to $6.90 in earnings for the year seen prior. Keep in mind, this is unadjusted. Adjusted, we are looking for $6.50 to $7.00. At $6.75 in EPS, and a $50 stock, the valuation is quite attractive when you consider the balance sheet and store footprint expansion.

The balance sheet is healthy. Academy has $378 million in cash with just with $484 million in long-term debt. The company paid down $100 million in debt over the last year. This is strong. The company is using that debt to expand is store footprint and grow. Adjusted free cash flow remains strong and is seen at $330 million this year at the midpoint. Further, the company continues to reward shareholders through dividends and buybacks. The company has been buying back stock, as in the quarter it repurchased $124 million in stock, and also paid $8 million in dividends.

Final thoughts

This is a trader’s stock. As a firm focused on helping investors learn to trade more and ramp their income, there is value in Academy Sports and Outdoors, Inc. shares. We have a company that is stabilizing its comps, managing inventory, and will expand its store base by 30% in the next few years. While it has been a lousy investment, sharp traders have made a killing here. As the stock looks to fall back to under $50, we think you can build a trading position to cash in on a rally over the next few months or so. Plus, you get a dividend while you wait.

Read the full article here