The Virtus Diversified Income & Convertible Fund (NYSE:ACV) is a closed-end fund or CEF, that investors can use to earn a relatively high level of income from the assets in their portfolios. This is immediately apparent in the fact that the fund has a 10.63% yield at the current price. As regular readers will likely immediately notice, this is a higher yield than that possessed by most closed-end funds today. This is because many funds have seen their yields driven down by the current market rally and investors’ expectations of near-term interest rate cuts. Here is how this fund’s yield compares to its peers:

|

Fund Name |

Morningstar Classification |

Current Yield |

|

Virtus Diversified Income & Convertible Fund |

Hybrid-U.S. Allocation |

10.63% |

|

Bexil Investment Trust (OTCPK:BXSY) |

Hybrid-U.S. Allocation |

7.58% |

|

Calamos Strategic Total Return Fund (CSQ) |

Hybrid-U.S. Allocation |

7.36% |

|

Eaton Vance Tax-Advantaged Dividend Income Fund (EVT) |

Hybrid-U.S. Allocation |

8.33% |

|

Gabelli Convertible & Income Securities (GCV) |

Hybrid-U.S. Allocation |

12.83% |

|

RiverNorth Opportunities (RIV) |

Hybrid-U.S. Allocation |

12.71% |

Admittedly, many of these funds have entirely unique portfolio compositions that could account for the wide disparity in yields. The “Hybrid-U.S. Allocation” classification simply means that the fund invests in a combination of common stocks, bonds, and hybrid securities issued by American companies. The return characteristics of different types of securities vary significantly, and this has an impact on the ability of each of these funds to earn the investment income needed to pay a certain yield. In addition, funds such as the Calamos Strategic Total Return Fund have seen their share prices bid up recently, and this reduces their current yields.

With that said, we can see that the Virtus Diversified Income & Convertible Fund has a yield that is above the median for its peer group. This is a good thing for income-focused investors since it means that we are not unnecessarily leaving income on the table and the market appears to believe that the fund’s yield is sustainable. Of course, we will want to take a closer look at it to make sure that this is the case.

As regular readers might remember, we previously discussed the Virtus Diversified Income & Convertible Fund in early May of this year. The equity market has been reasonably strong since that time, but bond prices have struggled. Basically, until very recently, the various participants in the market were expecting that the inflation rate would remain very high, and the Federal Reserve would respond by keeping interest rates at elevated levels. That naturally had an impact on bond yields and bond prices. This might cause many people to assume that the fund’s performance has been somewhat middling since this fund includes both equity and fixed-income exposure.

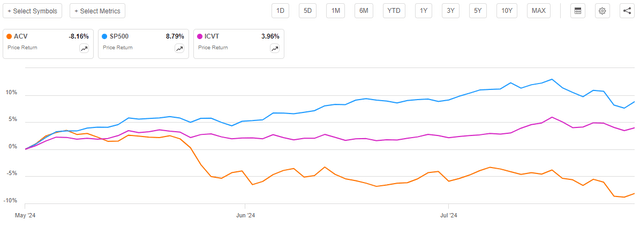

However, in my previous article, I was rather unimpressed with this fund. I downgraded it to a “Sell” rating, citing the fact that the fund has failed to cover its distribution for two straight years (as of January 31, 2024) and has been struggling to earn much in the way of net investment income. It turns out that my call was the right one, as the fund’s share price has declined by a whopping 8.16% since the publication of that article:

Seeking Alpha

As we can clearly see, this was substantially worse than the 8.79% gain of the S&P 500 Index (SP500). The fund also significantly underperformed the 3.96% gain of the iShares Convertible Bond ETF (ICVT), which is perhaps a better benchmark for this fund. This underperformance is certainly going to reduce the fund’s appeal, according to anyone who might be considering taking a position in it. Anyone who read my previous article is not likely to be surprised by it, though, and hopefully was able to get out of the fund before the big decline in late May.

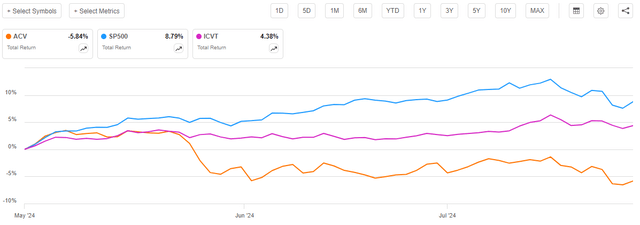

With that said, investors in this fund did not do as poorly as the above chart suggests. As I stated in the previous article:

A simple look at a closed-end fund’s price performance does not necessarily provide an accurate picture of how investors in the fund actually did during a given period. This is because these funds tend to pay out all of their net investment profits to the shareholders, rather than relying on the capital appreciation of their share price to provide a return. This is the reason why the yields of these funds tend to be much higher than the yield of index funds or most other market assets.

As the fund’s distribution provides a real return to the shareholders, it is important to include it in our performance chart. When we do that, we get this alternative chart:

Seeking Alpha

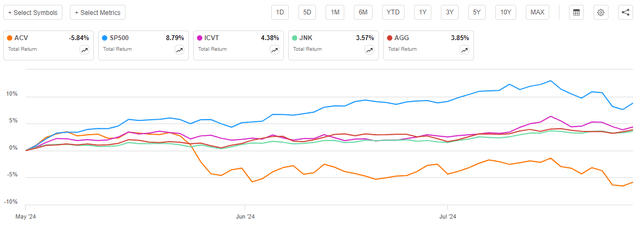

Overall, this chart still shows that selling the fund back at the start of May was a smart move. Even when the distribution is included in the fund’s performance, investors are down 5.84% since that date. This is substantially worse than either common stocks or convertible bonds delivered over the same period. To add to the disappointment, both investment-grade bonds, iShares Core U.S. Aggregate Bond ETF (AGG) and junk bonds SPDR Bloomberg High Yield Bond ETF (JNK) delivered a positive total return over the period in question:

Seeking Alpha

Thus, this fund’s recent performance has been very disappointing, and it would have been best to avoid holding the fund through this quarter.

However, a fund’s past performance is no guarantee of its future results. The overall conditions in the market have changed a bit since our last discussion. Also, this fund has released its first-quarter 2025 holdings report that details any changes that the fund might have made to its portfolio over the past few months. Therefore, let us revisit this fund today and see if it might be time to buy back in.

About The Fund

According to the fund’s website, the Virtus Diversified Income & Convertible Fund has the primary objective of providing its investors with a very high level of total return. This makes a lot of sense given the fund’s strategy, which is explained in great detail on the website:

The Fund seeks to provide total return through a combination of current income and capital appreciation while seeking to mitigate the risk of capital loss. The Fund strives to dynamically allocate across convertibles, equities, and income-producing securities.

The Fund will normally invest at least 80% of its net assets (plus any borrowings for investment purposes) in a diversified portfolio of convertible securities, income-producing equity securities and income-producing debt and other instruments of varying maturities, of which at least 50% of total managed assets are invested in convertibles. The Fund has the latitude to write covered call options on the stocks held in the equity portion.

This description clearly states that the Virtus Diversified Income & Convertible Fund invests in a combination of convertible securities, common stocks, and various types of fixed-income securities. And, this is precisely what we would expect from a hybrid fund, and on the surface, it appears to be similar to the strategy used by many of the other Virtus funds as well as the Calamos funds. This works pretty well with the fund’s total return objective because these three types of securities will provide their total return through a combination of current income (dividends, distributions, coupons, and other direct payments to their owners) and capital gains. Total return is the combination of both income and capital gains, so it works pretty well.

The fiscal 2025 first-quarter holdings report (linked earlier) states that the fund had the following asset allocation as of April 30, 2024:

|

Security Type |

% of Net Assets |

|

Convertible Bonds |

71.2% |

|

Corporate Bonds & Notes |

28.6% |

|

Convertible Preferred Stock |

6.1% |

|

Preferred Stock |

0.0% |

|

Common Stocks |

35.9% |

|

Warrants |

0.0% |

|

Money Market Fund |

4.6% |

While the fund’s strategy description does state that the fund can write covered call options against its common stock holdings, the fund did not have any option positions outstanding as of April 30, 2024. This probably worked out in the fund’s favor. As I discussed in various previous articles, writing a covered call option causes the fund to sacrifice some upside potential of the common stock. It cannot realize all the gains that it otherwise would have if the option had not been written. The S&P 500 Index is up 8.41% since April 30, 2024:

Seeking Alpha

Thus, by not having any call options written against its stock positions, the fund was probably able to make some gains from its common stock holdings over the past three months. This is obviously favorable to the opposite scenario in which the fund had earned premium income but sacrificed the capital gains, which most likely would have been less profitable. As one of this fund’s problems over the past two years has been the destruction of net asset value, it needs all the gains that it can get right now. This should help.

We do notice some fairly major changes to the fund’s portfolio compared to what it had at the time of our previous discussion. As you may recall, at the time of that article, the fund’s most recent portfolio information corresponded to January 31, 2024, so we now have information about the changes that it made during the months of February, March, and April. Here is a simple chart detailing these changes:

|

Asset Type |

Weighting As Of January 31, 2024 |

Weighting As Of April 30, 2024 |

% Change |

|

Convertible Bonds |

82.8% |

71.2% |

-11.6% |

|

Corporate Bonds & Notes |

18.5% |

28.6% |

+10.1% |

|

Convertible Preferred Stock |

5.9% |

6.1% |

+0.2% |

|

Preferred Stock |

0.0% |

0.0% |

No Change |

|

Common Stocks |

38.2% |

35.9% |

-2.3% |

|

Warrants |

0.0% |

0.0% |

No Change |

|

Money Market Fund |

0.0% |

4.6% |

+4.6% |

In the previous article, I noted that the Virtus Diversified Income & Convertible Fund appeared to be increasing its corporate bond holdings and reducing its convertible security allocation over the course of 2023. This trend appears to be continuing today, as the fund’s bond holdings increased substantially during the first quarter of its current fiscal year. The fund’s convertible security holdings decreased by a similarly large amount.

That is, to put it mildly, rather surprising as convertibles have beaten both investment-grade bonds and junk bonds year-to-date:

Seeking Alpha

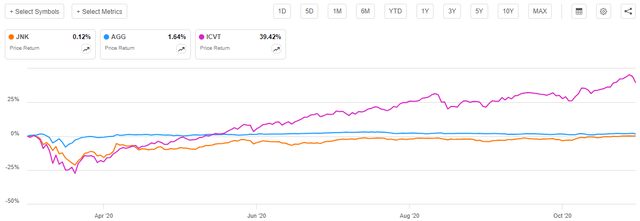

The fund, meanwhile, has apparently been decreasing its allocation to the best-performing asset class out of these three while increasing its allocation to the underperforming assets. That is not the best move right now, and it will probably not be a good move if the Federal Reserve reduces interest rates in the near future. The last time that the Federal Reserve cut interest rates was at two meetings on March 3, 2020, and March 15, 2020. Here is how convertible bonds performed in relation to investment-grade and junk bonds over the remainder of that year:

Seeking Alpha

As we can clearly see, convertible bonds outperformed both investment-grade corporate bonds and junk bonds by a lot the last time that the Federal Reserve cut interest rates. Admittedly, this may not be a perfect comparison because we do not have numerous businesses being forced to go without the revenue needed for debt service, but still, the conclusion is fairly clear. If interest rates are reduced, convertibles will probably outperform investment-grade or junk bonds, if for no other reason than the fact that they are a better inflation hedge.

No matter how we look at it, it appears that the Virtus Diversified Income & Convertible Fund is making the wrong move right now. It should have been increasing its convertible allocation during the first quarter of the fiscal year, not decreasing it. This will probably lag on its performance, or at least prevent it from doing as well as it should have been able to deliver.

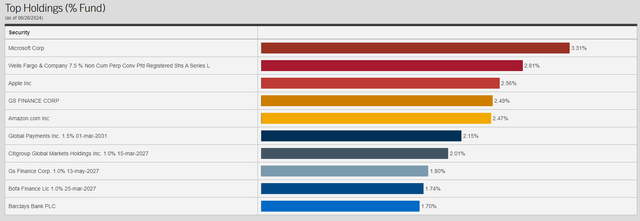

Here are the largest positions in the fund as of June 28, 2024:

Virtus Investments

There have been numerous changes to the fund’s largest holdings since the last time that we discussed this fund. The most significant of these is that Block, Inc. (SQ), Uber Technologies, Inc. (UBER), The Southern Company (SO), and Welltower Inc. (WELL) have all been removed from the list. In their place, we have Apple Inc. (AAPL) as well as a few issues from The Goldman Sachs Group, Inc. (GS), Citigroup Inc. (C), and Bank of America Corporation (BAC). These new additions are not all common stock, as we can clearly see in the chart above. Indeed, many of these new additions appear to be convertible securities, so they will have some characteristics of both stocks and bonds. The downside, of course, to their convertible nature is the incredibly low coupon yields possessed by these bonds. This is one of the reasons why this fund has a lower investment income than would be expected. It delivers a higher proportion of its total return in the form of capital gains than most funds that invest primarily in fixed-income assets.

The fact that four of the fund’s largest positions were changed during a three-month period suggests that this fund has a very high turnover. This is certainly the case as its most recent annual report states that the fund has a 119.0% turnover. This is substantially higher than its peers:

|

Fund Name |

Portfolio Turnover |

|

Virtus Diversified Income & Convertible Fund |

119.00% |

|

Bexil Investment Trust |

26.00% |

|

Calamos Strategic Total Return Fund |

29.00% |

|

Eaton Vance Tax-Advantaged Dividend Income Fund |

29.00% |

|

Gabelli Convertible & Income Securities Fund |

37.00% |

|

RiverNorth Opportunities Fund |

73.00% |

(All figures from the most recent annual report for each fund).

This could mean that this fund has a much higher expense ratio than its peers, but it only sits at 1.67% excluding the costs of leverage. That is not really too bad, as shown here:

|

Fund Name |

Expense Ratio Excluding Leverage |

|

Virtus Diversified Income & Convertible Fund |

1.67% |

|

Bexil Investment Trust |

2.13% |

|

Calamos Strategic Total Return Fund |

1.53% |

|

Eaton Vance Tax-Advantaged Dividend Income Fund |

1.12% |

|

Gabelli Convertible & Income Securities Fund |

1.87% |

|

RiverNorth Opportunities Fund |

1.85% |

(All figures from CEF Data).

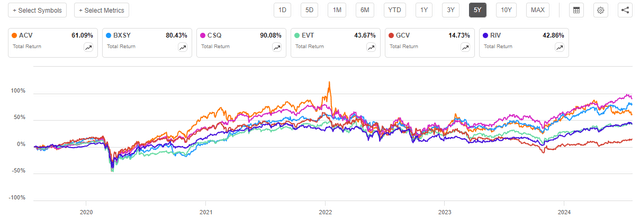

As we can see, the Virtus Diversified Income & Convertible Fund is not the cheapest fund out of this peer group. However, its expense ratio is below the median value, so it is not really that bad. The fund’s performance after expenses is not too bad either, as the fund has delivered a 61.09% total return over the past five years:

Seeking Alpha

There were only two funds that outperformed the Virtus Diversified Income & Convertible Fund on a total return basis over the past five years. As these performance figures tell us what the investors actually received after paying the fund’s expenses, it does not appear that we really need to obsess over the fund’s expense ratio.

For comparison purposes, the S&P 500 Index returned 80.42% and the iShares Convertible Bond ETF had a 55.44% total return. Therefore, the Virtus Diversified Income & Convertible Fund provided its investors with a total return that is between the two indices, even after expenses. This is not too bad, and once again it tells us that we should not need to obsess over the fund’s expense ratio.

Leverage

As is the case with most closed-end funds, the Virtus Diversified Income & Convertible Fund employs leverage as a method of boosting the effective yield and total return produced by its portfolio. I explained how this works in my previous article on this fund:

Basically, the fund borrows money and then uses that borrowed money to purchase convertible securities, common stock, and other publicly traded securities. As long as the total return that the fund receives from the purchased assets is greater than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to an excessive amount of risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its total assets for this reason.

As of the time of writing, the Virtus Diversified Income & Convertible Fund has leveraged assets comprising 31.85% of its overall portfolio. This is relatively in line with the 31.56% leverage ratio that the fund had the last time that we discussed it. That is, admittedly, surprising as the fund’s share price has declined since that time so substantially. In today’s market, it has become rather common to see a fund’s share price outperform its net asset value, but the reverse is not really ever seen.

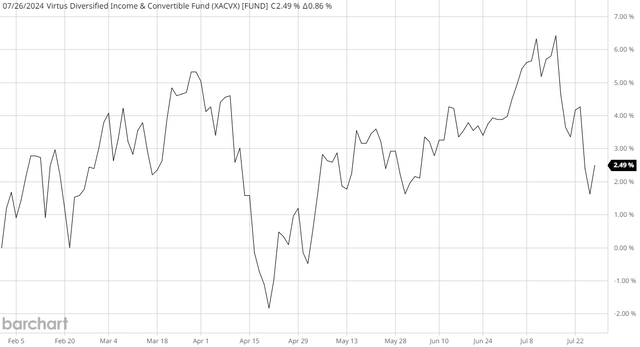

However, this fund appears to be an exception. This chart shows the fund’s net asset value from May 1, 2024, until today:

Barchart

As we can see, the fund’s net asset value has risen by 2.99% since the publication date of my previous article on it. This is in direct defiance of the steep share price decline that we have seen since that date. That certainly has a major impact on the fund’s valuation, which we will discuss later in this article. The important thing to take away right now is that it makes a lot of sense that the fund’s leverage did not exhibit the increase that we would expect from the share price performance. This is because its net asset value has actually held up very well.

Here is how the leverage ratio of the Virtus Diversified Income & Convertible Fund compares with its peers:

|

Fund Name |

Leverage Ratio |

|

Virtus Diversified Income & Convertible Fund |

31.85% |

|

Bexil Investment Trust |

0.00% |

|

Calamos Strategic Total Return Fund |

30.08% |

|

Eaton Vance Tax-Advantaged Dividend Income Fund |

19.06% |

|

Gabelli Convertible & Income Securities Fund |

8.00% |

|

RiverNorth Opportunities Fund |

32.00% |

(All figures from CEF Data).

As I pointed out previously:

This is unfortunate, as we can clearly see that the Virtus Diversified Income & Convertible Fund is employing more leverage than its peers. This could suggest that the fund is using more leverage than is actually safe from a risk management perspective. However, it is not completely out of line with the Calamos Strategic Total Return Fund, which uses a very similar strategy. The fund’s leverage has also come down a bit over the past three months.

Risk-averse investors may want to be cautious here, but overall, the fund does not appear to be too bad in terms of leverage.

Distribution Analysis

As we observed in the previous article:

This represents the second year in a row for which the fund failed to cover its distributions fully. On February 1, 2022, the fund had net assets of $282.348 million. This was down to $216.157 million as of January 31, 2024. This is a bad sign, as it suggests that the fund will almost certainly need to cut the payout before it runs out of investible assets.

The fund failed to cover its distribution for the two-year period that ended on January 31, 2024. This situation appears to be improving for the current fiscal year. Here is the fund’s net asset value from January 31, 2024, until today:

Barchart

As clearly shown, the fund’s net asset value has increased since the start of the current fiscal year. This tells us that the fund has managed to cover all the distributions fully that it has made this year, along with some excess. If this continues, which is possible given current market expectations, then it should be okay to maintain its distribution. This is an improvement over what we saw previously.

Valuation

Shares of the Virtus Diversified Income & Convertible Fund are currently trading at a 4.10% discount to net asset value. This is a much more attractive valuation than the 2.03% discount that the shares have had on average over the past month. It is certainly better than the premium that this fund’s shares had the last time that we discussed it.

The current price seems fairly reasonable given the fund’s portfolio performance year-to-date.

Conclusion

In conclusion, the Virtus Diversified Income & Convertible Fund has delivered a very disappointing performance since the last time that we discussed it. However, it appears that most of this was caused by the fund losing the premium valuation that it formerly had. Its portfolio performance has been much better than the share price suggests. I will admit though that I am not impressed with the fund’s move into fixed-rate bonds and away from convertible bonds, which have been delivering a better performance. That is, in fact, my only complaint about this fund right now, as it otherwise looks much better than it did back in early May.

At this time, it is appropriate to upgrade this fund to a “Hold.” The current valuation is quite reasonable, it appears to be covering the current distribution, and the performance of the portfolio makes it seem certain that any further near-term declines will be temporary.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here