A person holding $100 U.S. currency notes.

Seeking Alpha readers who have followed my work over the years have probably noticed that I’m a guy who eats his cooking. I own over 100 stocks in my dividend growth stock portfolio. That is why when I’m covering a company, it’s because I believe in it and have a vested interest in its success as a long-term shareholder (or would like to eventually own it).

The supplemental insurer Aflac (NYSE:AFL) is a company that I don’t own a sizable stake in within my portfolio (0.4% of my dividend income). However, I am confident in the business and would like to up the weighting of it within my portfolio. For the first time since February 2022, let’s dig into Aflac’s fundamentals and risks to understand why I would be willing to add to my position at the right price.

Aflac’s Awesome Dividend Growth Track Record Can’t Be Faked

Aflac’s 2.2% forward dividend yield isn’t especially attractive compared to the financial sector median of 4%. That explains why Aflac earns a D grade for dividend yield from Seeking Alpha’s Quant system.

But for investors who can overlook this lower starting income, there are plenty of reasons to like the stock.

As many readers are probably aware, Aflac easily meets the requirements necessary to qualify as a Dividend Aristocrat. The company is an S&P 500 component with 40 consecutive years of dividend growth, which is well above the 25-year minimum. While companies can massage earnings figures in a variety of ways to their advantage, they can’t fake dividend growth for 40 years: Either a company can’t pay a growing dividend decade after decade or it can do so. Suffice it to say, that Aflac is a company with remarkable dividend consistency.

Not to mention that the supplemental insurer’s dividend has compounded at 9% annually over the past 10 years – – better than the financial sector median of 7.9%. This is how Aflac earns a B+ grade for dividend growth from Seeking Alpha’s Quant system.

Respectable dividend growth should continue in the years ahead for two reasons. First, the analyst consensus for adjusted diluted EPS growth is 6% annually over the medium term. Second, Aflac’s adjusted diluted EPS payout ratio is quite low: The company is slated to pay $1.68 in dividends per share in 2023. Against the analyst consensus of $6.04 in adjusted diluted EPS for 2023, this is a 27.8% adjusted diluted EPS payout ratio. That should leave the company with the necessary buffer to meet my annual dividend growth rate forecast of 7.25% over the long haul.

A Fundamentally Intact Business

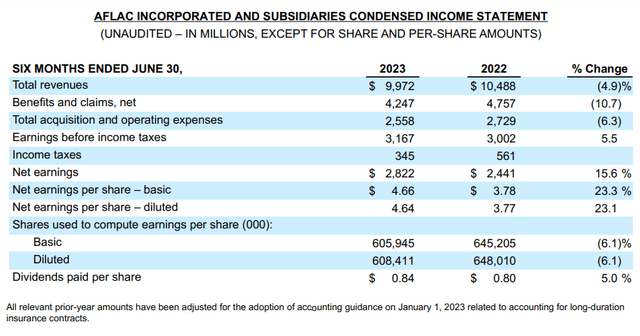

Aflac Q2 2023 Earnings Press Release

Through the first half of 2023, Aflac has delivered decent operating results to its shareholders. The company’s total revenue dipped 4.9% over the year-ago period to $10 billion in the first half. A drop in the topline may not seem all that encouraging, but there is more to the story.

Back in 2019, news spread that Japan Post improperly sold hundreds of thousands of Aflac policies. This has pressured revenue in Japan for a few years now. That explains how Aflac Japan’s total revenue declined by 13.8% year-over-year during the first half of 2023. But with Japan Post Group recently launching the new cancer insurance product in April, Aflac Japan could eventually be on its way to recovery.

Aflac U.S. recorded $3.3 billion in total revenue for the first half, which was up 1.7% over the year-ago period. Along with higher corporate and other revenue and net investment gains, this is how Aflac’s overall revenue only slightly decreased in the first half.

Aflac’s adjusted diluted EPS excluding unfavorable foreign currency translation grew by 11.3% year over year to $3.24 during the first half. Aflac’s increasing digital adoption of new business applications and claims helped its expense ratio to fall below 20% for the first half. Coupled with a substantially lower share count from share repurchases, these factors are why currency-neutral adjusted diluted EPS growth far outpaced revenue growth.

Besides its solid operating results, Aflac is a financially robust business. As of June 30, the company had $4.7 billion in cash and cash equivalents. This was much greater than its minimum target amount of $1.8 billion, which is why Aflac has been assigned A- and A3 credit ratings from S&P and Moody’s on stable outlooks (details in this section sourced from Aflac Q2 2023 earnings press release and Aflac Q2 2023 10-Q filing).

Risks To Consider

Aflac may be doing reasonably well operationally, but there are risks that investors need to be comfortable with before becoming a shareholder.

First off, Aflac Japan comprised 69% of its total revenue in 2022 and Aflac Japan held 80% of the company’s total assets in 2022. This means that the company’s financial prospects correlate with Japan’s overall economy. If the country’s economic fortunes are pressured, Aflac could also be harmed as a result.

Another risk to the company is that while it is rolling out technology to make its business more digital, most policies are sold through face-to-face interaction. In times of public health emergencies like COVID-19, this hurt Aflac’s results. If another pandemic were to hit, this could again be true (a complete discussion of risks can be found in the Risk Factors section of Aflac’s most recent 10-K filing).

The Valuation Looks A Bit Too Rich

As is the case with any stock, it is important to not pay too much. This is because by avoiding paying much more than fair value, the odds of long-term investment success rise significantly. That is why I will use two valuation models to assess the fair value of Aflac’s shares.

Money Chimp

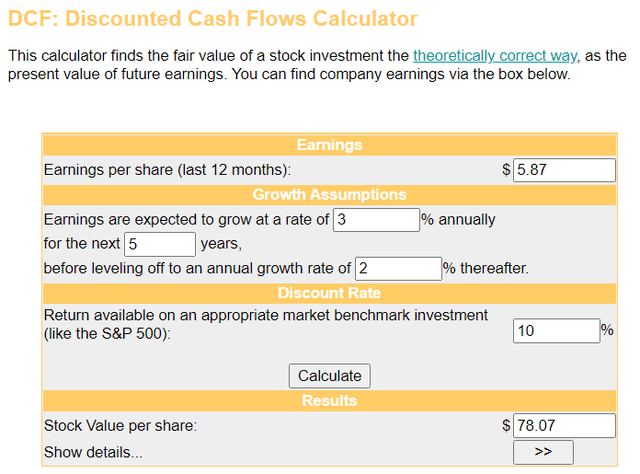

The first valuation model that I’ll utilize to value shares of Aflac is the discounted cash flows or DCF model. This consists of three inputs.

The first input into the DCF model is the last 12 months of currency-neutral adjusted diluted EPS. That amount is $5.87 for Aflac.

The next input for the DCF model is growth predictions. I’ll assume a 3% annual growth rate for five years, which is about half of the analyst consensus. I will then factor in a deceleration to 2% annually in the years thereafter.

The final input into the DCF model is the discount rate, which is the annual total return rate. This differs from one investor to another, but my personal preference is 10%.

Using these inputs for the DCF model, I came out with a fair value of $78.07 a share. That means Aflac’s shares are trading at a 2.9% discount to fair value and offer a 2.9% upside from the current price of $75.84 a share (as of October 2, 2023).

Investopedia

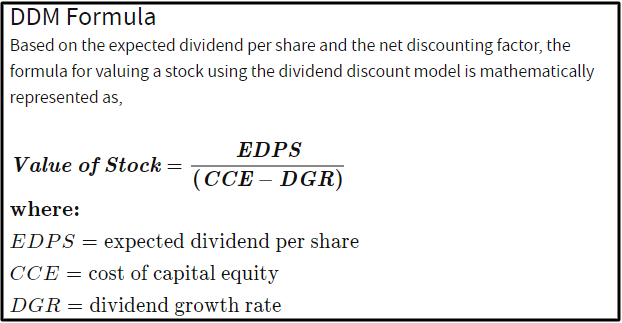

The other valuation model that I will employ to estimate the fair value of shares of Aflac is the dividend discount model or DDM, which also has three inputs.

The first input for the DDM is the annualized dividend per share, which is $1.68 for Aflac.

The second input into the DDM is the cost of capital equity or annual total return rate. I will again use 10% for this input.

The third input for the DDM is the annual dividend growth rate. As I alluded to earlier, I’ll assume 7.25% for this input.

Plugging these inputs into the DDM, I get a fair value of $61.09 a share. This implies that Aflac’s shares are priced 24.1% above fair value and could pose 19.4% capital depreciation from the current share price.

When I average these two fair values together, I compute a fair value of $69.58 a share. That suggests shares of Aflac are trading at a 9% premium to fair value and could have an 8.3% downside from the current share price.

Summary: Aflac Is A Buy Below $70 A Share

Aflac is a dream stock for dividend investors: The dividend has an established track record of growth, it is well-covered by profits, and rising earnings should give it more room to grow moving forward.

But after rallying 17% since I last covered the stock as the S&P 500 has sunk 5%, Aflac isn’t the value that it was not so long ago. Until the stock dips back below $70 a share, that is the only reason I rate it a hold for the time being.

Read the full article here