Enphase (NASDAQ:ENPH) is officially a fallen angel. The company had been one of the strongest secular growth stories in the market and was rewarded with a premium multiple because of that. But the higher interest rate environment has thrown a wrench into the growth story, at least in the near term, as well as raising questions into the competitive landscape. The stock looks cheap based on consensus estimates, but there remains the possibility that consensus estimates prove too optimistic. The stock is trading at around 25x earnings, a reasonable valuation given the long term secular growth tailwinds at play here. That attractive valuation plus the net cash balance sheet have me upgrading my rating from “hold” to “buy,” but I caution that the near term is likely to be volatile, and it isn’t clear that we have reached the bottom as of yet.

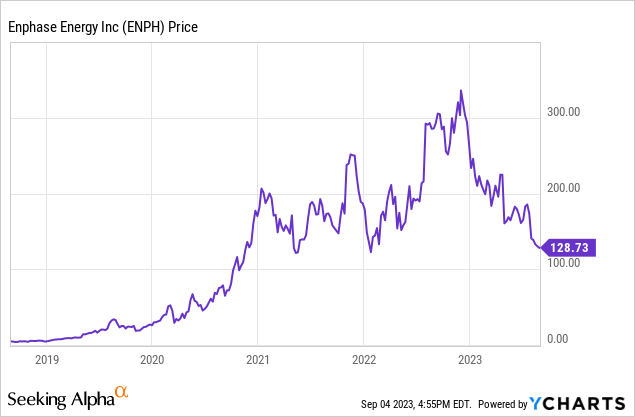

ENPH Stock Price

ENPH has crashed hard from all time highs, but the stock is still up over 30x over the past 5 years (that’s not a typo).

I last covered ENPH in June where I explained why I was rating the stock a “hold” in spite of the vicious stock price crash. The stock has crashed another 30% since then, finally entering the high end of my fair valuation range. It seems unlikely that we’ve reached the end of the bearishness phase, but the stock is finally looking as buyable as it ever has following the pandemic.

ENPH Stock Key Metrics

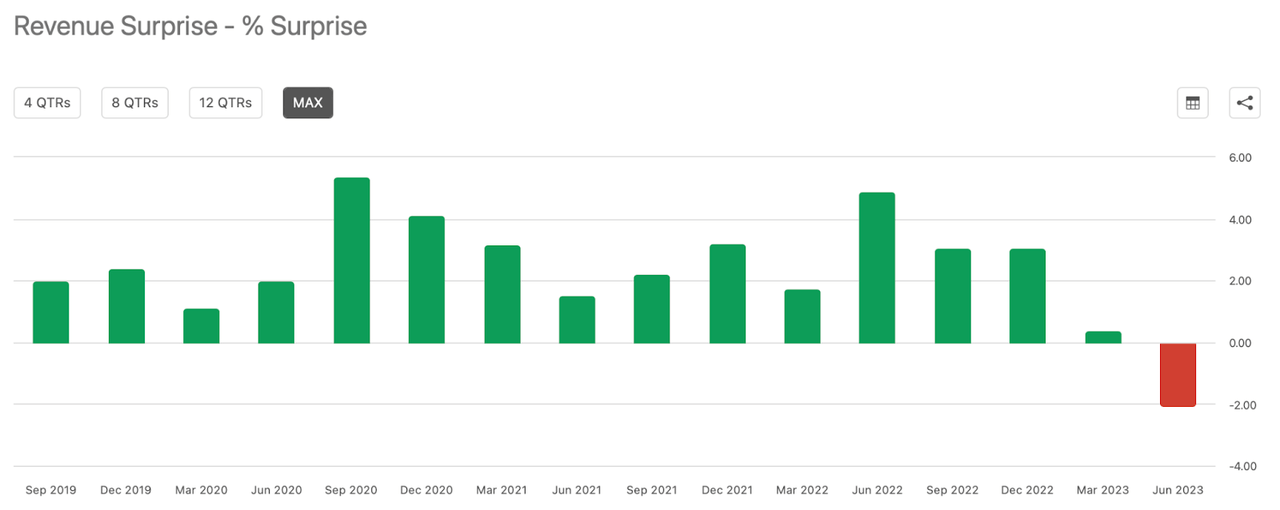

In its most recent quarter, ENPH delivered 36.7% YoY revenue growth to $711.1 million, at the low end of guidance for between $700 million and $750 million.

2023 Q2 Presentation

We can see below that this was the first time in many years that ENPH has reported revenue results below consensus estimates – and the miss was big.

Seeking Alpha

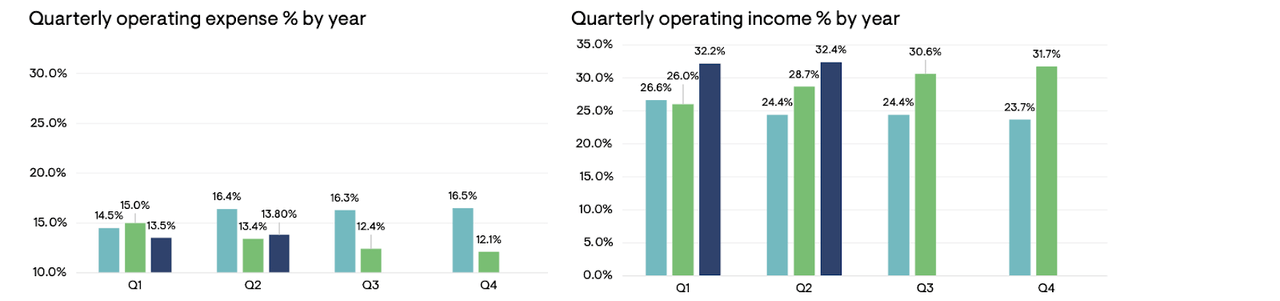

ENPH was able to still deliver solid margin expansion on a YoY and QoQ basis.

2023 Q2 Presentation

ENPH ended the quarter with $1.8 billion of cash versus $1.3 billion of debt, representing a solid net cash balance sheet. The company repurchased $200 million of stock in the quarter at an average price of $159.43 per share and management authorized a new $1 billion program.

These results may not seem so bad on the surface, even if they did miss consensus estimates. The problem is that things are expected to get worse – much worse – moving forward. For the third quarter, management guided for up to $600 million in revenue, which would represent a YoY decline from the $634.7 million in revenue reported last year. Operating margins are expanded to decline to 28% on a non-GAAP basis.

On the conference call, management reiterated that the weakness can be blamed on the higher interest rate environment. Higher interest rates have slowed down housing transactions and reduced demand for solar installations given that they are often purchased with some sort of financing. That said, questions about competition emerged on the call. Management tried to calm such fears by suggesting that they are seeing “stable high market share” and expect their partnerships to “go even deeper during the downturn.” However, investors may be growing fearful that their duopoly with SolarEdge (SEDG) may be under threat from a formidable foe in Tesla (TSLA), which has been able to draw attention due to its storage capabilities. Management did discuss that competition on the call, at least stating that “pricing is normal” for microinverters, and that any price reductions on their batteries are mainly due to having released their third generation product, leading to natural price cuts on their older products. Management guided for their fourth generation battery to be released “within a year” and to come with more attractive gross margins, though it isn’t clear if the price competition may intensify by then.

There are clear obstacles to growth in the near term, as it is anyone’s guess when interest rates come down, if ever. Management however reminded investors that residential solar has “only achieved 4% to 5% penetration in the U.S.” and remains a long term secular growth story. Management suggested that they may see headwinds normalize next year, though I am not of the view that this is such an easy forecast to make.

Is ENPH Stock A Buy, Sell, or Hold?

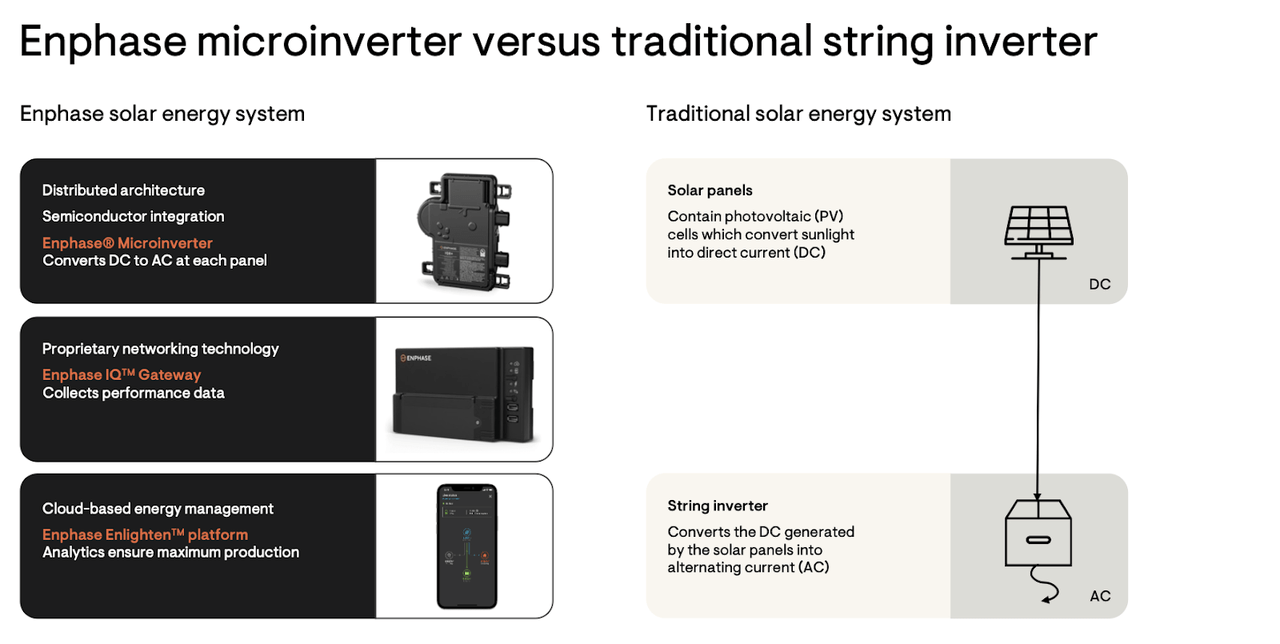

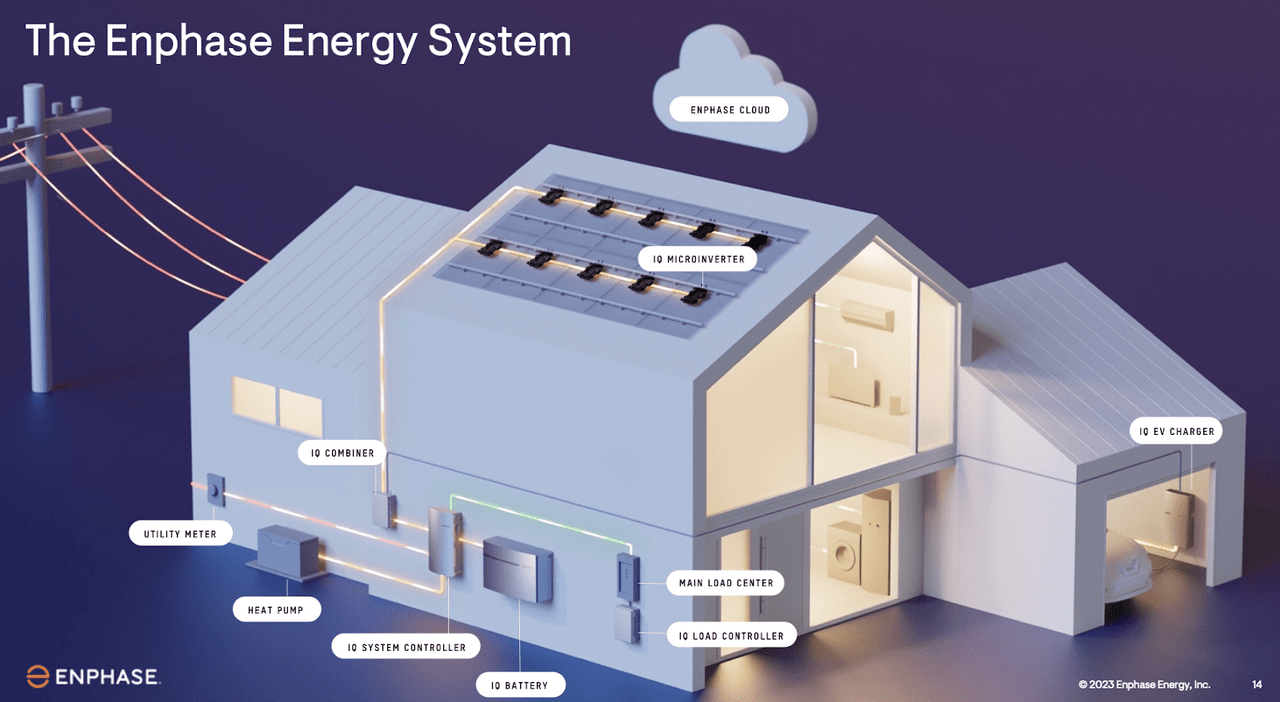

The easy way to think about ENPH is that it helps homeowners make more optimal use of their solar panels by streamlining energy management. These microinverters are kind of like what video streaming is to cable.

2023 Q2 Presentation

While these microinverters are not cheap, ENPH estimates that due to the high value-add of these products, the payback is “between 5 and 7 years.” ENPH’s dominant and well known positioning in the energy ecosystem have enabled it to expand its addressable market to the house’s entire energy system.

2023 Q2 Presentation

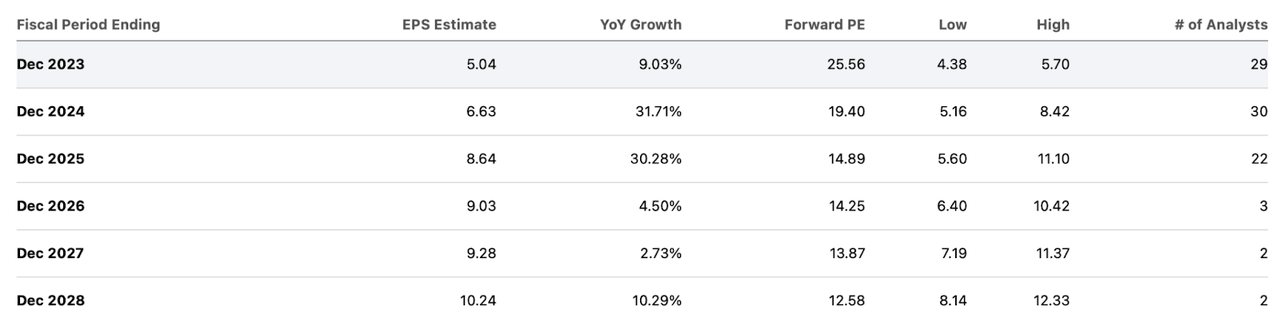

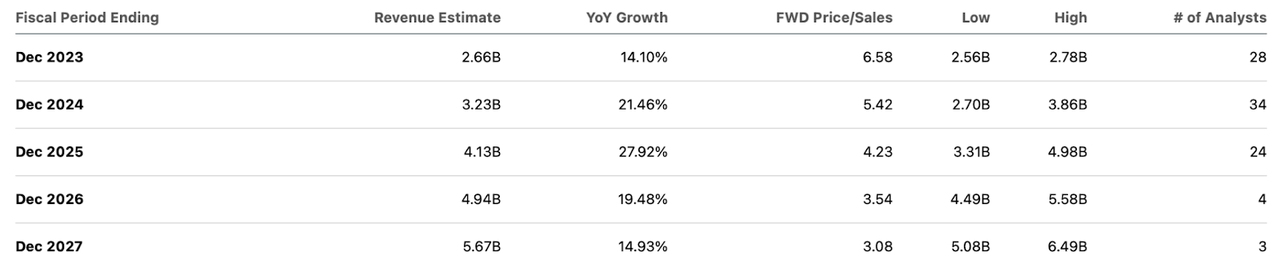

With the company stumbling on growth for the first time since its growth engine took off several years ago, the stock has re-rated downwards sharply. This is a stock that has tended to trade very expensively over the last several years, but now trades at 25.6x forward earnings. Compared against consensus estimates for 30% forward earnings growth, that valuation might look cheap.

Seeking Alpha

That said, I must caution that consensus estimates look quite aggressive. That 30% growth is expected to be powered by 21% revenue growth next year, with sustained growth in the years thereafter.

Seeking Alpha

Yes, I am aware that consensus estimates have already been going down over the past few months.

Seeking Alpha

Yet with the company forecasting growth to temporarily turn negative, I am hard pressed to draw the confidence to believe that near term headwinds will subside so quickly – perhaps they are incorporating expectations for a decline in interest rates (something I am not so willing to assume myself). Investors need to be prepared for the possibility that we are entering a “new normal” and ENPH will need to learn to operate in this higher interest rate environment. It is possible that top-line growth stabilizes around 10%, with earnings growth hovering around 8% to 14% depending on whether operating leverage or price compression drives the narrative. At those lower growth rates, the 26x earnings multiple begins to look not as cheap. My point is that while ENPH continues to be a high quality company in a highly attractive growth sector, the current stock price is not representative of imminent triple-digit returns and one should avoid “backing the truck” here.

Those looking for a further margin of safety may find it notable that put options are trading with generous premiums for this name, likely due to the greater volatility as of late. One could even find contracts deep out of the money offering attractive premiums – take for instance the $75 strike expiring in January 2025 which offers a $7.55 premium. At that price, ENPH would be trading at around 10x earnings, a price which would look legitimately attractive even if growth rates compress to the 10% range.

What are the key risks here? It is possible that solar stocks permanently fall out of favor. This wouldn’t impact ENPH’s fundamental performance, but clearly the potential reward is higher if the stock can fetch a premium multiple. I find it possible, if not likely, that interest rates remain higher for longer. It is not immediately clear if ENPH has tools in its disposal to reignite growth in the absence of a cut to interest rates. The stock likely has further downside – substantial downside at that – if growth rates continue to compress. The most important risk is that of competition. ENPH has shown an ability to compete alongside SolarEdge all these years, but TSLA is admittedly a wild card. TSLA is highly profitable with $20 billion of net cash as of the latest quarter – it is possible that the company decides to engage in an aggressive price war to gain market share. I suspect that the average consumer may be drawn to the TSLA brand as the average person is more likely to know about the Tesla car than an Enphase microinverter (or even know what a microinverter is). Prospective investors need to keep a close watch on competition with TSLA as that can greatly impact forward growth rates.

I rate ENPH a buy due to the growth at a reasonable price valuation, but caution that things are likely to get worse before they get better.

Read the full article here