Last week, Air Liquide released its Q2 financial figures (OTCPK:AIQUF, OTCPK:AIQUY), confirming the 2023 target objectives. Here at the Lab, we positively view the company’s latest development, and one year later, the company stock price delivered a total return performance of 34.17%, outperforming the S&P 500 Index. Today, we are not providing our usual buy-case recap; however, we suggest our readers check our 2023 previous publication: 1) Air Liquide Is Delivering Value To Shareholders, and 2) Lower Gas Price Equals Higher Margin. H1 2023 results are well in line with our indication. Therefore, we remain ahead of Wall Street consensus, confirming a buy target of €190 per share.

Mare Past Analysis

Q2 Results

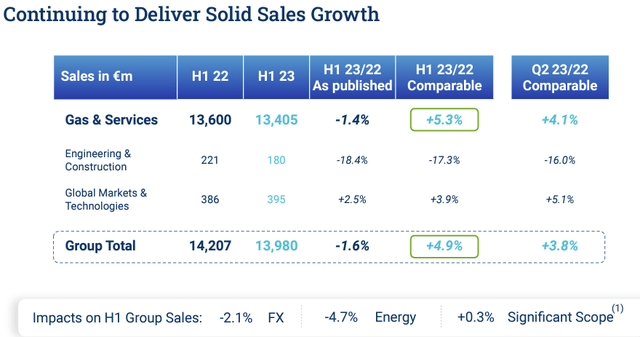

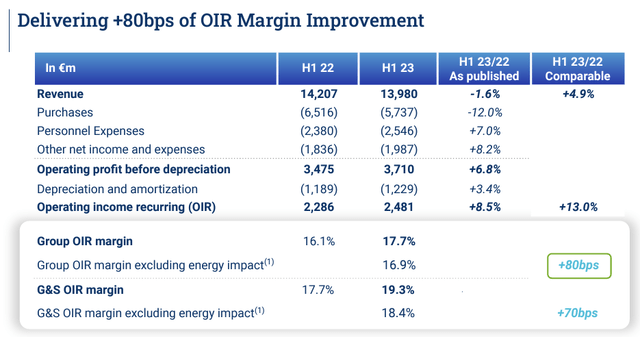

The specialty gas company delivered a core operating profit of €2.48 billion and was up by 9% on a yearly basis and exceeded analyst consensus, which on average was forecasting €2.44 billion. Excluding the energy pass-through, the EBIT margin was up by 80 basis points, reaching 17.7% and ahead of 20 basis points vs Wall Street. Looking at the sales, in Q2, Air Liquide delivered €6.80 billion and was down by 7% (again reporting a beat), with group organic sales that recorded a positive growth of 3.8%. The company’s main drags were energy and FX, down by 4.7% and 2.1%, respectively. This organic growth was lower than in Q1 2023. In detail, the company delivered an OSG of 6.7%; however, this past quarter was very challenging with tough competition and a slowdown in industrial production (especially in the EU area) combined with a softer macro environment.

Air Liquide sales evolution

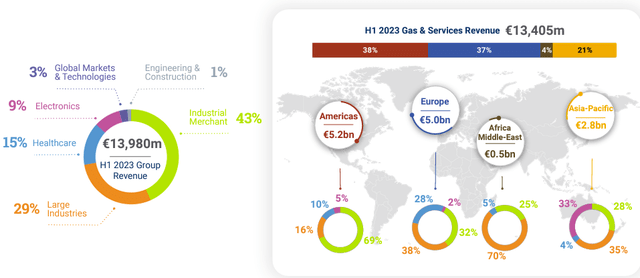

Going down to Air Liquide results, the company recorded a solid operating cash flow generation of 32% on a yearly comparison. This was also the result of higher earnings and lower working capital requirements (energy delta). In numbers, last year at the half-year results, the company recorded an outflow of €635 million, while now the working capital outflow was only at €298 million. Here at the Lab, we were forecasting a solid pricing power coupled with Air Liquide operating leverage. As a reminder, within its peers, the company is the most exposed to the EU area (37%), and in 2022, the EU gas prices recorded the highest level; with a reverse trend, the company is now in a much better position.

Air Liquide H1 Financials in a Snap

Mare Upside

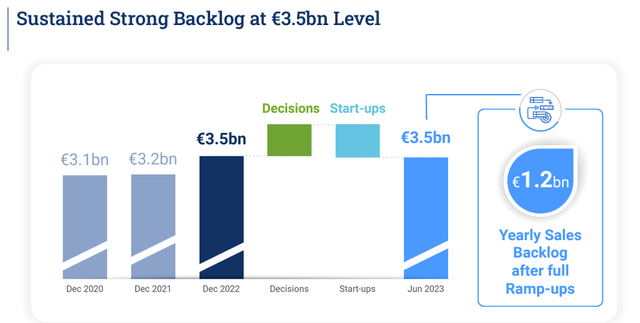

- The company maintained a solid order backlog. Air Liquide’s investment opportunities remained flat at €3.4 billion compared to a Q1 backlog of €3.5 billion. Air Liquide’s new orders are well-balanced between the Electronics division and Large Industries;

- Thanks to the Industrial Merchant performance and growth rate, we see the Fiscal Year company target achievable. This is also supported by the company’s management team, which reiterated that “Air Liquide is confident in its ability to increase its operating margin further and to deliver recurring net profit growth at constant exchange rates;.“

- In addition, still related to point 2), the €300m – €330 million outlook for new projects in Large Industries has also been confirmed;

- CAPEX was in line with estimates. Last year, Air Liquide investments reached €1.6 billion, while now we are at €1.7 billion;

- The consensus is estimating organic growth of 3.9% with a 17% EBIT margin. The company reached a core operating profit margin of 17.7% in H1. Therefore, we believe that analysts should re-precise Air Liquide in line with our indication with an EBIT margin H2 of 17.8%;

- the company has a solid balance sheet to support our buy rating target. Including the dividend already paid in May, Air Liquide maintained the same debt level recorded at December-end. In addition, interest rate payments are mainly fixed (89%).

Air Liquide EU exposure Air Liquide backlog Air Liquide debt

Conclusion & Valuation

Here at the Lab, AL’s stock should benefit from a revaluation. After the Q2 results, the company is likely to react positively, thanks to solid cash generation and a visible margin improvement. For this reason, we confirmed our buy rating. In addition, we see M&A optionality or a balance de-leveraging. Our €190 price target is derived by a 14x multiple on 2024 estimates. APD and Linde are trading at 14.5x and 15.5x, respectively. Downside risks include global industrial production, regional oversupply, execution risk on CAPEX, and lower growth rate. In addition, FX might be a drag on the company’s results.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here