Investment Thesis

Alarum Technologies (NASDAQ:ALAR) is an Israeli company that is dual listed on the Nasdaq Stock Exchange and the Tel Aviv Stock Exchange. Previously a holding company with multiple businesses, Alarum sold or scaled down other business lines and as of Q1 2024, 96% of its revenue now comes from NetNut, it’s enterprise data collection solutions business. Management has communicated that they are “100% NetNut” and that will be the only focus for the company going forward. NetNut offers IP proxy services and data collection tools that help enterprises access websites anonymously and scrape data from them.

Alarum is a usage-based SaaS company benefiting from big data and AI trends. At the heart of all artificial intelligence is the need to collect data. Alarum helps business collect critical data needed to run business analysis, keep tabs on competitors, etc. Despite a legendary 1500% (15x!) run-up over the last 52 weeks, the stock is trading at a 18x forward P/E (our estimates) even though we expect NetNut to grow revenues by 90% next year. This is very cheap for a SaaS company with a very long runway ahead. While they are very different companies, many large-cap SaaS stocks also tied to big data and artificial intelligence themes such as MongoDB (MDB) and Snowflake (SNOW), trade at 10-20x P/S (price to sales, not price to earnings) despite lack of GAAP profitability and only 30-40% expected revenue growth.

Given ALAR’s massive run-up, some investors may think they’ve already missed the party. Looking at fundamental metrics and long runway, however, we think the party just got started and that winners can keep winning. Much of the massive run-up was due to Alarum exiting or scaling down its unprofitable cybersecurity and consumer internet access businesses. Because both were unprofitable, they masked the strong performance of fast-growing NetNut, Alarum’s hidden gem. By exiting these other businesses, Alarum can clearly demonstrate NetNut’s clear strengths in consolidated financial reports, which should drive investor discovery and re-rating. We rate the stock a STRONG BUY with a target price of $40.

Business Overview

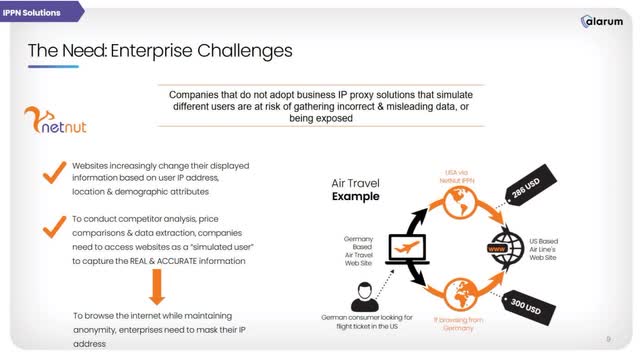

NetNut offers IP proxy services and data collection tools that help enterprises access websites anonymously and scrape data from them. This anonymity is important because websites increasingly change their displayed information based on user IP addresses, locations, and other demographic information or may block IP addresses that are overused. Without IP proxy solutions, companies are at risk of collecting misleading or incorrect data or being blocked.

Alarum’s April 2024 Corporate Presentation offers a good example of travel websites. Travel websites often vary prices for the same airplane ticket depending on the location of the user doing the browsing. A New York to London flight may cost more for users browsing from New York than users browsing from London, despite being the exact same flight. As a consumer, one would benefit from being able to mask one’s IP address in order to achieve better (and in our opinion fairer) prices. As an enterprise constantly collecting data, using the same IP address may lead to the website blocking that IP address as most websites have basic anti-scraper tools. Additionally, without varied IP addresses, enterprises may collect misleading or incorrect data leading to flawed analysis.

Chart 1: NetNut: Why Companies Need IP Proxy Solutions

Why Companies Need NetNut (Alarum April 2024 Corporate Presentation)

Alarum’s Q1 2024 Results Showed Continued Strength

On May 21, 2024, Alarum announced blowout Q1 2024 results. The stock initially fell because Alarum had already pre-announced its revenue numbers in April 2024 and the market was thus already expecting good results. However, the stock subsequently recovered and reached new highs. Across the board, Alarum posted strong growth metrics, with NetNut growing 139% YoY, gross margins increasing to 78% and net profits increasing to $1.4 million from -$0.7 million a year ago. Non-IFRS net profit was $2.8 million compared to -$0.1 million a year ago. Also notable for the DBNRR (Dollar Based Net Retention Rate) of 1.66x, which is phenomenal.

With micro-cap stocks, investors are frequently worried about cash burn as that often leads to significant equity dilution or bankruptcy. Indeed, Alarum was unprofitable for a long time due to its cash-burning cybersecurity business and had to do a $4.25 million capital raise in September 2023 at a price of $2.72 per ADS, which is literally less than 1/10 the price Alarum currently trades at. However, Alarum has turned the corner and cash on the balance sheet increased to $15.1 million compared to $10.9 million on Dec 2023. Adjusted EBITDA, a good proxy for operational cash flow, came in at $3.2 million. We don’t think Alarum will have cash flow problems in the future.

The only negative we saw with the results was uncertainty regarding the development and adoption of its new products. It sounded like new products like the Website Unblocker and AI Data Collector were still in early phases and it’s unclear whether they are being adopted quickly by clients. We’d like to see more clarity in the Q2 2024 results. Overall, we were very impressed with the results.

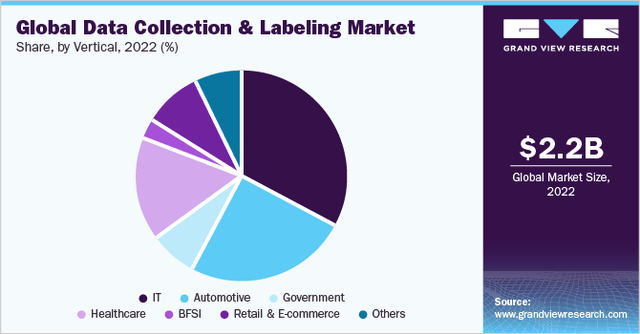

The Data Collection and Labeling Market is Expected To Grow At a 29% CAGR

Driven by AI tailwinds, the data collection and labeling market is growing very quickly. According to Grandview Research, the data collection and labeling market is expected to grow from $2.2 billion to $17 billion from 2023 to 2030, or a 28.9% CAGR. NetNut and its competitors will be beneficiaries of this bonanza and we expect the entire industry to do well. Nearly all sectors have a need for data collection, which means NetNut can garner clients from different sectors, which reduces the riskiness of weakness in any one sector impacting NetNut’s growth.

Chart 2: Global Data Collection & Labeling Market Share by Vertical

Global Data Collection & Labeling Market – Share By Vertical (Grandview Research)

The residential IP proxy market is expected to grow slower, with a report from Knowledge Sourcing Intelligence forecasting a CAGR of 11.5% from 2024 to 2029. However, this still represents growth significantly above GDP and we think the report may underestimate how AI tailwinds will drive further growth.

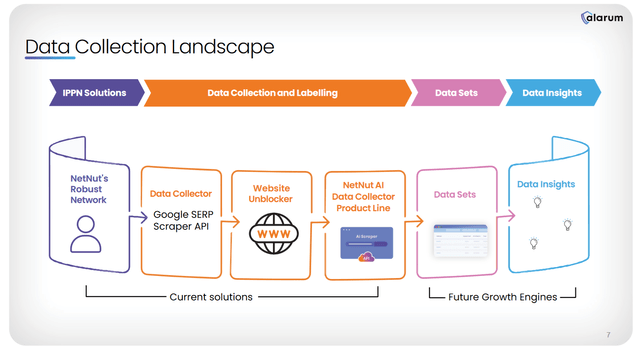

NetNut’s new product launches will drive new growth from new and existing clients

While most of NetNut’s revenue still comes from its proxy network solutions, the company has expanded across the data collection landscape and now offers many data collection and labelling products. In October 2023, NetNut launched its first data collection product, the SERP Scraper API. In January 2024, NetNut introduced its Website Unblocker, which helps enterprises bypass website blocking tools. In February 2024, NetNut announced the launch of its revolutionary AI data collector product line. Most of these products are probably still in initial testing phases for their clients, so we will only see significant revenue impact later in 2024 or early 2025.

Chart 3: Alarum’s Data Collection Product Landscape

NetNut: Data Collection Landscape (Alarum April 2024 Corporate Presentation)

Financials, Valuation and Quant Rankings

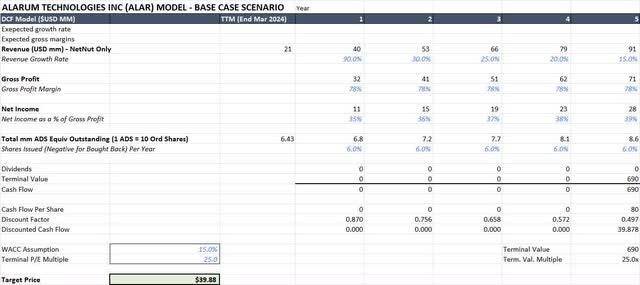

DCF Valuation

Using a 5-year DCF approach we get a target price of $40 using the below assumptions:

- Annual revenue growth rate of 90% for next twelve months that then subsequently decreases to 30% for the 24th to 36th month. Revenue growth subsequently decreases and reaches reaching 15% in Year 5. The overall 5-year revenue CAGR is 33.6%. The particularly high growth in the first year is justified due to 1) NetNut’s growth rate of 139% and 2) their very high DBNRR of 1.66x, meaning existing clients spent 66% more this year on Alarum products.

- 78% gross margins in Year 5 similar to current figures.

- 30% net margins in Year 5 similar to current figures.

- Share count of 64.3 million shares with 6% dilution a year, leading to 86 million shares in Year 5. We note that 1 ADS is equivalent to 10 ordinary shares.

- WACC of 15.0% and a terminal P/E multiple of 25x. We apply a high WACC of 15% because of Alarum’s status as an Israeli micro-cap status. This terminal PE assumption of 25x is higher than the S&P 500’s current multiple of 21x. As a SaaS company with recurring revenues and a long growth runway, we think 25x is justified and even conservative. Additionally, we expect Alarum to graduate into small cap territory within the next few years, which should attract more institutional investors.

Table 1: Alarum Valuation Model

Alarum Valuation Model (Author’s Analysis, Seeking Alpha)

Forecasts are inherently imprecise, but in Alarum’s case there is a particularly wide range of possible outcomes. We do see a scenario in which the stock maintains revenue hypergrowth for several years, in which case the stock could re-rate from a current ~18x forward P/E to something closer to 30x P/E. This is a formula for a clear multi-bagger. On the other hand, execution failures and loss of market share to Bright Data and other competitors could cause revenue to collapse, tanking the stock price with it.

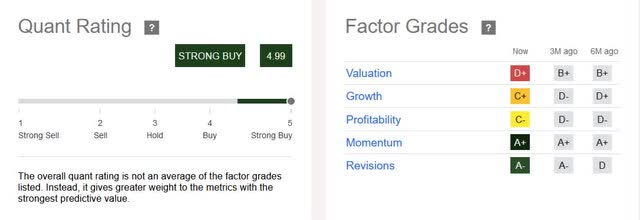

Seeking Alpha Quant Rankings and Factor Grades

Table 2: Alarum Quant Ratings and Factor Grades from Seeking Alpha

Alaurm Seeking Alpha Quant Ratings (Seeking Alpha)

Seeking Alpha’s factor grades show Alarum scores excellently on momentum and revisions while scoring poorly on valuation, growth and profitability. Alarum’s overall quant rating is a Strong Buy and Alarum ranks first in a universe of 45 Information Technology System Software Stocks. We think Seeking Alpha’s quant model is heavily rating momentum as Alarum has went up 12x in the last year and clearly believes the stock run-up can continue.

Negatives and Risks

Competitive Landscape

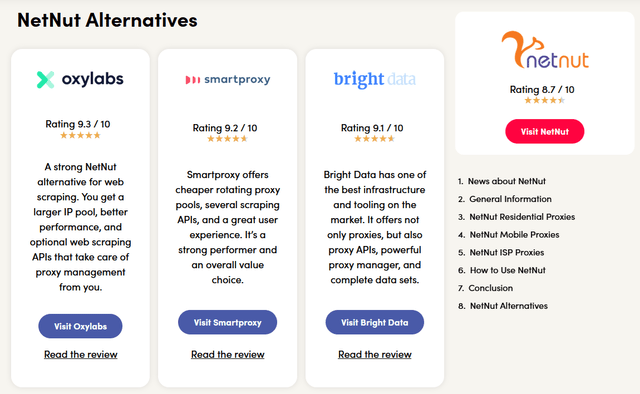

NetNut faces a competitive landscape. Fellow Israeli company Bright Data is the clear leader in the space while Oxylabs and Smartproxy also serve enterprises and are likely larger than NetNut. According to Proxyway’s in-depth NetNut review, Oxylabs, Smartproxy and Brith Data all scored higher ratings than NetNut. We normally prefer to invest in the industry leader, but in this case NetNut’s closest competitors are all private companies. We think demand for proxies and data collection tools are growing fast enough that all players will be winners, but NetNut may lose market share if it’s simply not able to execute as well as its competitors.

Chart 4: NetNut Alternatives

NetNut Alternatives (Proxyway)

Legal Risk

Meta and X (formerly known as Twitter) both sued Bright Data in the United States, claiming that Bright Data’s data scraping activities violated each company’s terms of service. Meta later dropped its case because Meta could not prove (Meta admits defeat against web-scraping firm Bright Data, abandons legal action | CTech) that Bright Data had scraped anything other than publicly available data. X’s case was also dismissed for similar reasons, with a judge ruling that creating information monopolies would disservice the public interest:

“Giving social networks complete control over the collection and use of public web data “risks the possible creation of information monopolies that would disserve the public interest,” the judge wrote. He added that X was not “looking to protect X users’ privacy,” and was “happy to allow the extraction and copying of X users’ content so long as it gets paid.”

Bright Data was likely targeted by Meta and X due to being the largest player in its industry. If Meta/X won their case, every other proxy provider including NetNut would be dramatically affected. While Bright Data won its case in the United States, it remains unclear if Meta or X could successfully sue Bright Data in other jurisdictions, such as the European Union. Success by Meta/X there would significantly reduce the potential total addressable market for NetNut.

Israeli-Based Company

NetNut is an Israeli-based company. Israel accounting standards differ from American standards, and accounting regulations may in some cases be not as stringent. Furthermore, NetNut could still face operational disruptions if, for example, key NetNut employees are called up for the war. As an Israeli company, Alarum’s stock could also face boycotts from certain investor groups, which could depress the stock price.

Conclusions

Despite Alarum’s micro-cap status, tough competition, legal risks and a 15x run-up over the last year, we think Alarum is trading too cheaply relative to its current growth and long future runway. We rarely see SaaS companies growing revenues by 90% and trading at 18x forward P/E (our estimates). Alarum’s continued strong results should attract a larger investor base, and the stock should re-rate from there. We think investors should consider a small position in Alarum stock. Alarum is a 3.5% position in our portfolio, and we rate the stock a STRONG BUY with a target price of $40.

a

Read the full article here