Thesis

Align Technology (NASDAQ:ALGN) has a first-mover advantage in the clear aligner market. Its bullet-proof balance sheet and solid competitive position justify its premium valuation. I am cautiously optimistic about ALGN’s prospects due to its rich valuation. My assumptions yield a modestly attractive ~11% IRR with a 30x FY1 EV/EBIT exit multiple in 2025.

The clear aligners market

Research suggests that there’s roughly a 60% probability that you have some degree of imperfection in the form of malocclusion/misalignment. There are several cosmetic, aesthetic, or medical reasons why someone would be tempted to fix their teeth imperfections, but all of them combined contribute to the formation of the orthodontic treatment market. Conventionally, the dentist/orthodontist would suggest brace treatment, but many began offering the alternative and often superior treatment of clear aligners. The market for invisible plastic aligners is estimated to be worth ~$4.1bn in 2022. The Total Addressable Market comprises roughly 15 million new orthodontic case initiations annually, and ~75% of them represent the teen market.

The orthodontic market is largely underpenetrated by clear aligners, with the majority of cases still being treated with legacy braces. In the US, clear aligners (as an industry) have captured a 20% market share from conventional braces, and penetration globally is less than 10%. This presents a structural growth opportunity for investors if the penetration story unfolds over several years. A significant driver of penetration is the education of consumers about the benefits of clear aligners and the training of physicians to offer treatment and promote their adoption.

Aligners vs braces

So, let’s briefly compare the pros and cons of each method of treatment. For starters, clear aligners are Invisible. Forget the metal wires and awkward-looking metal braces. If need be, they can be removed for comfort or to eat, although patients have to be kept on at least 22h/day. There is also research to support that in non-extraction cases, clear aligners reduce treatment time and require fewer dentist visits.

There are also some downsides to clear aligner treatment. First, in extreme malocclusion cases, the clear aligners may not work. Second, patients need to brush their teeth and floss often. Finally, in many cases, they require buttons on the teeth (which are small white attachments on the teeth for the aligners to hook on).

All in all, the benefits outweigh the disadvantages in most cases, consequently making a strong case for clear aligners. However, the cost is the final component that is important in the patient’s decision-making process. Clear aligners cost anywhere between $3000-$8000 vs. $1500-$7000 for conventional braces.

Growth drivers

Developed countries are seeing massive growth in adults seeking orthodontic treatment, which is mainly driven by the availability of technologically advanced solutions such as clear aligners. Increased adoption is boosted by the following developments:

Trained dentists

An increasing number of dentists are being trained in the application of the technology. Ongoing/incremental investments by existing/new entrants in the space. WHO studies suggest that there are 2.5 million dentists and orthodontists globally, and ~6% of dentists (150 thousand) have been trained to apply Invisalign (the leading brand) to date. As more patients are educated about clear aligners and more dentists are being trained, several research institutions estimate that the invisible aligner market will grow by ~16% over the next seven years.

Technological advancements

Technological improvements allow aligners to address more types of complex orthodontic cases. ALGN is continuously investing in technologies that help its solutions treat more complex malocclusion cases.

Hyperconsciousness of smile

In the post-COVID era, more people sit in front of cameras for work and pleasure. This makes people more conscious of their aesthetic appearance, including their smile. Moreover, record-breaking social media usage is also contributing to this hyperconsciousness.

Competition

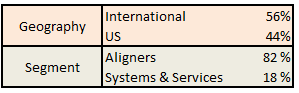

Align Technologies offers industry-leading invisible aligners, which led to its quasi-monopolistic market position across the globe. Besides clear aligners, the company’s offering portfolio includes intra-oral scanners and computer-aided design & manufacturing services. The company’s product portfolio includes Invisalign clear aligners, iTero Intraoral scanners, and OrthoCAD digital services for dental professionals. ALGN continues to push the boundaries of innovation and release new hardware and software offerings that can be applied to various treatments in dentistry practice. Below is a breakdown of revenue by geography and segment.

Revenues by segment and region (Company reports)

The oligopolistic clear aligner market is dominated by Align Technology, but the following companies are challenging for market share: 3M, Institut Straumann, Ormco, 3Shape A/S, Dentsply, and Argen. In the corporate world, the most widely hated (and secretly desired) word is ‘Monopoly’. This is because it attracts unwanted regulatory attention that distracts the leader in the space from extending its leadership. Invisalign holds roughly 85% of the clear aligner market in the US. However, competition is becoming increasingly apparent as many of the players challenging the incumbent are well-capitalized and technologically capable.

Competition Matrix (CapitalMind)

Advantages over competitors

With the aforementioned in mind, the prevailing question becomes – did Align Technology build a moat wide enough to fend off competitors or will they chip away market share over the years? To answer this question, let’s examine Align’s sustainable competitive advantages and the fundamental evidence to support their existence.

Switching costs

Align’s iTero intraoral scanner (costs ~$50,000) is a best-in-class optical impression system sold alongside CAD/CAM software used in dental offices for orthodontic and restorative digital procedures. The digital data captured by the device can be submitted to Align and used in the 3D printing of patient Invisalign cases and in the manufacturing of dental implants and other procedures. While the Invisalign system has third-party interoperability across other intraoral scanners (manufactured by 3M, Dentsply Sirona, and 3Shape), the iTero scanner interfaces exclusively with the Invisalign system for orthodontics. In other words, while Align can manufacture clear aligners based on scans conducted on the top four intraoral scanners, the iTero scanner can not be used to make competitors’ aligners. Invisalign offers discounts for iTero based on the volume of Invisalign cases initiated by its partners. 50% of all Invisalign cases are submitted via iTero.

Intellectual property

Considering that Align pioneered the technology 25 years ago, some key patents expired in 2017, which opened up the company to competition. As soon as the patent expired, a stream of alternative offerings (especially DirectToConsumer), such as SmileDirectClub, AlignerCo and more, entered the market. Hence, I don’t consider Align’s hardware technology to be a significant source of sustainable competitive advantage. On the software and data front, however, Align’s IP of over 10 million patient scans from treatments make for a unique competitive advantage. The data set is leveraged to improve the success rate in complex malocclusion cases.

The brand has become synonymous with clear alignment treatments, offering a discreet and effective orthodontic solution. The first-mover advantage and its established B2B and B2C channels give Align the upper hand over competitors as the trusted brand in the space.

Financial profile and recent developments

As of Q2 2023, ALGN has always maintained a net cash position and currently has ~$1 billion in cash to deploy. The company also has an active $1 billion share buy-back program.

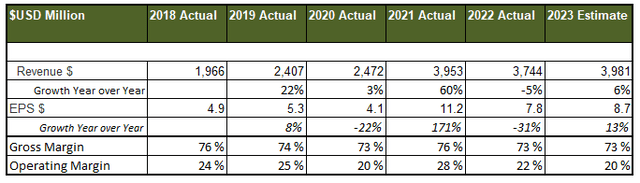

Align has achieved outstanding annual revenue and Earnings Per Share growth over the past ten years of 20% and 21%, respectively. The tailwinds outlined earlier should continue driving high growth rates going forward. Management guides for 20-30% revenue growth long term. Considering that the market is expected to grow ~15%, Align should be able to outpace that by 3-4% by capitalising on its decent competitive advantages. The company’s strategy has relied on strong organic growth by stealing market share from the traditional braces market.

In 2022, Align suffered a significant downfall in sales due to the pulled-forward demand during the COVID period. Evidently, Align’s profitability was impacted by the decline in volumes. The weakness in Align’s core US market coincided with lockdowns in China, magnifying the downside.

Growth and Margins (Company Reports and Guidance)

Valuation

ALGN rebounded from last year’s lows and is up 69% YTD. The majority of that can be attributed to investors regaining confidence in ALGN’s position, as the stock had a 50% re-rating YTD. In other words, FY1 P/E was up 50% to 40x. Over the same period, the S&P 500 Health Care sector was down 17%, and the S&P was up 16%.

Valuation multiples (Seeking Alpha)

ALGN has always traded at a premium to peers, considering its high-quality business model and the long-term demand tailwinds. Now, that premium is aligned with historical averages, and relative value is not particularly attractive.

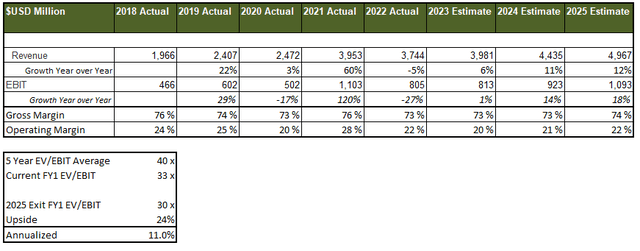

In my modelling assumptions, I factor in a modest recovery under what seems to be a tough macroeconomic condition across the world. In 2023, I modelled growth to be in line with management’s guidance, and in the following years, I expect the growth to gradually converge closer to historical averages due to improving macroeconomic conditions and the long-term tailwinds analyzed earlier. Management has several profitability-enhancing initiatives in place that should yield stability in the margin profile. I model for margin stabilization and gradual expansion.

Valuation Model (Company reports and Author’s projections)

Risks

Macro

Macro-economic exposure. Aligner treatments are largely out-of-pocket expenses, and insurance usually only covers a portion of the costs. The discretionary nature of demand exposes ALGN to cyclicality and macroeconomic conditions.

Competition

During the easy money era, competitors spawned from all over the world to challenge ALGN in various forms, including B2B and B2C. Now, many of them are falling apart, especially in the B2C market. However, well-respected players in the dental market have also launched clear aligners, and I expect those to have a negative impact on ALGN’s market share gradually.

Conclusion

Align Technology is a first mover in the fast-growing market of clear aligners. Both its leading market position and bulletproof balance sheet deserve a premium valuation to peers despite facing tougher competition. Following the recent multiple re-rating, Align’s risk-reward profile is modestly attractive under my modelling assumptions.

Read the full article here