Today, we put Alkermes plc (NASDAQ:ALKS) in the spotlight. The stock of this overseas drug concern got a nice little boost following better than expected quarterly results on Wednesday. Can the rally continue? An analysis follows below.

Seeking Alpha

This mid-cap, commercial stage biopharma concern is headquartered in Dublin, Ireland. Alkermes has several products already on the market. The stock currently trades around $28.00 a share and sports an approximate market capitalization of $4.6 billion.

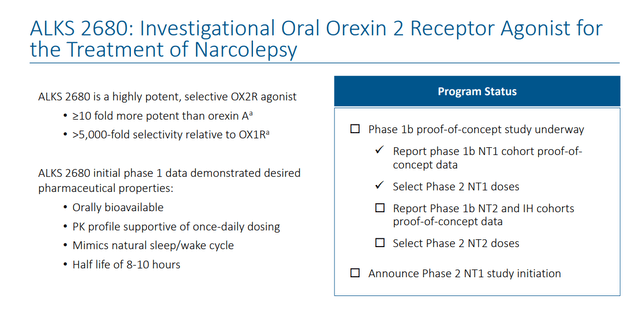

The company has an existing product portfolio including treatments for alcohol dependence, opioid dependence, schizophrenia and bipolar I disorder. The company also garners manufacturing and royalty revenue and has several candidates being developed within its pipeline. However, the only clinical stage candidate is a compound dubbed ALKS-2680, which should advance to Phase 2 development by year-end. Topline Phase 1b data was disclosed in April of this year. Therefore, Alkermes’ pipeline will not be germane to this analysis.

July 2024 Company Presentation

The company’s three bestselling, wholly owned drugs are:

VIVITROL – A treatment of alcohol and prevention of opioid dependence. As part of a patent litigation settlement, Alkermes granted Teva Pharmaceutical (TEVA) a license to manufacture/market a generic version of VIVITROL late in 2023.

ARISTADA – An intramuscular injectable suspension for the treatment of schizophrenia.

LYBALVI – An antipsychotic drug for the treatment of adults with schizophrenia and bipolar I disorder.

Alkermes also has licensed VULMERITY to drug giant Biogen (BIIB). VULMERITY is a novel oral fumarate for the treatment of relapsing forms of multiple sclerosis or MS. Alkermes manufactures this product (composition of matter patents run into 2033) and also receives a 15% royalty on net global sales.

Alkermes completed the spinoff of its oncology business ‘Mural Oncology (MURA)‘ in late 2023 to become a fully focused neuroscience concern. In late 2023, Alkermes announced it was selling its manufacturing facility in Ireland to drug giant Novo Nordisk (NVO) for a sum of $92.5 million. Alkermes will also retain all royalty revenues associated with products (INVEGA SUSTENNA®/XEPLION®, INVEGA TRINZA®/TREVICTA® and INVEGA HAFYERA®/BYANNLI) currently manufactured at the facility. Alkermes will continue to produce all its proprietary products at its manufacturing facility in Ohio.

Second Quarter Results:

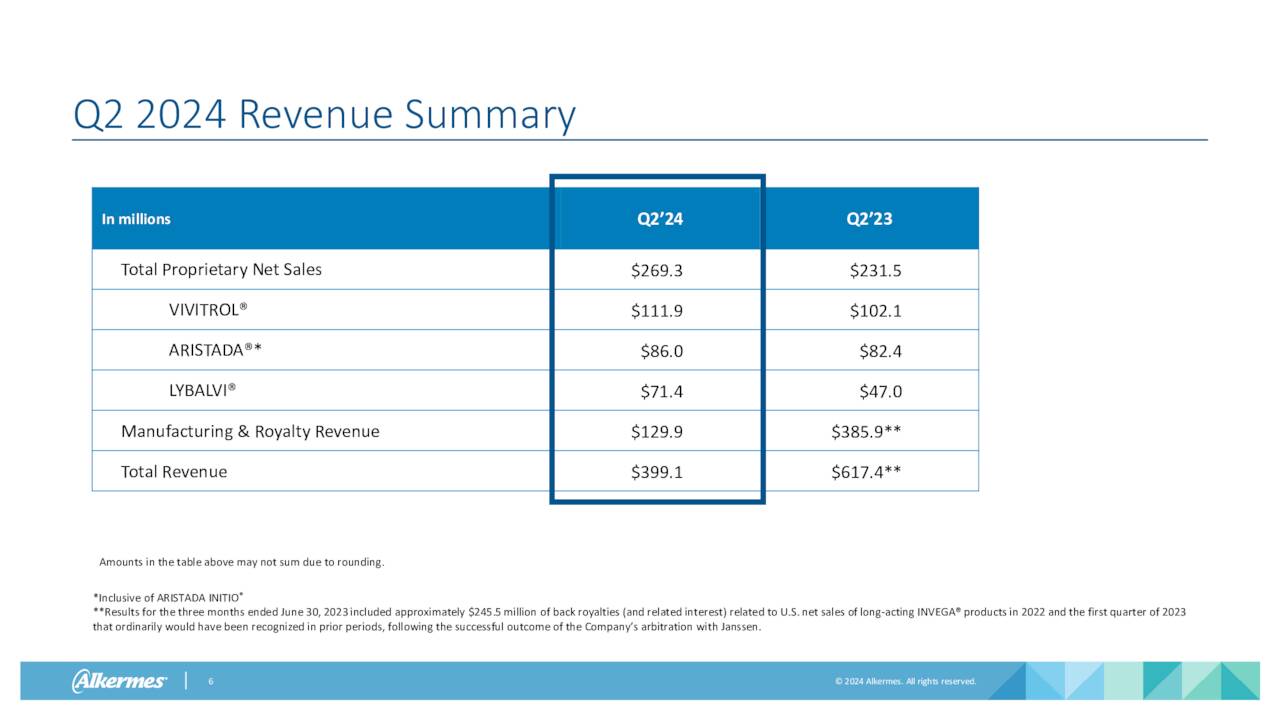

Alkermes plc posted its second quarter numbers on July 24th. The company posted non-GAAP earnings of 72 cents a share, a penny a share above the consensus.

Revenues fell just over 35% on a year-over-year basis to $399.1 million. However, sales were nearly $6 million north of expectations. The fall in revenues was strictly the result of a settlement with Janssen Pharmaceutica N.V. that resulted in back royalties of $245.5 million in the same period a year ago.

July 2024 Company Presentation

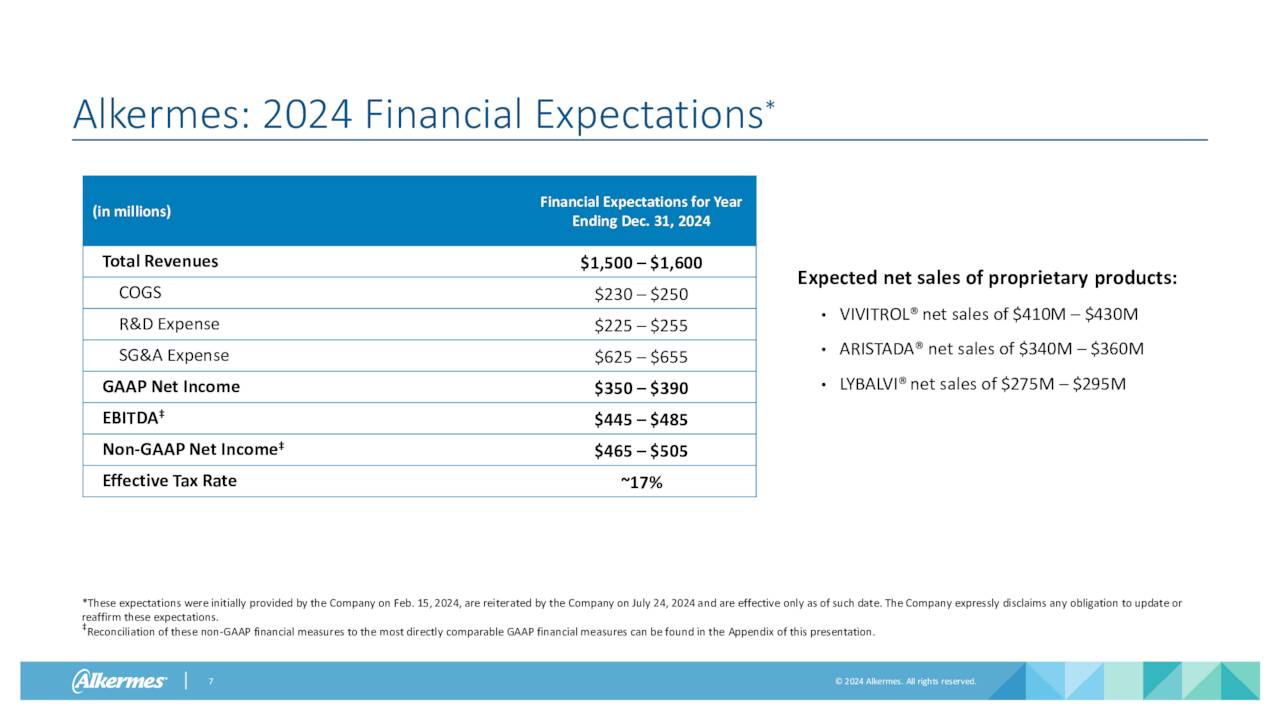

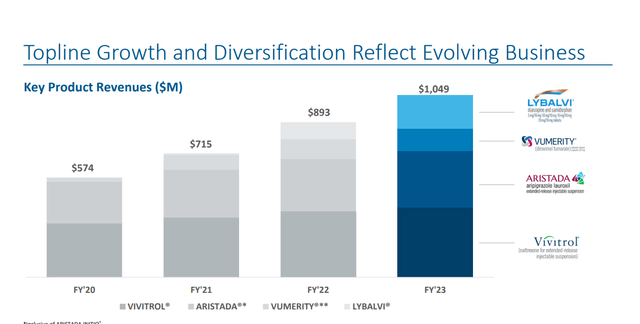

All three of Alkermes core products saw revenue growth in the second quarter on a year-over-year basis, led by a 52% increase in sales from LYBALVI which was approved mid-year 2021. Sales growth for ARISTADA and VIVITROL were much slower, as can be seen above. VUMERITY manufacturing and royalty revenues for the quarter came in $35.2 million. Other manufacturing and royalty revenues for several other compounds were $78.7 million for the quarter. Royalties and net sales of INVEGA SUSTENNA will end in approximately three weeks and should take a $20 million chunk out of Q3 revenues. Management also reaffirmed its FY2024 outlook (below) as well.

July 2024 Company Presentation

Analyst Commentary & Balance Sheet

The analyst community is currently mixed on their outlooks for Alkermes. Since Q2 results hit the wires on Wednesday, four analyst firms, including Goldman Sachs and TD Cowen, have reiterated Buy ratings on the stock. Price targets proffered range from $32 to $38 a share. Leerink Partners ($28 price target, down from $30 previously) and H.C. Wainwright ($37 price target, up from $35 previously) have maintained Hold ratings on the equity.

The company ended the second quarter with a tad over $960 million of cash and marketable securities on its balance sheet against approximate debt obligations of $290 million. The company’s cash balance rose just over $150 million during the quarter. Alkermes repurchased 3.5 million of its own shares in the quarter, spending nearly $85 million to do so. The company still has $315 million available on an existing stock repurchase authorization. Insider activity in the stock has been sparse so far in 2024. Three insiders via three transactions have sold just over $450,000 worth of shares collectively year to date. Approximately eight percent of the outstanding float in the shares is currently held short.

Conclusion

Alkermes plc made $1.44 a share on $1.66 billion in revenue in FY2023. The current analyst firm consensus is for profits to surge to $2.70 a share in FY2024, even as revenues fall to $1.51 billion. They project earnings of $2.62 a share in FY2025 on flat sales.

July 2024 Company Presentation

Even with this week’s gain in the shares, the stock is not expensive on an earnings valuation basis, as ALKS trades for under 11 times forward earnings. The challenge is overall sales growth is slowing substantially from recent years. Earnings for FY2025 are also projected to be slightly down.

Management has done a commendable job of streamlining the company in recent quarters and solely focusing Alkermes in neuroscience. Q2 results slightly exceeded expectations, and the stock has also benefited from the huge sector rotation the market has seen into small and mid-caps through the past couple of weeks. The 15% move up in the stock over the previous two weeks seems to have moved the stock to fully valued status in my opinion. Therefore, I am Neutral on the shares at these trading levels. If the stock saw profit taking and moved back down to the $25 level, I would probably establish an initial position in ALKS utilizing covered call orders at that time.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here