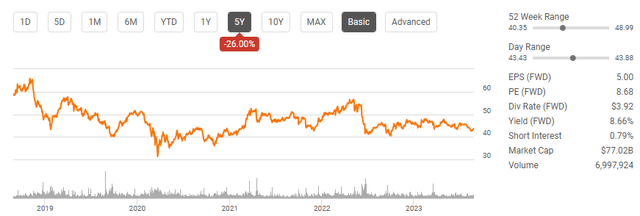

The Dividend Kings are a renowned group of companies that have consecutively increased their dividend payments for the last 50 years or longer. Of all the publicly traded companies, only 29 have earned the privilege of being referred to as a Dividend King. I consider Altria Group (NYSE:MO) the king of the Dividend Kings because it raised its quarterly dividend to shareholders by 4.3%, marking the 54th year of consecutive dividend increases, and as of the close on 8/25 MO has a dividend yield of 8.98% ($3.92 / $43.66). The only other Dividend King that has a yield exceeding 5% is 3M Company (MMM), with a dividend yield of 6.06% ($6 / $98.95). At the 2023 investor day conference, MO outlined its future dividend plan to 2028 and just delivered the first mid-single digit annual increase from its multi-year plan. MO is often looked at unfavorably due to its focus on tobacco products, but its earnings and ability to return capital to shareholders is undeniable. Shares of MO have declined by -26% over the past 5 years, and I am thrilled to acquire more shares of the Dividend King at depressed levels.

Seeking Alpha

Long live the king of dividends

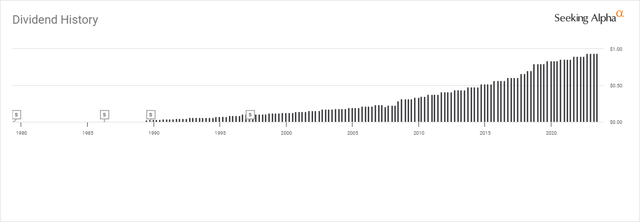

Going into 2023, MO had increased its dividend 57 times over the past 53 years. MO operates a profitable and financially predictable business, allowing them to allocate billions toward dividends and repurchase shares annually. For many investors, the dividend has become the focal point for MO as Mr. Market continues to underappreciate its earnings power and undervalue its shares.

MO may not have the longest run of increasing their dividend, but from an income perspective, I would rather invest in MO, generating an 8.98% yield with 54 consecutive increases, rather than investing in Dover (DOV), which has increased their dividend for 68 years and yields 1.41%. I tip my cap to every company that is part of the Dividend King club as it is one of the most impressive accomplishments for any business as it showcases the organization’s viability and ability to navigate difficult economic and business cycles. When I am investing for income, I prefer purchasing the combination of high-yield and dividend growth any chance I get.

Altria Group

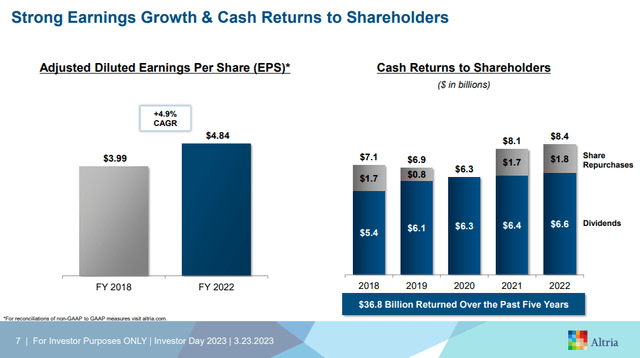

Since the end of 2018, MO has increased its dividend from $3.20 to $3.76 at a compound annual growth rate of 4.1%. The latest 4.3% increase took the annualized dividend from $3.76 to $3.92, which is in-line with their previous projections. Management established a new progressive dividend goal that targets a mid-single-digit increase on an annual basis as part of their 2028 enterprise goals. I had previously speculated that my definition of mid-single digit would be the 4-6% range, and it looks like management agrees. I believe MO won’t be dethroned as the king of Dividend Kings in my eyes because of how much the dividend is projected to increase. Below, we can see the tremendous growth MO has delivered to shareholders, and it’s not stopping any time soon.

Seeking Alpha

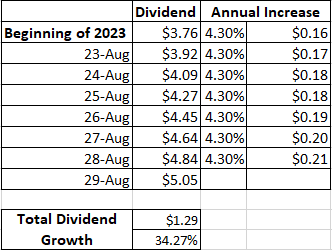

When MO says that mid-single-digit annual dividend growth is part of their 2028 Enterprise Plan, I will speculate that that means we will see this growth rate every year through 2028. When I plug a 4.3% annual growth rate in on an annual basis to match the recent increase, MO’s dividend will grow by $1.29 or 34.27% from the beginning of 2023 to the start of 2029. If you had purchased 100 shares of MO at the beginning of 2023, you would have spent $4,541, and if my projection becomes accurate and those shares are held, they would generate $29.97 of income over a 6-year period from 2023 through 2028. This doesn’t account for reinvesting the dividends and benefiting from the powers of compounding. This would be roughly 66% of the initial investment generated in dividends.

I don’t know what MO will do, but I feel it’s safe to assume that they will have no problem sticking to their projections, considering their history of 54 consecutive dividend increases. I am comfortable continuing to purchase shares as MO declines as I can dollar cost average into my position, benefit from annual dividend increases, and increase the number of shares I have every quarter by reinvesting the large dividends. From a dividend perspective, MO is my favorite Dividend King, and I think the market is undervaluing its shares significantly.

Steven Fiorillo

I think the market is wrong on Altria’s valuation and I see future value waiting to be unlocked

It doesn’t matter if you’re making widgets or semiconductors, $1 of revenue and $1 of earnings have the same value. The difference is the ability to scale and apply a growth factor to these numbers. When I look for baseline valuations to determine if a company is undervalued, I examine the price to free cash flow (FCF) it trades for and the forward P/E to understand how much I am paying for the company’s future earnings and if they’re expected to grow over time. I am going to compare MO to the following companies because they are also boring, non-tech companies with long histories of dividend increases. In fact, 4 of the 5 are Dividend Kings:

- 3M Company

- Philip Morris (PM)

- The Coca-Cola Company (KO)

- PepsiCo (PEP)

- Procter & Gamble (PG)

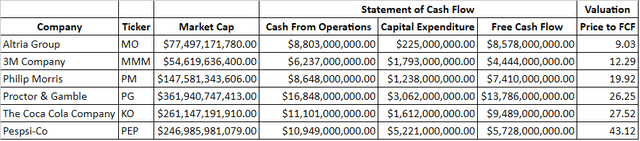

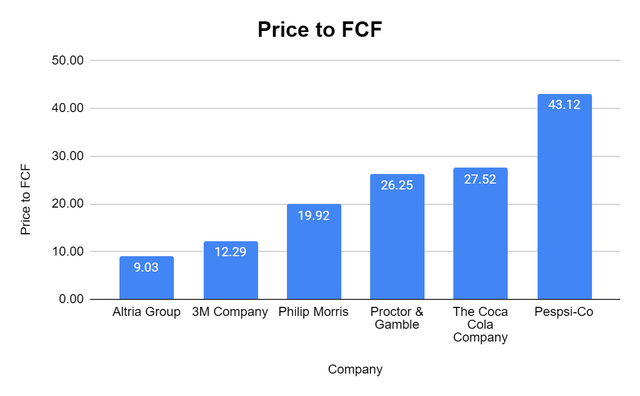

First, I will look at each company’s price to FCF. If you were to purchase a business privately, one of the first questions you would find an answer to would be how long until I make my money back. When I invest in public companies, I want to see how long they will take to generate their market cap from FCF. Generating an abundance of FCF increases a company’s ability to generate value for shareholders. When anyone invests in a company, they are paying the current value for the company’s future cash flow in terms of revenue and profitability, so it’s important to see what you’re paying for.

Steven Fiorillo, Seeking Alpha

In the trailing twelve months (TTM), MO has generated $8.58 billion in FCF. They are currently trading at 9.03x their TTM FCF, which is a low multiple. The most similar company to them is probably PM, and PM trades at 19.92x its FCF and generates -$1.17 billion less in FCF than MO over the TTM. This is a very wide gap, considering MO generates significantly more FCF than PM. When I look at other Dividend Kings, they are trading at larger multiples, MMM trades at 12.29x, then PG jumps to 26.25x. This is very interesting to me because when I look at MO from a profitability perspective and take the industry out of the equation, the multiple on its profits seems too low.

Steven Fiorillo, Seeking Alpha

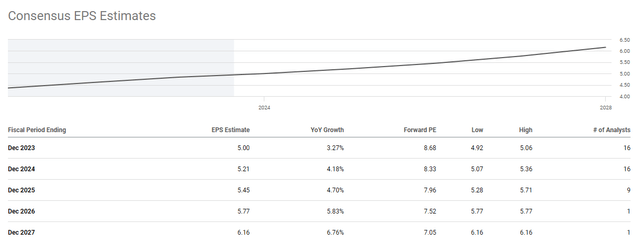

Next, I want to see what the analysts are projecting for the future EPS. I normally look out for several years to create a better picture for myself. All of the future consensus estimates I used can be found on Seeking Alpha by clicking on this link (Click Here).

Seeking Alpha

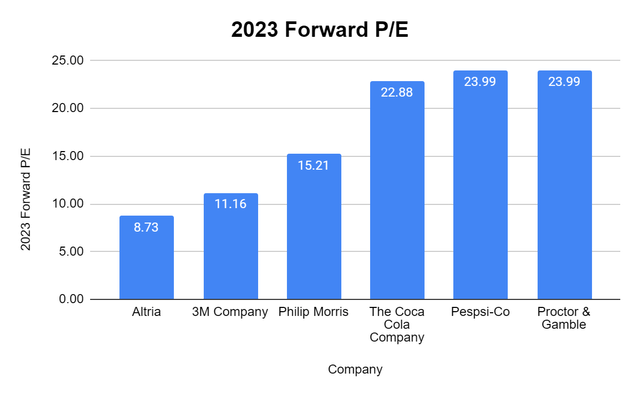

There are 16 analysts who have provided EPS projections for 2023 and 2024 for MO, and another 9 analysts have projected what they will generate in 2025. MO is expected to generate $5 of EPS in 2023, $5.21 in 2024, and $5.45 in 2025. MO trades at the lowest forward P/E ratios of the peer group in each of the following 3 years.

Steven Fiorillo, Seeking Alpha

Based on the current share price of $43.67, you would be paying 8.73x earnings for MO’s 2023 earnings. Going out to 2024 and 2025, you would be paying 8.38x and 8.01x MO’s future earnings. Over the next 2 fiscal years, MO is expected to grow its earnings by 9%, which is significantly lower than the others in the per group, but that is hardly a reason for the deep discount on the forward P/E multiples. MO is still growing its EPS, which is an indication of its ability to provide annualized dividend increases, which is one of the main focal points of the investment. PM has slightly more than double the estimated earnings growth, but you’re paying 15.21x 2023 earnings compared to 8.73x for MO. Mr. Market is valuing MO as if earnings are going to decline drastically, and that’s not the case. MO may not have the forward growth that some may want to see, but that’s not a reason for MO to have a high single-digit P/E looking out several years.

Steven Fiorillo, Seeking Alpha

Conclusion

MO is my favorite Dividend King, and I am adding to my position. MO just provided shareholders with their 54th consecutive year of dividend increases and is projecting that they will continue growing the dividend in the mid-single-digit range. After looking at the numbers, MO looks drastically undervalued, especially when compared to PM and other Dividend Kings. MO may not be the right investment for you, given its sector, and everyone should do their own research before investing. MO fits within my investment parameters, and I believe it’s one of the best income-producing equities for investors focused on producing income. I think that MO should trade in the $50-$60 range rather than the $40-$50 range, which currently presents an opportunity for capital appreciation and generating a large yield.

Read the full article here