Investment Thesis

The recent downturn has arguably exposed that AMD (NASDAQ:AMD) is far past its stage of high growth. Other data further confirms that AMD is stalling, and at this point should hence be seen as merely an alternative Intel (INTC), not as a growth stock that will deliver strong alpha. Nevertheless, the company still sports a high valuation, which further makes the stock (even) less compelling.

Background

I have covered AMD twice previously this year.

In February, I warned investors that the growth story was finally finished: Advanced Micro Devices: Growth Story Finished (AMD). While the stock has perhaps held up reasonably compared to the sell rating at the time, arguably there is no reason the stock couldn’t indeed have declined as investors could have decided to rate AMD with a lower multiple given the lowered growth outlook.

In May, I dived a bit deeper into the product and competitiveness outlook trends: AMD Stock: Data Center Doom Scenario Unfolding (AMD). AMD will face a more competitive environment than in the last several years going forward, increasing risk.

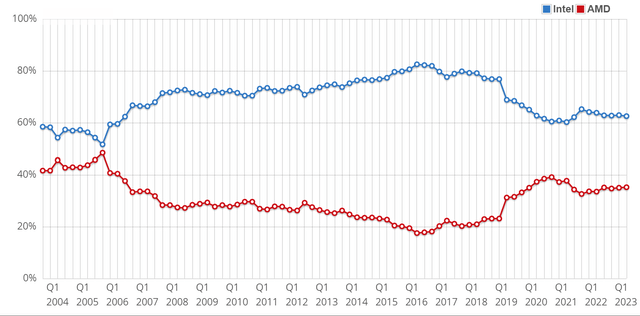

Market share trends

The latest information suggests that AMD’s market share gains have been stalling for a few years now after the rapid growth in 2019-2020. This data is among all CPUs. The source further details the distinct trends in laptop, desktop and server.

PassMark

Note that this data is created based on CPUs running the PassMark CPU benchmark, and should therefore at best be considered an approximate overview of the underlying market share trends. For example, a CPU that was bought years ago running this benchmark would count toward the CPU’s vendor’s market share. Especially in the server segment, the PassMark data would suggest that Intel’s market share has been stable for the last three years, which even Intel isn’t arguing.

Nevertheless, the data does more or less align with other signals, such as Intel claiming that it has regained PC market share for a few quarters now, and that its data center share is perhaps doing a little better than expected. This is also visible in the company’s financials, which showed how AMD’s PC revenue halved in Q3’21, a far larger decline than Intel’s.

Technology trends

These results also align with the technology evolution. Intel regained strong competitiveness in late 2021 with Alder Lake, and Sapphire Rapids is starting to do the same on the server side, with further improvements slated next year with Granite Rapids and Sierra Forest.

Overall, for AMD this increased competitiveness from Intel means that there are simply no obvious opportunities for (further) market share growth. AMD had grown significantly over the last several years, but this thesis has played out, with no compelling new thesis replacing it.

Q2 results

From Seeking Alpha coverage:

Revenues fell 18% to $5.36B, but were expected to do worse, and gross profit slipped 19% to $2.44B, though gross margin remained flat at 46%.

Despite AMD’s rosy projections for a strong double-digit CAGR, the reality is that the company hasn’t been immune to the downturn. Also note that the gross margin hasn’t improved much (further) over the last few years, indicating that AMD is still for a large part operating as a value offering/brand.

While the PC segment was responsible for most of the decline, even the data center segment declined by 11%.

AMD expects sequential growth to $5.7B at the midpoint for Q3, but since Intel is also expecting further sequential growth, this aligns with the thesis that AMD has become some sort of second or alternative Intel. Also similarly to Intel, AMD touted the growth in its AI pipeline. However, both Intel and AMD’s pipelines are minuscule compared to Nvidia’s (NVDA) actual revenue.

Valuation

Without any obvious growth catalysts on the horizon, as stated the thesis for AMD in that regard would be at best as an alternative to Intel. However, this is not a strong thesis, as the valuation is simply not in its favor.

AMD trades for 40x 2023 EPS estimates and over 25x 2024 estimates. While the semiconductor market is (despite some of its cyclicality) generally seen as a growing one, which means AMD should still enjoy some reasonable growth that could lift the stock over time, there is simply little compelling in this valuation given that the investment thesis isn’t very compelling to start with.

Investor Takeaway

Depending on how much credence one lends to the 2024 estimates, the 2023 estimates show that AMD trades for an above average to high valuation. In spite of this, there is arguably little to support such a premium valuation, and hence to justify an investment.

With eroding technology leadership that is already causing a stalled market share trend, AMD is simply acting as an alternative Intel at this point: one without fabs and therefore also a lower potential gross margin. This is further supported by the fact that the data center segment has quickly decelerated from triple digit growth to a double digit decline in the recent quarter.

Although it is certainly not unlikely that the downturn will make way for an upturn, a lot of that is already priced into the stock. As such, investors might have to wait quite some time for what may ultimately end up as mediocre alpha in the stock.

Overall, the financials and market share trends over the last two quarters have reinforced my hold rating, very slightly weighing towards a sell as the valuation remains stretched. Note that from the start Intel’s turnaround was only expected to show material progress from 2024 onwards, so the lackluster performance AMD has displayed in recent quarters bodes little optimism for when the marketplace really starts to heat up in the next year.

Read the full article here