Thesis

Amdocs Limited (NASDAQ:DOX) is an undervalued dividend-growth company. This BBB investment-grade company has a low long-term debt-to-capital of just 17.57%. It is expected to post an average high single-digit adjusted operating earnings growth rate of 9.32% this year, and 9.58% for the next 2-3 years. Add to that the 2.31% dividend yield that has been growing at an average of 11.91% a year for the past 5 years (a slight dip compared to the 12.59% dividend growth rate for the past 10 years), and DOX should easily provide returns above 10% a year.

Business Overview

According to form 20F,

Amdocs is a leading provider of software and services for approximately 400 communications, entertainment and media industry and other service providers in developed countries and emerging markets. We believe the demand for our solutions is driven by our customers’ continued migration to the cloud, deployment of 5G networks and transformation into digital service providers to provide connectivity services, content and applications on any device through digital and non-digital channels…

Service providers are increasingly focusing on their core capabilities and investing in 5G and fiber rollouts to meet the demand for increased bandwidth, faster pace of innovation for new digital services and the introduction of GenAI, as well as to improve their business and operational agility and optimize and monetize their investments in such services…

We develop, implement and manage software and services designed to meet our customers’ business needs and empower them to transform their boldest ideas into reality. Our technology, design-led thinking approach and expertise help service providers to migrate to the cloud, manage and monetize their next-generation networks, further transform into digital service providers, accelerate their GenAI journeys, enhance their entertainment offerings, and serve their customers across all channels.

Amdocs focus on telecommunication customers, including some of the largest telecommunications companies in the world like America Movil, AT&T, Bell Canada, Singtel, Telefonica, Telstra, T-Mobile, Verizon and Vodafone. Amdocs’ customers also include broadband, mobile and entertainment service providers Altice USA, Charter, Comcast, DISH, J:COM, Rogers Communications and Sky.

The main revenue driver is “Managed Services” which

“provide multi-year, flexible and tailored support, managing IT, business processes and applications services, such as application development and maintenance, operations, IT and infrastructure hosting, cloud operations and in-house developed practices, and legacy modernization.”

In 2023, Managed Services generated 58% of its annual revenue.

2023 20F Page F-37

What I Like About The Company

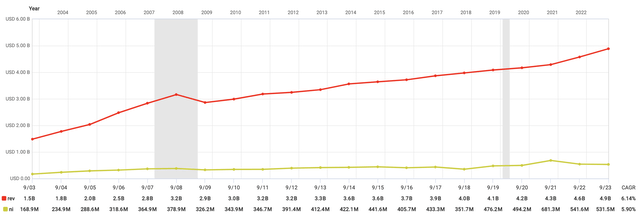

1. This is A Growing and Resilient Business

Both revenue and net income have been growing steadily since 2001.

Fastgraph

This is a business that continued to generate revenue and net income through the Great Financial Crisis, dropping just $0.05 per share in 2008, from $2.14 to $2.09 per share in adjusted operating income. This is a business that grew revenue and net income through the COVID-19 pandemic.

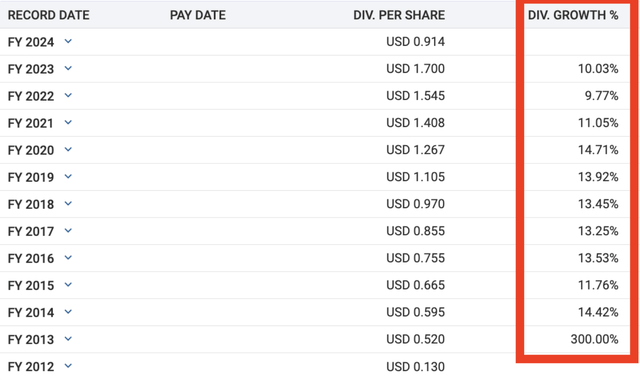

2. This Is A Dividend Growth Compounder

Since this business started paying dividends in September 2012, it has continued to grow that dividend at an average rate of 12.59% (excluding the huge jump from $0.13 per share in 2012 to $0.52 per share in 2013), and the total of dividends paid out has more than 9x from $22 million in 2012 to $201 million in 2023. With the payout ratio at just 28.8%, maintaining that average dividend growth rate of between 10% to 12% is definitely safe.

Fastgraph

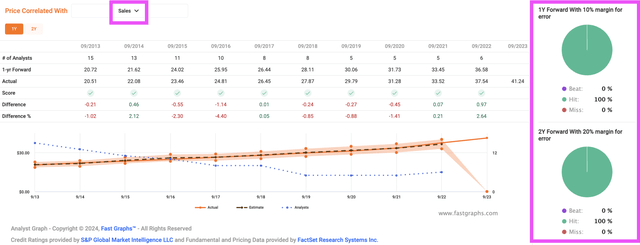

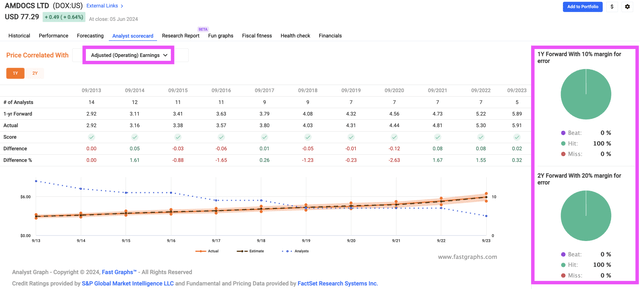

3. Predictable Revenue

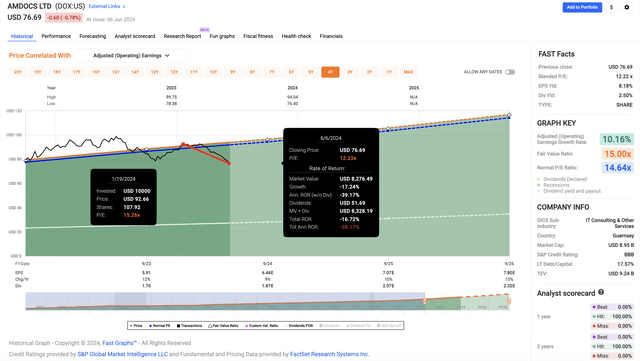

DOX’s revenue is usually very predictable and consistent. The contracts customers sign contracts with DOX are often multiple-year ones, like the recently signed a 5-year deal with AT&T and with Charter Communications that will last till 2029. Service disruptions are a no-no for these huge companies, and once they sign with DOX, it will take a lot to change to a different service provider.

Coupling the predictable revenue and adjusted operating earnings with clear guidance from the management, FactSet analysts have been able to forecast DOX’s 1-year and 2-year revenue and adjusted operating earnings correctly 100% of the time (i.e., with less than 5% margin of error).

Fastgraph DOX Sales’ Predictability Fastgraph DOX Earnings’ Predictability

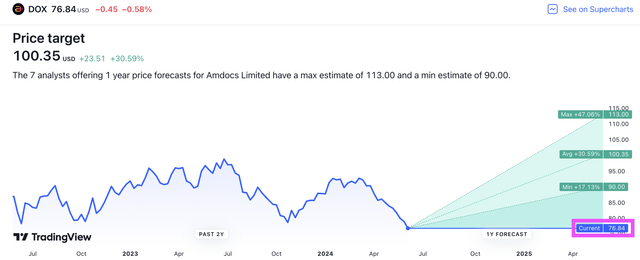

4. Analysts’ Bullish Take On DOX

Analysts are generally bullish on DOX. DOX’s current price is far below analysts’ price targets, both the lowest one-year price target of $90 and the consensus price target of $100.35.

TradingView

It is not difficult to see why. According to Gartner’s research,

IT services will continue to see an increase in growth in 2024, becoming the largest segment of IT spending for the first time. Spending on IT services is expected to grow 8.7% in 2024, reaching $1.5 trillion… This is largely due to enterprises investing in organizational efficiency and optimization projects. These investments will be crucial during this period of economic uncertainty.

Barclays recently upgraded DOX to “Overweight,” raising the price target from $100 to $115.

5. Strong Balance Sheet

DOX is a BBB credit rated company that has a low long-term debt-to-capital of just 17.57%. It generated $823 million in operating cash flow in 2023 and has $544M in cash and cash equivalents as of the latest quarter. The $803 million in total debt is of no concern in my opinion.

Why Did The Stock Price Taken A Hit in 2024?

2024 has been a great year so far for the S&P 500 (SPY), which has gained around 12%. It has been terrible for DOX, though, which has fallen 17% year-to-date.

Fastgraph

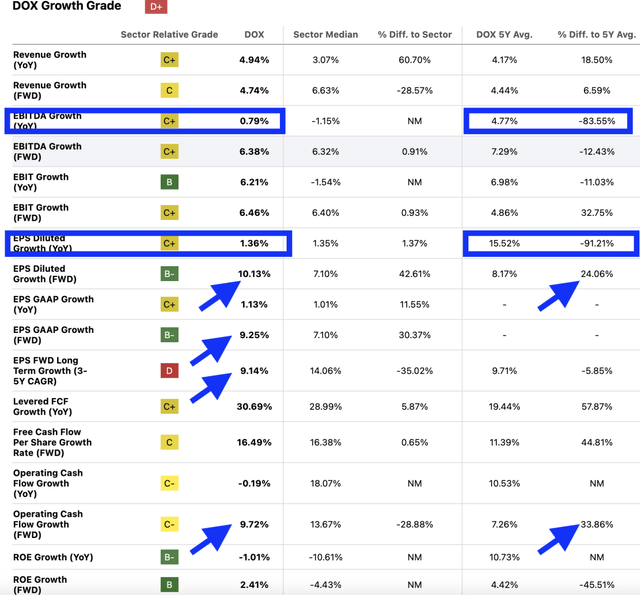

Two reasons.

One, DOX’s growth rates year-on-year growth rates has declined. EBITDA “grew” by just 0.79%, an 83% decline for the company to its 5-year average. Diluted EPS year-on-year growth of just 1.36% is also much lower than its 5-year average growth rate of 15.52%.

Seeking Alpha

Management is still expecting high single-digit to low double-digit growth in 2024 and in the next few years, and these expected growth rates are higher than the past 5-year average growth rates.

However, investors might wonder if DOX can pull off those expected growth rates, so when management lowered their guidance for 2024, that hit investors’ confidence hard. This would be the second reason.

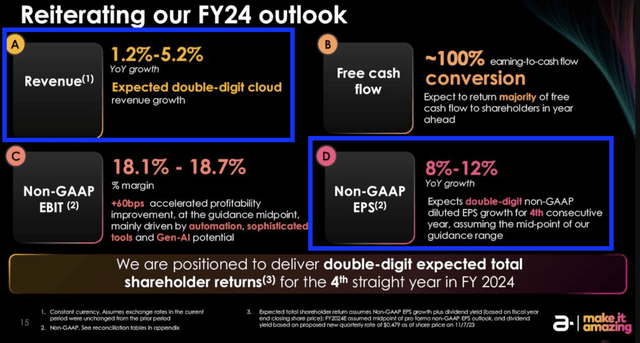

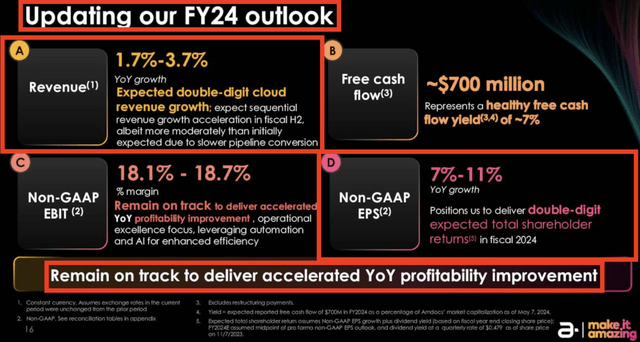

The following slide was taken from DOX’s Q1 2024 earnings presentation slide.

DOX Q1 Earnings Presentation Slides

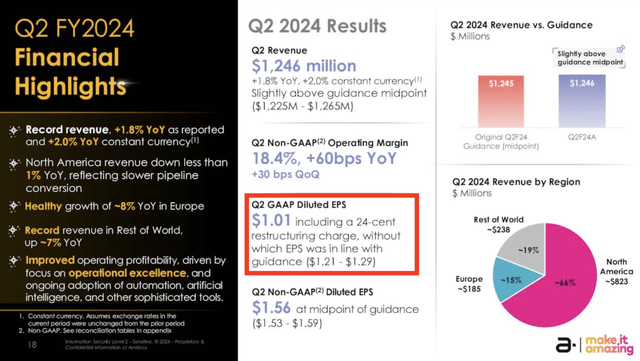

Compare that to the next slide below, taken from DOX’s Q2 2024 earnings presentation slide.

DOX Q2 2024 Earnings Presentation Slide

Comparing the two slides, the following differences stood out.

- Management’s guidance for y-o-y revenue growth was revised from 1.2%-5.2% to a narrower 1.7% to 3.7%. Although the low end of the estimate was raised by 0.5%, the top end of the previous estimate fell by 1.5%.

- Non-GAAP EPS y-o-y growth was revised down from 8%-12% to 7%-11%.

- The exuberant “double-digit expected total shareholder returns” was toned down to become “deliver accelerated yoy profitability improvement.” Does that mean management does not expect “double-digit shareholder returns” for FY 2024??

Furthermore, there was a decrease in the diluted earnings per share. Although that is a non-recurring hit due to restructuring costs, it still stings.

DOX Q2 2024 Earnings Presentation Slide

Compelling Valuation

Analysts’ gave price targets ranged from $90 to $113, but by themselves, price targets are not indicative of a stock’s fair value.

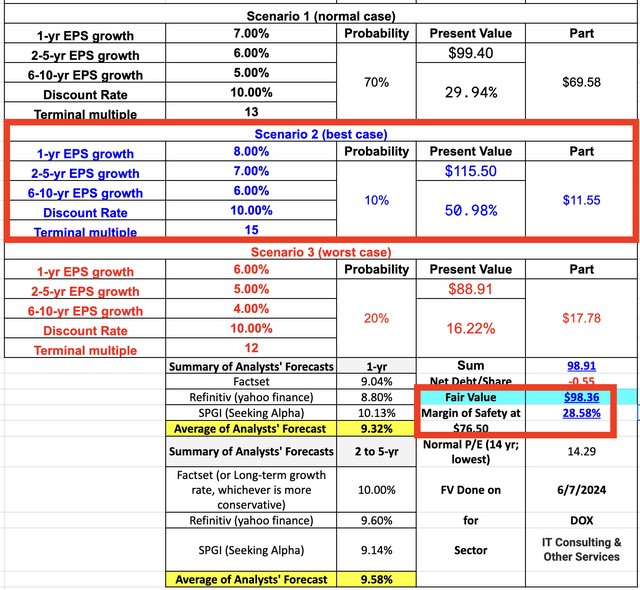

Analysts have been 100% right about DOX’s sales and adjusted operating earnings projections, and the projected growth is 9.32% for this year and 9.58% for the next three years. To build in a greater margin of safety in my valuation, I assume a discount rate of 10% (4.285% risk-free rate + 6.4275% risk premium), a 70% chance (instead of 100%) that DOX will meet the low end of its non-GAAP EPS growth of 7%, a 10% probability that DOX could grow EPS by 8% (when the high end of the guidance is 11%), and a 20% likelihood that DOX’s growth goes lower than the 7% that management guided, despite management expressing confidence in the Q2 2024 conference call that growth will pick up in the second half of 2024, my own valuation of DOX ranges from a low of $88.91 in my bear case to a high of $115.50 in the bull case.

Author’s Take on DOX’s Fair Value

Even in my bear case, DOX’s valuation is still higher than the price it is trading at the time of writing this article. I believe that buying DOX at around $76.5 offers investors a 28.5% margin of safety.

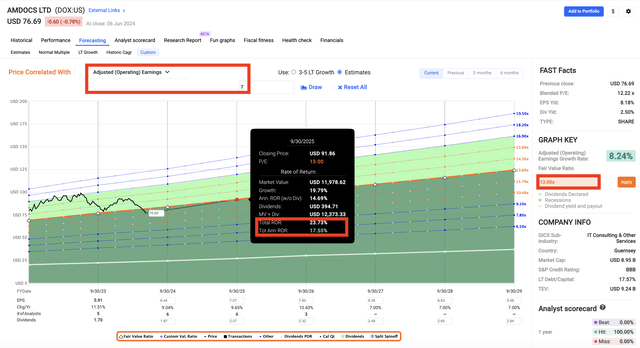

Hypothetically, at an EPS growth rate of 7% for 2024 and 2025, and an earnings multiple of just 13, DOX offers the potential to provide a 17.55% in total annualized rate of return by the end of 2025.

Fastgraph

What I Do Not Like

There was a short seller report written about DOX in 2021, accusing management of fudging the numbers, among other things. Management responded in 2021,

The report contains inaccurate statements, groundless claims and speculation that were designed to drive the stock price downwards to serve the short seller’s interests to the detriment of Amdocs shareholders.

Having owned stocks that were the target of short reports (e.g., Medical Properties Trust (MPW)), I know full well the damage such reports can cause.

To date, I could not find further developments in this matter, and as far as I can tell, the reasons for the stock price decline in 2024 were not related to the contents of this report. However, if the matter has not resolved, the accusations raised in that report may continue to cast doubts in the minds of investors.

Conclusion

Like I said at the start, I like Amdocs Limited for many reasons. It is an undervalued dividend-growth company. This BBB investment-grade company has a low long-term debt-to-capital of just 17.57%. It is expected to post an average high single-digit adjusted operating earnings growth rate of 9.32% this year, and 9.58% for the next 2-3 years. Add to that the 2.31% dividend yield that has been growing at an average of 11.91% a year for the past 5 years (a slight dip compared to the 12.59% dividend growth rate for the past 10 years), and DOX can easily provide returns above 10% a year.

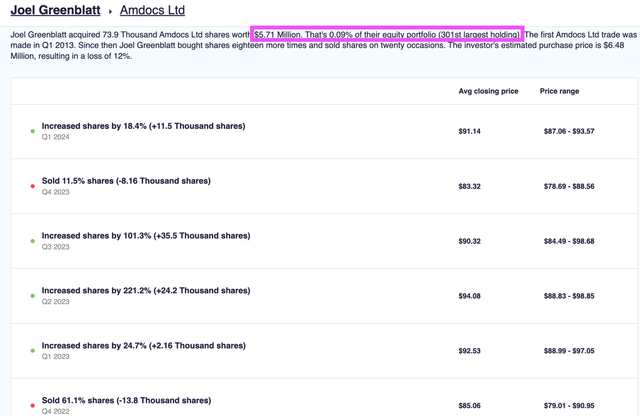

It also does not hurt to know that famed value investor Joel Greenblatt agrees. In Q1 2024, he just increased his position in DOC by 18.4%. His average purchase price has been above $91, so to be able to buy in at $76.50 is a steal in my book.

Stockcircle

Read the full article here