Investment Thesis

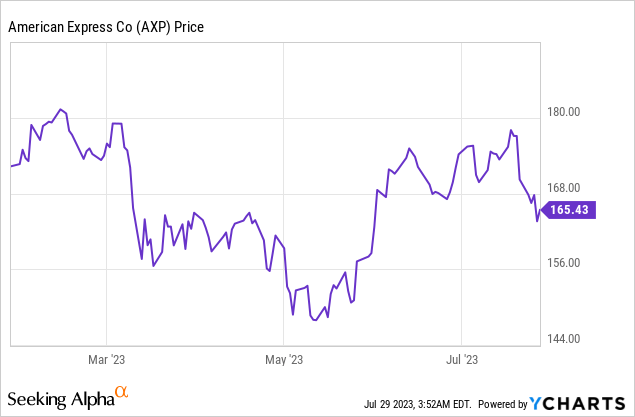

American Express’s (NYSE:AXP) share price has declined around 8% since my previous coverage in February, as the company was partially impacted by the fear of the SVB bank failure. I continue to believe the company presents a compelling investment opportunity for investors.

The latest earnings remain very solid with both the top and the bottom line growing by double-digits, as the company benefited from higher interest rates and strong consumer engagement. The broad economy is also holding up much better than expected, which should provide further support for spending. The strong backdrop alongside the discounted valuation should translate to solid upside potential moving forward.

Solid Q2 Earnings

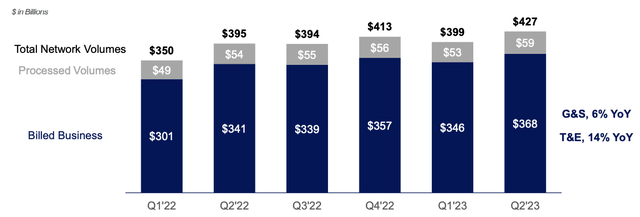

American Express released its second-quarter earnings earlier this month and the results continue to be very solid. The company reported revenue (net of interest expense) of $15.1 billion, up 12% YoY (year over year) compared to $13.4 billion. The growth was mostly driven by higher interest income and strong consumer momentum. Interest generated from loans increased 56% from $2.71 billion to $4.21 billion, as the interest rate shot up during the year.

On the non-interest side, net card fees grew 21% from $1.48 billion to $1.79 billion, as the company acquired 3 million new cards during the quarter. Discount revenue (merchant fees) increased 7% from $7.87 billion to $8.48 billion, as consumer spending remained upbeat. Travel & entertainment continue to see strong traction, with volume up 14% YoY.

American Express

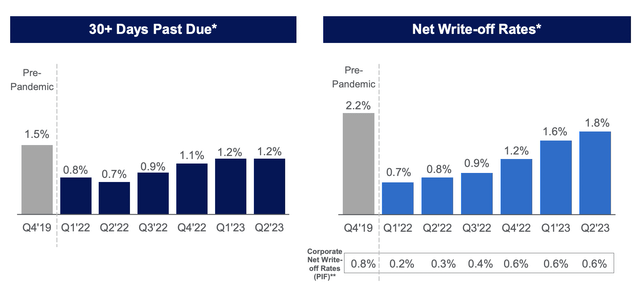

The bottom line was largely in line with the top line. The most notable segment was the provisions for credit losses, which nearly tripled from $410 million to $1.2 billion due to higher interest rates. The jump looks alarming but I am not too concerned right now. For context, while the latest net write-off rate of 1.8% is significantly higher than 0.8% in the prior year, the figure is still below the pre-pandemic level of 2.2%. The delinquency rate of 1.2 is also below the pre-pandemic level of 1.5%, as shown in the chart below.

The company continues to manage its operating expenses well. Expenses as a percentage of revenue declined 410 basis points from 77.6% to 73.5%. The increase in write-offs was offset by the drop in expenses, resulting in the net income up 11% YoY from $1.93 billion to $2.14 billion. The net income margin dipped 20 basis points from 14.4% to 14.2%. The diluted EPS was $2.89 compared to $2.57, up 12% as it benefited from a lower share count. The company also reaffirmed its full-year guidance and continues to expect revenue and EPS growth of 16% and 13% at the midpoint, respectively.

American Express

Resilient Economy

Despite the increasing interest rates and the shrinking balance sheet, the US economy has been holding up much better than most expected. Other than certain rate-sensitive sectors such as commercial real estate, the overall economy remains pretty solid. The strength is particularly evident on the consumer side, as excessive savings from the pandemic stimulus and the low unemployment rate provided a strong financial buffer.

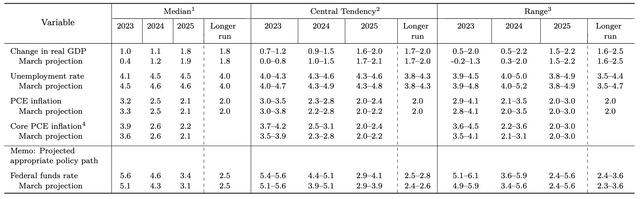

Amid the strong momentum, the Federal Reserve recently revised its 2023 median real GDP forecasts from 0.4% in March to 1% in June. The unemployment rate was also downward revised from 4.5% to 4.1%, as shown in the chart below (these projections are released every other meeting therefore no forecasts were given in the FOMC meeting last week).

The resilient economy will likely translate to a longer period of elevated interest rates, but the impact on American Express should be relatively neutral, or even positive. While this may continue to put pressure on the delinquency rate, the increase in interest income should be able to offset the increase in write-offs, as shown in the latest earnings. I believe this backdrop should continue to favor consumer spending, which benefits the company meaningfully.

Stephen Squeri, CEO, on spending trend

Card Member spending hit another all-time high in the quarter, with U.S. consumers and card members outside the U.S., both up by double-digits, which offset some softness in U.S. small businesses. Millennial and Gen Z consumers continue to be the fastest-growing portion of our card member base with U.S. billings up 21% in the quarter.

Federal Reserve

Discounted Valuation

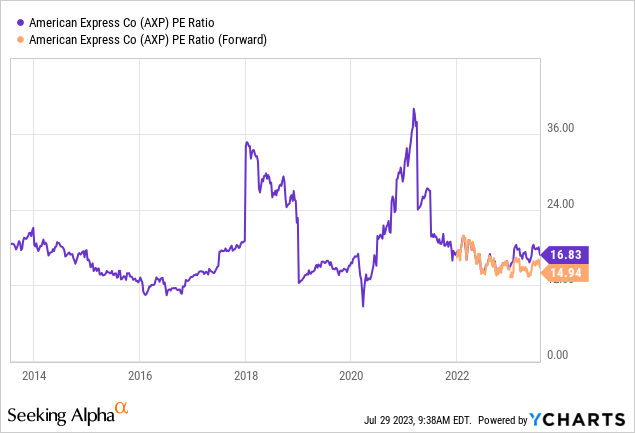

While many companies’ valuations have become very elevated amid the market rally, American Express is a rare quality company still priced at a discount. The company is currently trading at a PE ratio of 16.8x, which is quite cheap on a historical basis. As shown in the first chart below, the multiple is currently near the bottom of its historical range, representing a solid discount of 13% compared to its 5-year average PE ratio of 19.3x.

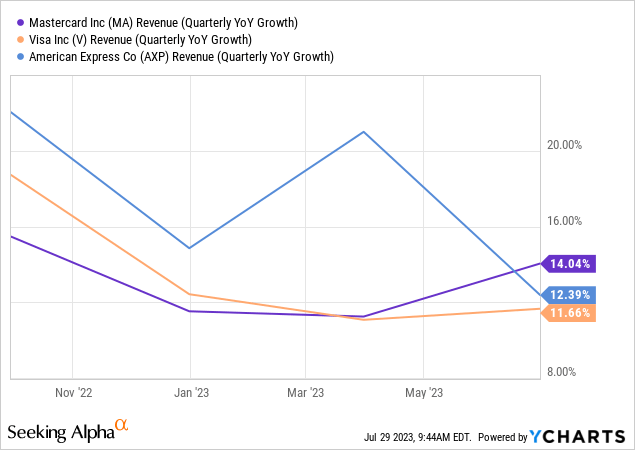

As mentioned in the previous article, the company is also trading at a steep discount compared to credit card peers Mastercard (MA) and Visa (V). I continue to find the massive valuation gap exaggerated as the three companies are actually growing revenue at a similar pace, as shown in the second chart below. American Express deserves a small discount due to its credit exposure, but I also think its valuation should be closer to peers.

Investor Takeaway

American Express’s latest earnings were once again very solid. The rise in interest rates significantly boosted interest income and the non-interest side continues to see strong card acquisitions and travel & entertainment spending. The latest developments in the economy also seem to favor the company, as consumers remain resilient while higher interest rates benefit interest income.

An economic downturn or recession is a potential risk, but the current trend remains healthy, and the company’s affluent customer base should also provide better resilience compared to peers. The company’s valuation continues to be discounted and I believe the huge valuation gap presents attractive rerating potential that could translate to ample upside. Therefore, I reiterate my buy rating on American Express stock.

Read the full article here