Investment thesis

American Financial Group, Inc. (NYSE:AFG) is a successful property and casualty insurance company. And there are two ways in which you can invest.

You can buy its debentures, such as AFGC (NYSE:AFGC), with a face yield of 5.125% and a current yield of 6.17%. I believe it is a security that allows you to sleep at night because there is little risk in my opinion.

After comparing AFG stock with its dividends and the debentures, I conclude that AFGC debentures make more sense for income investors.

About American Financial Group

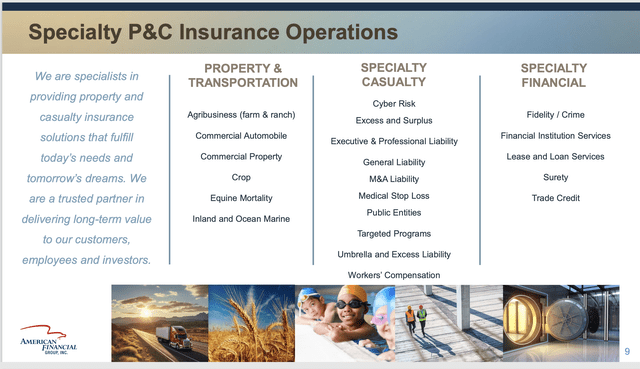

According to the firm’s website, its insurance origins go back to 1872, while it has been in its current form since 1959. It is a property and casualty, or P&C, company that focuses on “specialized commercial products for businesses”, or what’s known as niche markets.

It is a holding company for 35 specialized businesses, grouped into three segments:

- Property and transportation

- Specialty Casualty

- Specialty Financial

This slide from the May 14, 2024, Wells Fargo Financial Services Investor Conference provides more detail about the lines of business followed by companies in each of the segments:

AFG Segments information (AFG investor presentation)

AFG announced its Q1-2024 results on May 1, and the highlights included:

- Net earned premiums totaled $1.546 billion, compared with $1.437 billion in Q1-2023.

- Core net operating earnings were $231 million, down from $2.47 million last year. The company attributes the setback to lower returns from its alternative investment portfolio.

- Net earnings were $2.42 million, or $2.89 per share, compared to $2.12 million or $2.49 per share in the same quarter last year.

Combined ratios, which are calculated by dividing losses and expenses by earned premiums, were strong for all three segments in Q1:

- Property & Transportation: 89.0% versus 91.0% last year.

- Specialty Casualty: 89.8% compared to 87.5% last year.

- Specialty Financial: 86.3% versus 86.5% last year.

Any ratio below 100% indicates an insurance company is profitable, and anything less than 90% is considered very good. American Financial, therefore beats the latter standard.

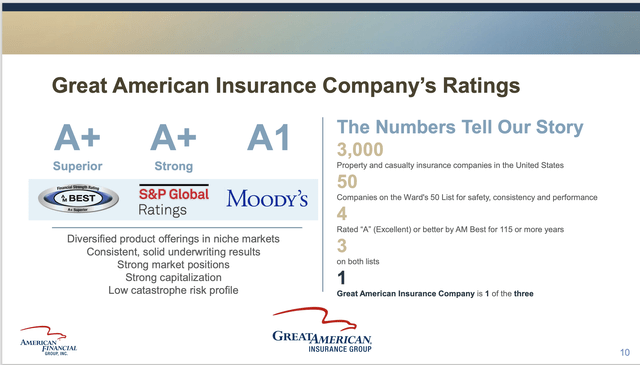

The strength of insurance companies is also measured by three major ratings agencies. This slide from the presentation lays out American Financial’s excellent results:

AFG Ratings slide (Investor presentation)

Results for the most recent quarter underline the strength and stability of American Financial, which should assure debenture buyers.

American Financial’s debentures

Insurance firms issue debentures to raise long-term capital without diluting their ownership. They are a form of bond that pay buyers a modest, but competitive interest rate. The companies then go on to invest or use those funds at (hopefully) higher rates and profit on the margin.

American Financial has issued four sets of so-called baby bond debentures:

- 5.875% Subordinated Debentures due March 30, 2059 (AFGB)

- 5.125% Subordinated Debentures due December 15, 2059 (AFGC)

- 5.625% Subordinated Debentures due June 1, 2060 (AFGD)

- 4.50% Subordinated Debentures due September 15, 2060 (AFGE)

Note that each of these debentures has an expiry date in 2059 or 2060, which are decades away. They were issued in 2019 and 2020 and had maturity dates 40 years ahead.

Baby bonds are issued like stocks and trade on public markets like stocks, so buying them is not like buying conventional bonds.

Thus, share prices in these debentures go up and down like common shares. When the price goes up, the yield goes down and when the price goes down, the yield goes up.

When I first analyzed these securities in early January of this year, the share price was $22.16 and it yielded 5.77%. Since then, the price has come down, $20.90 on Tuesday, June 4 and the yield has risen to 6.17%.

That’s 39.90% higher than the current 10-year Treasury rate of 4.41%. A significant premium, if I can use that word, for little additional risk.

I say “little additional risk” because the company is growing and very profitable. As Co-CEOs S. Craig Lindner and Carl H. Lindner III noted in the Q1 earnings release, “AFG continued to have significant excess capital at March 31, 2024. Returning capital to shareholders in the form of regular and special cash dividends and through opportunistic share repurchases is an important and effective component of our capital management strategy.”

The current interest rate set by the Federal Reserve Board is in a range between 5.25% and 5.50%.

There is a risk factor that potential investors should recognize. The company could redeem the debentures before maturity. As I pointed out in the earlier article, one of the reasons for the current batch of baby bonds was to redeem 6.25% debentures that expire in 2054.

The greater the difference between the 2019-2020 bond rates and current interest rates, the more incentive American Financial has to replace them with new securities at lower yields.

To some extent, that risk is mitigated for purchasers of AFGC because the AFGB debentures pay 5.875% and the AFGD debentures pay 5.625%. The company is more likely to redeem them before AFGC, since its face yield is lower.

In that case, why not buy the higher-yielding debentures. You could, but their prices are above those of AFGC, offsetting the higher yields:

- AFGB: $23.55

- AFGC: $20.90

- AFGD: $22.96

As might be expected in an efficient market, there is no free lunch here.

Since the debenture is anchored to the pre-set yield, rather than earnings, we shouldn’t expect anything much in the way of capital gains or losses. That’s backed up by a five-year price chart:

AFGC Price Chart (Seeking Alpha )

American Financial’s Dividends

Very few companies can afford to pay special dividends, and American Financial stands out among those that do:

- 2019: two special dividends worth $3.30

- 2020: one special worth $2.00

- 2021: five specials worth $26.00

- 2022: three specials worth $12.00

- 2023: two specials worth $5.50

So far in 2024, it has paid one special dividend worth $2.50. The company also pays a regular dividend, which grew from $1.65 in 2019 to $2.60 in 2023.

American Financial has paid a dividend every year for the past 25 years, which is more than twice as long as the Financials’ sector median. In addition, it has 18 years of consecutive increases, which is far longer than the sector median of 2.1 years.

The 18-year streak of increasing dividends puts the firm on track to become a dividend aristocrat in another seven years. That’s a theoretical club for corporations; currently, there are only 67 out of more than 6,000 American stocks. The payment of dividends, especially those that increase every year, implies that a company is well managed. If we add special dividends to the mix, we might say excellently managed and highly profitable.

The regular dividend delivered a 2.21% yield at the close on Tuesday, June 4, when the price was $127.94. The average five-year growth rate is 12.23% and the payout ratio is a reasonably low 26.46%.

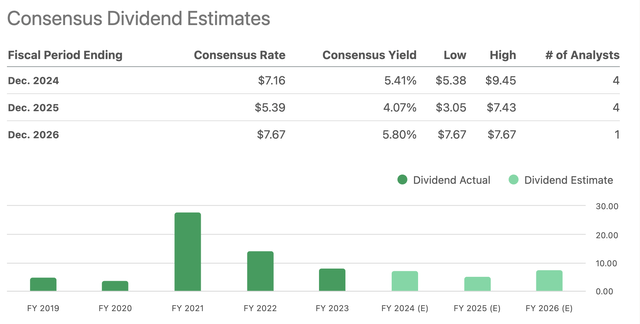

Looking ahead, the four Wall Street analysts covering the company see more increases ahead, albeit at a slower growth rate:

AFG dividend estimates (Seeking Alpha )

Summing up, the American Financial dividend has an attractive yield, is growing quickly, and often delivers special dividends that drive up the yield to far more than 2.15%.

There are some risks associated with the dividends, both regular and special. They depend on the continuing profitability of the company, unlike the debentures, which should only fail if the company fails.

Special dividends are most sensitive to profitability, since they are irregular and only occur if, as the Co-CEOs explained, the firm has “significant” excess capital.

Regular dividends are more reliable and depend on what have become routine profits. Plus, management normally hates to reduce or stop dividends, since that implies the company is in some sort of financial trouble. As we know, that happened to many firms during the pandemic, but American Financial was still able to increase its dividend.

American Financial also uses some of its excess capital to repurchase shares, which increases earnings per share, and thus valuations. The Q1-2024 earnings report shows the number of outstanding shares falling from 85.4 million in Q1-2023 to 83.8 million in Q1 this year.

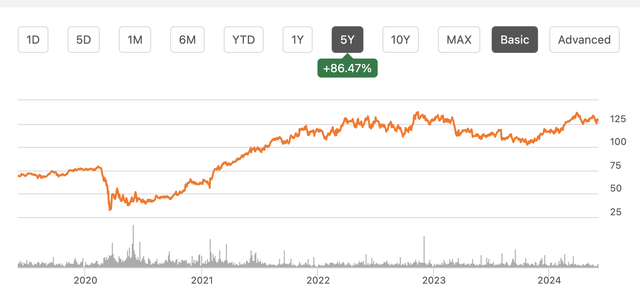

Buying AFG stock rather AFGC debentures also carries the potential for capital gains. Over the past five years, the share price has appreciated 86.47%, providing relatively rich capital gains to go along with the dividends:

AFG 5-year price chart (Seeking Alpha )

Comparing AFG debentures and dividends

The debentures, and specifically AFGC, are solid bets for income investors. While not risk free, they are close to it in my view. There is a possibility the company might exercise its right to redeem them, but that’s fairly low at the moment.

Looking at a spreadsheet of fixed income and bond yields published by Fidelity Investments on June 4, there are comparable yields available, but at higher risk. For example, 30+ year Corporate Baa/BBB bonds yield 7.41% (Moody’s gives AFGC a rating of Baa2).

Turning to dividends on AFG common stock, the current yield is 2.21%, roughly a third of the income provided by AFGC debentures. However, there are two wild cards.

First, there are the special dividends, which can be quite substantial some years, and modest in others. I believe, though, that they should be treated as bonuses. If they come, that’s good news. But, I would not treat them as a major factor in investment decisions.

The second wild card is the share price, something that affects AFG more than AFGC. The former is a conventional stock and the share price will reflect expected earnings, investor expectations, as well as other internal and external factors.

In the past year, AFG has varied between a low of $101.65 and a high of $137.72. That’s a difference of 35.48%. AFGC has fluctuated between a low of $18.23 and a high of $23.25, a difference of 27.54%. Of course, as AFGC nears its maturity in 35 years, the price will stabilize near its issuance price (par amount) of $25.00.

Overall, investors looking for above-average yields at relatively low risk should consider the debentures. They come from a strong company, one that has been profitable enough to pay special dividends every year for the past six years.

Valuation

The AFGC debentures began trading in 2019, and since then, the price has trended down, as we saw in an earlier chart.

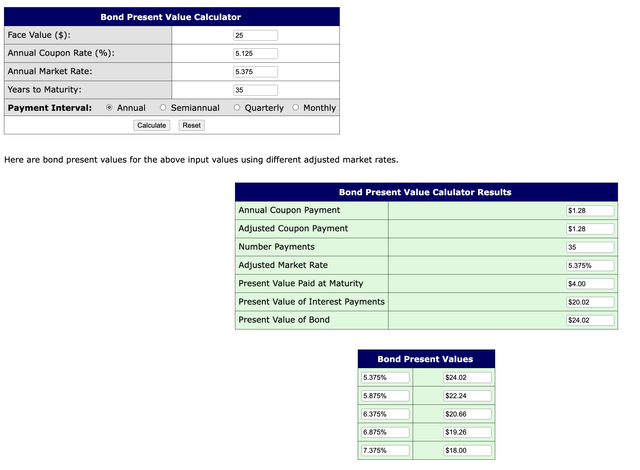

We know the price will eventually end up at $25.00, but in the 35 years before then, it will fluctuate according to interest rates and other factors. The bond present value calculator provides this assessment:

AFGC present value tables (buyupside.com)

The present value of $24.02 is 14.93% higher than the June 4 value of $20.90, making AFGC an undervalued stock. Combining the valuation with other data about the debentures and the parent company make it a Strong Buy; Seeking Alpha does not offer any other ratings for AFGC.

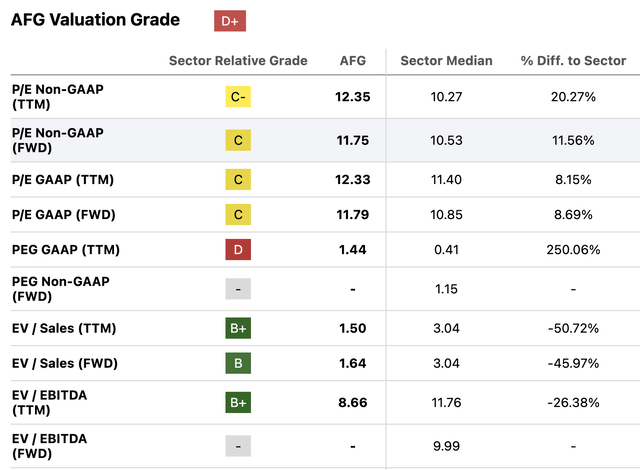

As for the parent company, it is considered expensive based on this excerpt from its Valuation page on Seeking Alpha:

AFG valuations table (Seeking Alpha )

The Wall Street analysts who follow AFG expect the share price to rise to $140.60 by June 4 next year, which would be a 9.90% increase. I think a more conservative estimate, based on earnings, is more appropriate.

The analysts expect earnings to grow by 3.79% this year and 8.86% in 2025. Averaging those two estimates gives us a midyear-to-midyear estimate of 6.33%.

Adding 6.33% to the June 4 price of $127.94 provides my AFG target price of $136.04. Based on this price, as well as what we know about the company’s underwriting and managerial successes, I rate AFG a Buy. That rating has also been provided by another Seeking Alpha analyst, while the Quant system offers a Hold, and Wall Street analysts provide two Strong Buys, one Buy, and two Holds.

Continuing growth at AFG should provide solid support for the price of AFGC.

Risk factors

As noted, parent company AFG has the right to buy back AFGC debentures and may do that if there is a significant change in interest rates. However, this risk is somewhat mitigated by the existence of two other series of debentures at higher rates.

Although this security has a fixed interest rate, it trades like a stock and the share price fluctuates. Therefore, there is a risk of capital losses from owning it.

The sustainability and investor confidence in AFGC debentures rests mainly on the stability and expectations about the parent company, AFG. Any loss of trust in AFG could cause a capital loss for AFGC shareholders.

Insurance companies can cover off much of their risk through reinsurance and other measures, but there is always a risk of catastrophes bearing costs the company is unable to meet.

If AFG becomes unable to pay special dividends, investors may lower their expectations and the amounts they are willing to pay for the stock of both the company and its debentures.

Conclusion

Both the American Financial Group’s stock and its 5.125% debenture now yielding 6.17% are good investments.

The common stock and dividend route is suitable for younger or more risk-tolerant investors, because of the potential of special dividends. In addition, there is a reasonably good probability of more capital gains in the future.

Debentures such as AFGC 5.125%, 2059 will attract income investors who want relatively strong distributions with little risk and a positive valuation, which is why I have rated it a Strong Buy. The underlying company is growing and profitable and will likely remain on that track for the medium to long term.

Read the full article here