Investment Outline

The share price for AMN Healthcare Services Inc (NYSE:AMN) has been a rollercoaster the last 12 months and now sits around 20% higher than the lows it had back in early April this year. But is the company worth buying into right now? Well, the market seems conflicted here. There is a rather larger short interest for the company at over 15%. The p/e sits at just 12, below the sector by nearly 40%. But when we look at the growth prospects and estimates of the company, it seems quite solid. Until 2027 the EPS is estimated to grow by around 24% which would be a CAGR of 6%. With no dividend, there isn’t such a strong buy case here, I think. The potential returns rely on the market deciding to give AMN a higher valuation, which would be the consequence of raised guidance or a significant beat on earnings. Back in May, AMN beat on both the top and bottom line for earnings, but with the coming earnings report on August 3, I think AMN is best rated as a hold.

Recent Developments

AMN Healthcare operates in the United States as a healthcare workforce provider for solutions and staffing services. This gets them a very broad set of regions and markets to serve. Healthcare workers are necessary in many areas, such as schools.

In a recent survey that AMN published on July 24, it showed that the majority of schools are understaffed with health professionals. This is setting AMN up as a solid option to supply the demand and better the environment there.

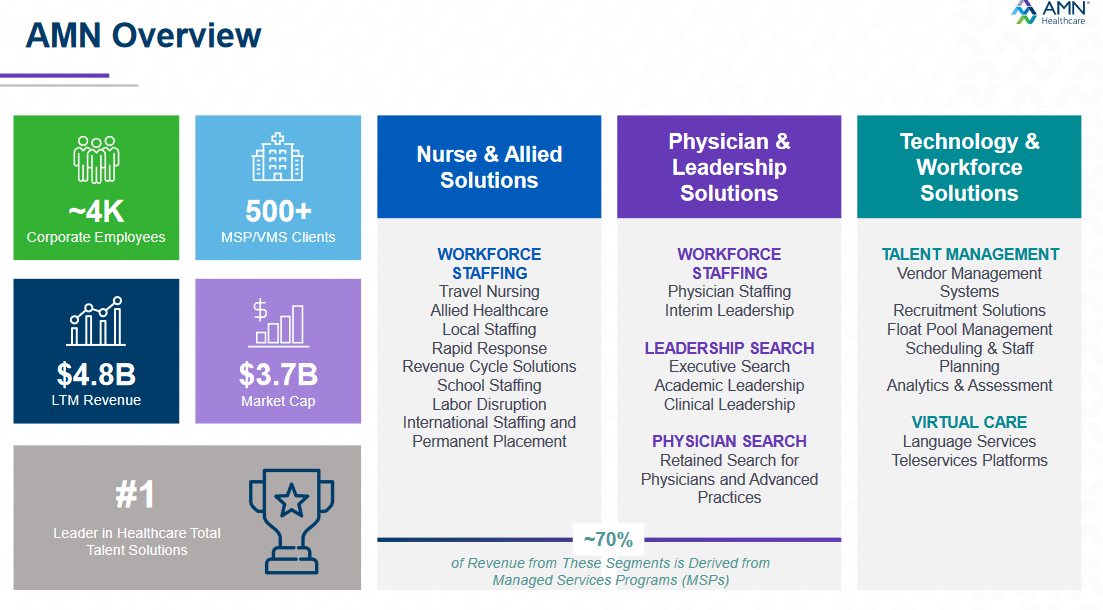

AMN Overview (Investor Presentation)

The President of AMN’s Schools division said the following regarding the results of the survey, “Many public schools are struggling to find the healthcare professionals they need at a time when the fallout from COVID-19 and rising mental health challenges are driving demand for school-based caregivers”. The need for filling these empty spaces is great and with AMN already boasting a strong network of clients and customers, over 500, they are in a great position to take a leading role here.

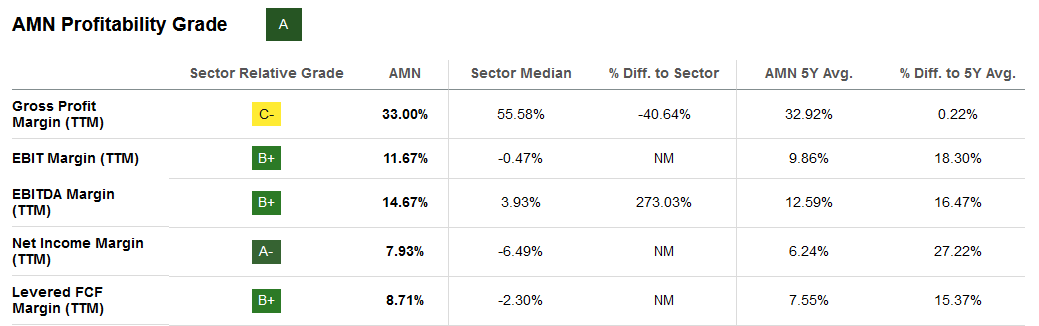

Margins

Margin Profile (Seeking Alpha)

The margins of AMN are quite impressive, I think. The company has managed to beat out the sector on many fronts, like the net margins and FCF margins, which I am looking mostly at. With FCF margins nearing 9% the company has had a lot of spare capital to spend on buying back shares. Something they have done a lot of recently. Since 2021 the shares outstanding have decreased by 10% which has strengthened the position of any investor in AMN.

Looking at the coming Q2 report from AMN, I don’t think we are likely to see a significant move to the margins. The company has taken on more debt, but this hasn’t increased the interest expenses drastically yet. Long-term debts sit at just under $1 billion, and AMN is having to pay back a significant amount of it any time soon, it seems. The TTM debt repayments are $70 million.

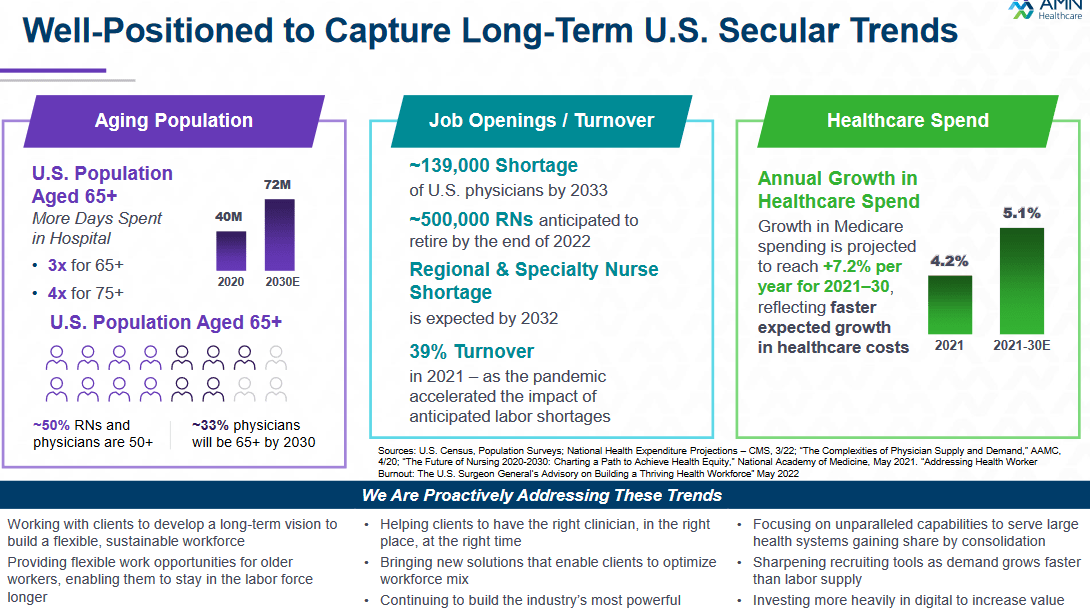

Company Position (Investor Presentation)

What will be driving long-term margin expansion seems to be several secular trends that AMN is well positioned for right now. Some of these include an aging population, which increases the average number of days spent in hospitals and the overall number of people that need to use them. This puts demand on workforces, and they need to find sound solutions, which AMN of course can help with, as we have discussed. Looking at how this could impact the margins, it would come from better cost efficiencies and operational performances. Demand drives higher prices and if AMN maintains solid expansions they can tap into the $40 billion healthcare staffing market much more efficiently. Ultimately, I think this will be driving margin expansion for AMN, but I also want to see proof of this concept and theory before suggesting the company as a buy.

Valuation

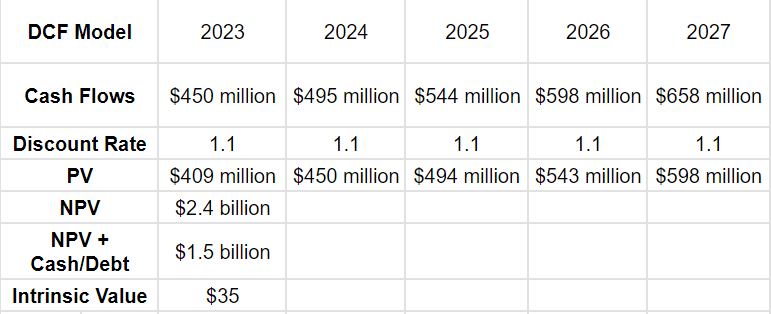

DCF Model (My Own Model)

As for my DCF model above, here I am assuming a 10% annual growth to the FCF. This is a fair bit below the 25% CAGR that has been achieved in the last 10 years. I find it unlikely this can be kept, and having a more pessimistic and realistic view of the model often leads to less risk for an investor. The intrinsic value comes out to $35 per share, which AMN is trading far above right now. Almost 3x more than the intrinsic value doesn’t make it a very appealing buy. What would switch this though would be the maintenance of the FCF growth they’ve had before. But that would also mean that AMN would most likely be trading at a higher p/fcf than it currently does, which is just 8 right now, 57% below the sector.

Risks

In evaluating the risks associated with AMN, one of the primary concerns lies in the management’s ability to effectively capitalize on their Workforce Solutions and stay ahead of the competition. While AMN has demonstrated its prowess in this domain, the rapidly evolving market dynamics demand proactive strategies to maintain a leading position.

With the healthcare staffing industry witnessing increased interest from various players, the potential entrance of larger competitors poses a substantial risk to AMN. If these competitors secure contracts at a faster pace and gain market share, AMN could face intensified competition, leading to potential revenue challenges and compressed profit margins.

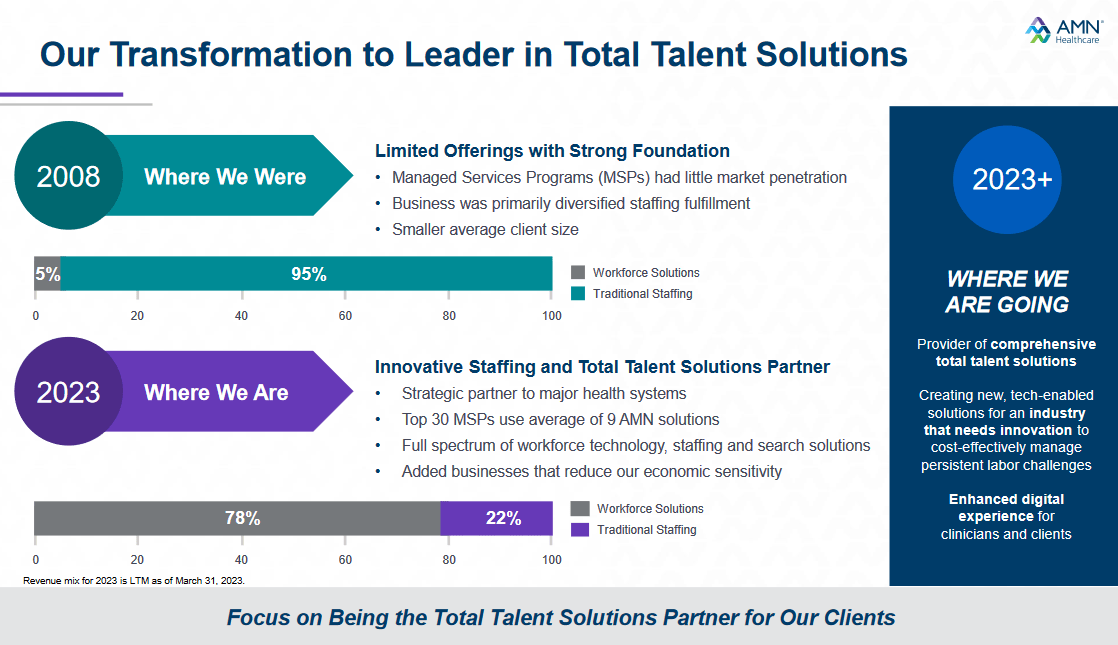

Company Transformation (Investor Presentation)

Moreover, the recruitment and staffing landscape is undergoing significant changes. The emergence of digital platforms, technological advancements, and shifting workforce preferences are reshaping how employers and jobseekers connect. AMN must continuously adapt and invest in innovative solutions to remain relevant and attract the best talent and clients.

Investor Takeaway

For investors that seek a healthcare play with a low valuation, it seems that AMN right now doesn’t offer enough potential and value to investors. The p/e sits very low, but the growth outlooks are rather flat or not that enticing I think, growing EPS just 6% annually until 2027. It makes sense the share price is trading where it does then. If there was a dividend included here, I think I might have other thoughts on the company, though. But for the meantime, I think AMN is best rated as a hold.

Read the full article here