Preamble

My regular readers would know I look for value, growth, and quality in the companies I write about. I have not published much lately as it has been much harder to find good quality, value investments with sustainable growth.

Amphastar Pharmaceuticals, Inc. (NASDAQ:AMPH) surfaced using Seeking Alpha’s screener is interesting. The parameters I set in Seeking Alpha’s screeners were:

- Long-term-debt-to-total-capital (between 0% to 50%)

- Past 3-years average revenue growth (greater than 10%)

- Forward Revenue growth (greater than 18%)

- Past 3-years earnings per share growth (greater than 15%)

- Forward earnings per share growth (greater than 26%)

- Price-to-earnings ratio (between 1 and 15)

- Net income margin (greater than 14%)

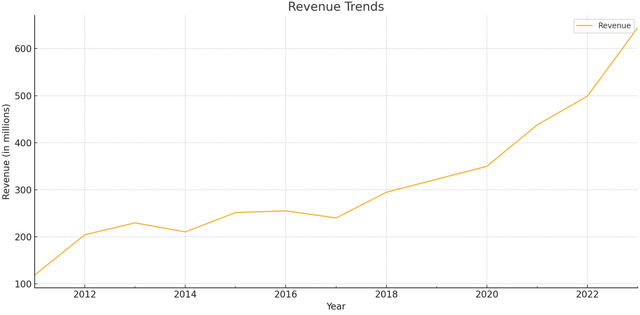

AMPH’s revenue growth trajectory looks good, convincing me to do a deeper dive.

Author’s using data from Factset

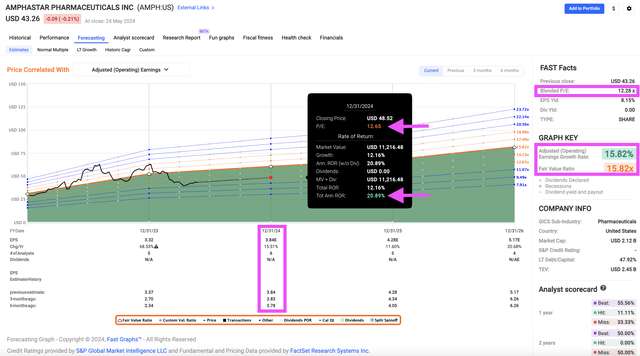

At first glance, the valuation looks reasonable too. Its blended valuation (P/E 12.28) versus its historical averages (2-year normal P/E 16.28; 5-year normal P/E 30.16), and analysts’ earnings forecast for 2024, 2025, and 2026, look very reasonable. Even if there is no PE expansion, so long as the projected earnings growth holds, AMPH could potentially return 20.89% by the end of the year.

Fastgraph

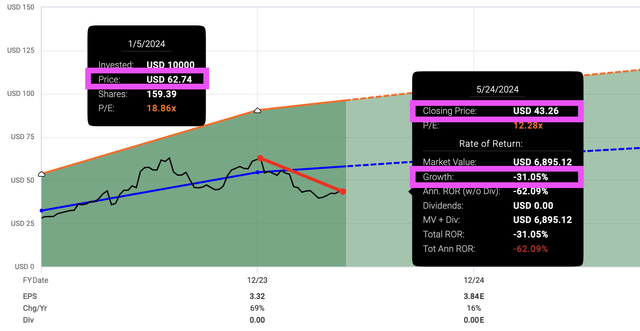

But why did a company that grew revenue and earnings fall 31% in 5 months?

Fastgraph

Let’s determine if AMPH is a value investor’s opportunity facing temporary headwinds or a business with deteriorating fundamentals.

Business Overview

According to AMPH’s 2023 10K (page 5),

We are a bio-pharmaceutical company focusing primarily on developing, manufacturing, marketing, and selling technically challenging generic and proprietary injectable, inhalation, and intranasal products, as well as insulin active pharmaceutical ingredient, or insulin API products. We currently manufacture and sell over 25 products, the overwhelming majority of which are prescription pharmaceuticals. Since December 2018, we have sold our patented Primatene MIST® using a new hydrofluoroalkanes, or HFA, formulation as our sole over-the-counter product. Our largest products by net revenues currently include BAQSIMI® glucagon nasal powder, or BAQSIMI®, Primatene MIST®, glucagon, epinephrine, phytonadione, and lidocaine.

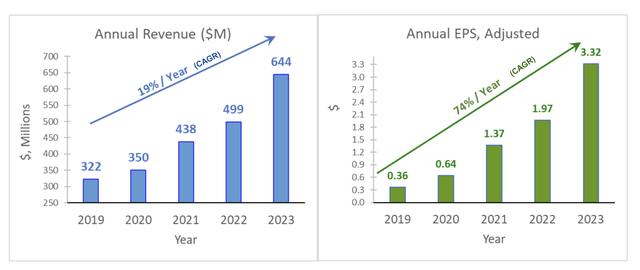

Overall, the company brought in $644 million in sales in 2023, a 29% increase in revenue from 2022. Over the past five years, AMPH grew sales at a 19% CAGR and adjusted earnings per share at a 74% CAGR.

Q1 2024 Earnings Presentation Slide

Business Strategy

Amphastar Pharmaceuticals, Inc. (AMPH) is in the generic biopharmaceutical business. That means that the company faces stiff competition from other generic pharmaceutical manufacturers. Also, due to the lower prices generics can fetch, the profit margins on these products are lower compared to brand-name products sold by bigger pharmaceutical companies.

The way AMPH navigates the competitive environment it is three-fold. First, it aims to sell products it described as “technically challenging generic and proprietary injectable, inhalation, and intranasal products” which require a higher barrier of entry. This is smart in two ways.

One, the competition is higher and barriers to entry are lower in the manufacturing of generics so by focusing on biosimilars more than generics, AMPH can better differentiate its products and charge a higher premium for them. For instance, the ANDA process for filing for approval of generic drugs do not require “preclinical (animal) and clinical (human) data to establish safety and effectiveness”. However, the approval process for biosimilars is different, known as the Biologics License Application or BLA. The data FDA requires in biosimilar applications include (1) analytical studies to provide data to support the structural and functional similarity of the proposed product to the reference product, (2) animal studies that may provide toxicology or pharmacology information, and (3) a clinical study (or studies) to prove that the proposed biosimilar moves through the body in the same way and provides the same effects as the reference product.

Even the generics AMPH sells are selected based on them having “difficult formulations, which require complex characterizations, difficult manufacturing requirements and/or limited availability of raw materials” to increase the barrier to entry and to reduce competition (page 11 of 2023 10K).

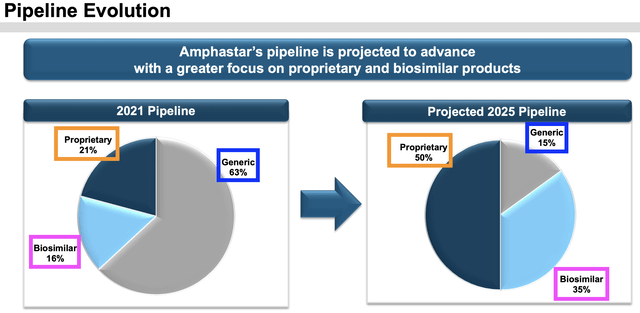

Two, the company is developing a pipeline of proprietary injectables, inhalation, and intranasal products. The intention is to shift the product mix from primarily driven by generics to mostly products under the proprietary and biosimilars categories which will offer higher barriers to entry to its competitors.

Earnings Presentation Slides Q1 2024

Secondly, it markets a diverse variety of products (25 being marketed, and 20 more at different stages in the pipeline) to reduce risks of intense competition in any one or two product categories that could lead to a price war that could reduce its margins significantly.

Thirdly, the products for the two markets – injectables and inhalables – that the company chooses to develop to drive growth are projected to have larger total addressable markets.

Based on the 2023 annual report (page 6), which states:

Injectable market – Based on a December 2023 IQVIA National Sales Perspective Report, the U.S. injectable drug market in 2023 was over $340 billion. Our generic development, including interchangeable biosimilar portfolio is targeting opportunities in over $11 billion of this market. The injectable market requires highly technical manufacturing capabilities and compliance with strict current Good Manufacturing Practice, or cGMP, requirements, which create high barriers to market entry. Due to these high barriers to market entry, there are a limited number of companies with the technology and experience needed to manufacture injectable products.

Inhalation market – Based on a December 2023 IQVIA National Sales Perspective Report, the U.S. inhalation drug market in 2023 was approximately $29 billion. Our generic development portfolio is targeting opportunities in over $6 billion of this market.

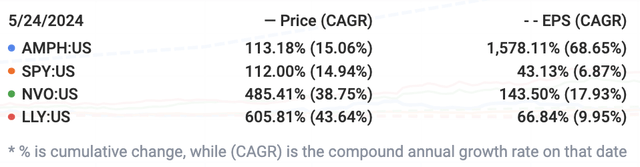

AMPH must be doing something right. For a company selling mainly generics, it has done pretty well compared to SPY and brand-name pharmaceutical companies like NVO and ELY. Its adjusted earnings per share grew by a CAGR of 68.65%, from $0.36 in 2019 to $3.32 in 2023, and Factset analysts expect AMPH to make $3.84 in 2024.

Fastgraph

Business Fundamentals

Sustainable Revenue Growth

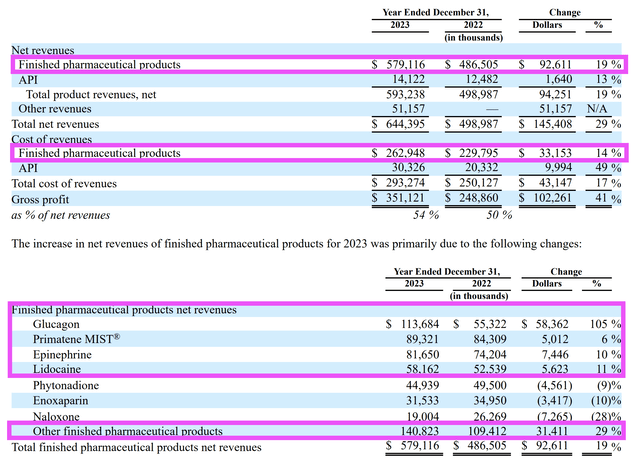

Year-on-year results, although mixed with growth in certain segments of the finished pharmaceutical products and a decline in sales in others, reflected a solid overall 19% revenue growth on the back of 14% in the cost of revenues.

2023 10K

Revenue has increased steadily over the years. Before the acquisition of BAQSIMI® from Eli Lilly & Company, revenue grew 2.17x from 2013 to 2022, growing even through the pandemic. That was very good. And with the BAQSIMI® acquisition and the supply crunch from injectable Glucagon, revenue grew 29% alone from 2022 to 2023, which is great. More on these two reasons later.

Author’s Compilation of Data from Factset; Ratio was calculated

All that is well and good but is the growth sustainable?

To assess that, one way is to look at how much the company spends to increase sales. It is always positive to spend less to make more.

Author’s

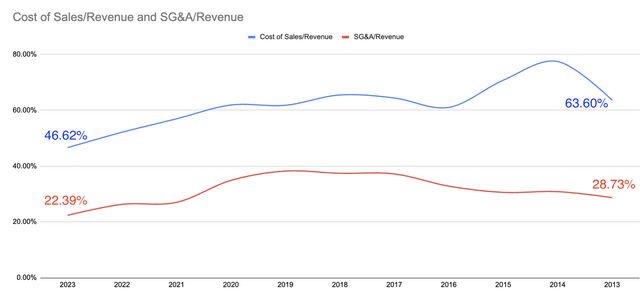

Over the years, AMPH has shown that it can spend less on sales and SG&A while increasing. In 2013, cost of sales was 63.6% of total revenue. By 2023, cost of sales has doubled but it is just 46.62% of that year’s total revenue. In 2013, SG&A was 28.73% of revenue. By 2023, SG&A has increased by 2.2x but it was just 22.39% of that year’s total revenue.

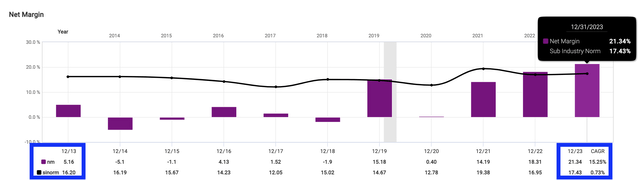

Margins Have Also Improved

In 2013, AMPH’s net margin was just 5.16%, far lower than the industry average net margin of 16.2%. By 2023, the net profit margin reached 21.34%, pulling ahead of the industry average net margin of 17.43%.

Fastgraph

Next, Lets Look At The Key Revenue Drivers Of AMPH

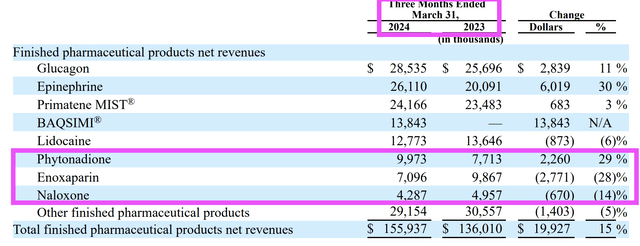

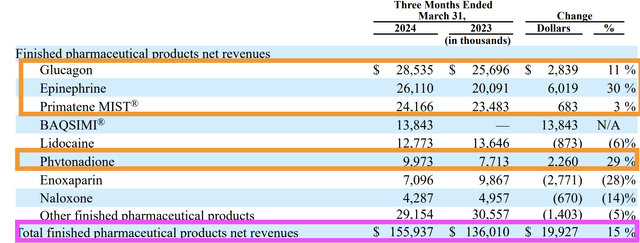

AMPH markets and sells 25 different products, but seven contribute the bulk of the revenue. I will begin by looking at products (phytonadione, naloxone, and enoxaparin) that experienced a decline in sales from 2022 to 2023.

The sales of phytonadione, naloxone, and enoxaparin face more competition, and consequently, show more fluctuations in their year-on-year and quarter-on-quarter results. For instance, year-on-year, sales of these three products fell.

Q1 2024 10Q

However, in the latest quarterly earnings report, sales of phytonadione jumped 29%. Commentary from the 2024 Q1 10Q (page 33) was as follows:

The increase in sales of epinephrine and phytonadione was primarily due to an increase in unit volumes, as a result of an increase in demand caused by other supplier shortages…

We anticipate that sales of naloxone and enoxaparin will continue to fluctuate in the future due to competitive dynamics. We also anticipate that sales of epinephrine and other finished pharmaceutical products will continue to fluctuate depending on the ability of our competitors to supply market demands.

CFO William Peters explained further in the Q1 2024 earnings call,

Epinephrine and phytonadione sales increased 30% and 29%, respectively, due to other supplier shortages for part of the quarter, with epinephrine sales increasing to $26.1 million from $20.1 million and phytonadione sales increasing to $10 million from $7.7 million.

The Star In The Product Line-up Is No Doubt Glucagon

The top four best-sellers are all reporting revenue growth in 2023 but the star that shines out is clear – Glucagon.

2023 10K

It was only in Q4 of 2020 that AMPH received the first-ever FDA approval of a generic version of rDNA Glucagon. Glucagon is used in injection emergency kit for the treatment of severe hypoglycemia and is used as a diagnostic aid.

Glucagon for Injection from AMPH product page

The eye-popping 105% growth in this product’s sales in 2023 was amazing, so it was important that Dan Dischner, Senior Vice President of Corporate Communications, added color to the sales expectations for Glucagon in the Q1 2024 earnings call,

As expected, our products such as glucagon injection, BAQSIMI, Primatene MIST and our hospital and clinical use offerings continue to experience steady growth. This reflects their ongoing importance and relevance in the market. Of particular note is the consistent demand trend for our hospital products which we anticipate will remain robust throughout the year. Our glucagon injection saw changes in demand, specifically in the diagnostics sector due to another manufacturer’s product availability.

He wanted to set the right expectations that although demand for Glucagon remains strong, the 105% growth in the Glucagon category in 2023 is not expected to be repeated in 2024 as that fantastic growth was due to a demand crunch for the product when two competitors discontinued their glucagon injection products at the end of 2022 (page 89, 2023 10K), and now that another company is entering the space, the same level of demand should not be expected.

But The Up-and-coming Growth Driver is BAQSIMI®

This is a product sold under the name BAQSIMI® which AMPH acquired from Eli Lilly & Company, or Lilly, in 2023. BAQSIMI®, the first and only nasally administered glucagon for the treatment of severe hypoglycemia in people with diabetes, is currently available in 27 international markets. Having this product open doors to a wider market for AMPH.

AMPH Product page

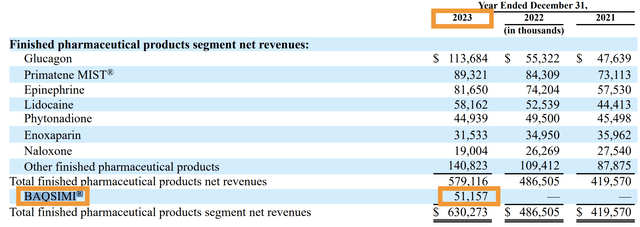

Unlike AMPH’s Glucagon product that needs to be first reconstituted before being injected into patients (instructions here), BAQSIMI can be administered easily in under a minute and no former medical training is required. Already in 2023, BAQSIMI booked sales of $51.157 million.

2023 10K

It is important to note that the $51 million figure did not paint a full picture of the product’s full potential as the way the sales were recorded is part of the Transition Services Agreement (TSA) with Lilly. According to the 2023 10K (page 88),

Revenues from the sales of BAQSIMI® under the TSA with Lilly during the year ended December 31, 2023, were recognized on a net basis similar to a royalty arrangement. The impact of this revenue recognition method resulted in lower reported revenues relative to the revenue that would have been reported had we recognized gross revenues from sales of BAQSIMI®.

In 2022, BAQSIMI® brought in $139.3 million in sales for Lilly, a figure that easily exceeded AMPH’s 2023 top product category by $25 million in 2023. This is a much newer product compared to the traditional injectable Glucagon, and hence it is not as widespread in its usage. BAQSIMI® worldwide annual sales were reported to reach $153 million and peak sales are projected by management to double from 2022’s figure to reach between $250 million to $275 million (slide 23 of the Q1 earnings presentation slides).

If everything looks rosy, why did the stock price crash 31% while SPY grew 11% in the first five months of 2024?

Reasons for the 31% Selloff

There could be four reasons for this.

Management Did Not Give Clear Guidance for 2024

Investors like certainty and when things are uncertain, they get worried. During the Q4 2023 and the Q1 2024 conference calls, management did not give specific guidance. There were positive comments regarding growth drivers:

- products such as glucagon injection, BAQSIMI, Primatene MIST, and our hospital and clinical use offerings continue to experience steady growth

- Primatene MIST… has maintained a steadily positive growth trajectory with consistent weekly in-store sales… we remain committed to achieving the $100 million sales milestone for this product in 2024 (translates to a 12.3% growth in this category year-over-year)

- potentially launching 4 to 5 products this year

Part of the reason for the lack of clarity is management is also struggling to get a handle on the exact timeline for revenue recognition for BASQSIMI. In the Q4 2023 earnings call, analyst Glen Santangelo wanted some help to frame 2024 in terms of this TSA that is in place with Lilly and how that arrangement would phase across the different countries. The reply from CFO William Peters was not very reassuring,

… it’s actually a little bit confusing to us, too. So — but here’s what I’ll say, that as I mentioned, 80% of the revenues from BAQSIMI come from the United States and part of the — we’re making that transition partway through the year…

So — and I don’t know, I could — feel free to answer some follow-up, because we don’t exactly know the exact date for most of these transitions either. Part of this has to do with inventory levels and winding down Lilly inventory labeling versus the Amphastar-labeled products and making sure that we have sufficient inventory of us to get launched. So it’s a little bit of a confusing process, so we don’t have exact dates either.

Increasing Costs In 2024

With the BAQSIMI acquisition, the increase in cost of goods and SG&A (around 17% of revenue) and other BAQSIMI-related expenses that were not there in 2023 may reduce earnings and pressure margins in 2024.

According to the Q1 2024 earnings, AMPH actually reported a 23% year-on-year growth in revenue.

2024 Q1 10Q

In the Q1 2024 10Q, management states that they experienced increased costs for labor and certain APIs and purchased components.

2024 Q1 10Q

The increase in expenses related to the expansion of BAQSIMI®-related sales and marketing efforts, and in salary and personnel-related expenses, are expected. And it should be expected that these expenses would continue to increase during the year.

Selling Pressure from Insiders and Institutional Investors

When a huge percentage of a company’s stock is being sold, and being sold in a short period of time, that creates a strong selling pressure.

As stated in the 2023 10K (page 73), CEO Jack Zhang and Chief Operating Officer Mary Luo own approximately 26.1% of AMPH’s outstanding common stock. As of 31 December 2023, there were 48 million shares outstanding. It was also stated that the two individuals have each pledged shares of their common stock to secure funds borrowed under existing credit lines from three financial institutions. All these lenders have varying rights including the right to conduct a forced sale at its sole discretion.

It was recorded that CEO Jack Zhang and Chief Operating Officer Mary Luo sold a huge chunk of their AMPH shares between January and April 2024. From 8 January 2024 and 10 January 2024, Mary Luo sold 170,196 shares. From 6 March 2024 to 17 March 2024, Jack Zhang disposed (which could involve selling, gifting, or donating) of 955,150 shares. Together, the duo disposed of over 1.125 million shares or 2.3% of the float.

Between September 2023 and April 2024, Morningstar’s Ownership page showed funds and institutional investors selling 5.817 million shares (12% of the float), more than the 1.961 million shares (4%) purchased.

With a total of around 14% of the stocks being sold in the last 6 months or so, the selling pressure on AMPH stock has been immense.

Regulatory Hurdle from the FTC

It always strikes me as weird when the FTC instead of the FDA meddles with pharmaceutical companies. Nevertheless, the headline below will chill shareholders.

FTC

It was reported that warning letters were sent to 10 companies, including AMPH. The letter sent to Amphastar Pharmaceuticals Inc. was regarding a glucagon nasal spray to treat severe hypoglycemia in type-1 diabetics, specifically, and it was referring to Baqsimi.

What are AMPH’s options?

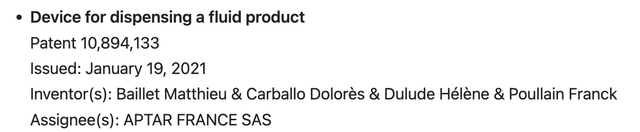

It can dispute the allegations of wrongdoing, or it could withdraw the listed patent. I believe management will do the latter as that is unlikely to impact sales of Baqsimi at all. I say that because the patent that FTC is questioning is the one having the patent number 10894133.

FTC Warning Letter

A check at Drugs.com – Prescription Drug Information reveals the details of this particular patent, which is for a device dispensing a fluid product.

Drugs.com

There are two more patents protecting Baqsimi, and those are the ones that matter. Patent 10,213,487, which expires in 2036, “provides a powder formulation containing glucagon or a glucagon analog for nasal administration, useful in the treatment of hypoglycemia, and in particular the treatment of severe hypoglycemia” and “provides a method of making this powder formulation, and to devices and methods for using the powder formulation“.

The other is Patent 10,765,602, which expires in 2039, “relates to a medication delivery system including a medication administration device, a medication within the medication administration device, a container defining a cavity receiving the medication administration device, and a cap attached to the container and sealing the medication administration device within the cavity.“

With the patent protecting Baqsimi’s formulation and the rapid dispensing method that gives it an edge over the current injectables, I do not think the projected sales of Baqsimi will be adversely affected.

Valuation

Amphastar Pharmaceuticals, Inc. (AMPH) shares look cheap no matter the angle I take.

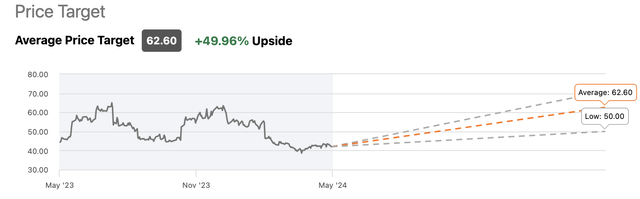

Wallstreet analysts are generally bullish about AMPH, with an one-year consensus price target of $62.50, representing an almost 50% upside from the current price.

Seeking Alpha

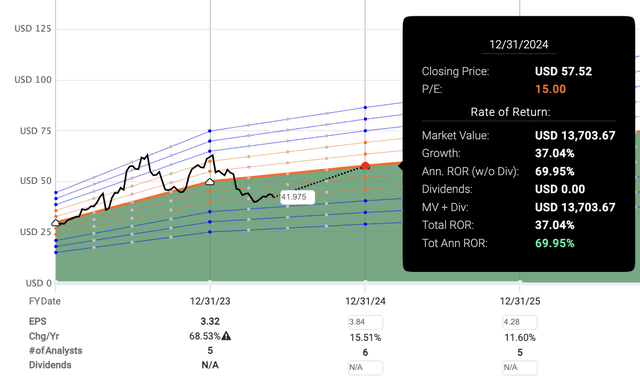

Assuming Factset analysts are right about their adjusted earnings forecast, AMPH would then be trading at just 10.8x 2024’s earnings and 9.7x 2025’s earnings. Compare that to AMPH’s normal P/E for the past 5-years (30.16), and 10-years (43.37). And it would only take a slight P/E expansion to 15 for AMPH to provide a 37% capital appreciation within the year.

Fastgraph

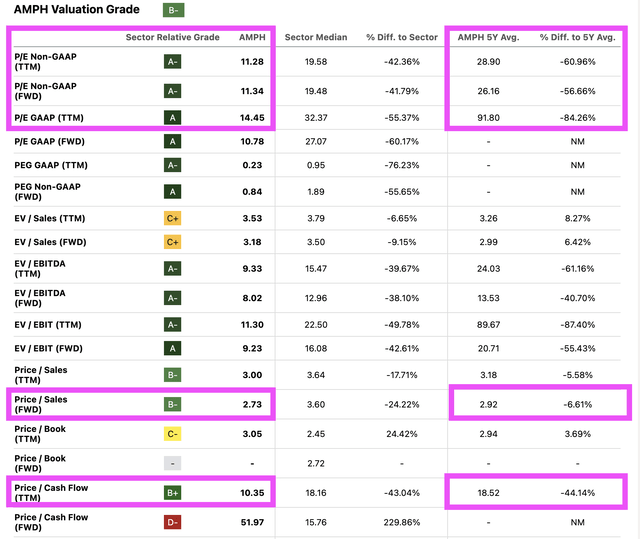

Comparing AMPH’s valuation metrics to its own five-year averages, AMPH is much cheaper from P/E, P/S, and P/Cash Flow perspectives.

Seeking Alpha Valuation Page

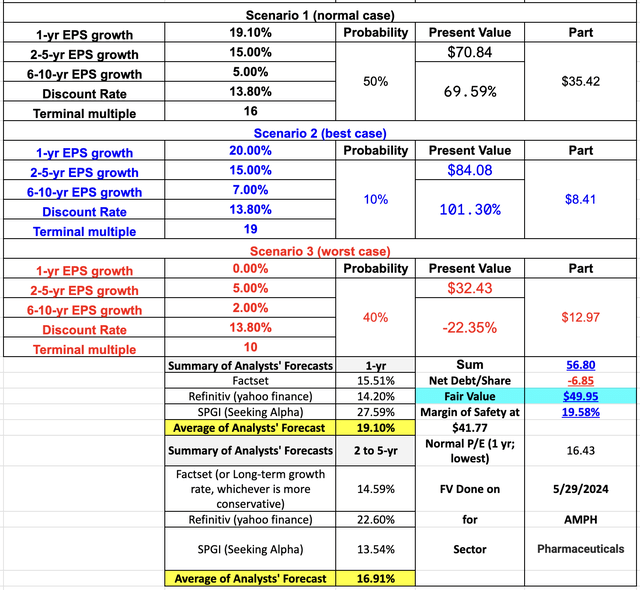

Finally, using very conversation assumptions below in my DCF analysis, I still get to a fair value of $49.95, which gives me a 19.58% margin of safety at a price of $41.77 per share.

Author’s DCF calculation

Conclusion

As a business, there are many things to like Amphastar Pharmaceuticals, Inc.: Its main revenue drivers are growing nicely, net margins have been improving and has exceeded the industry average. Over the past few years, it has been growing revenue and earnings nicely, and management has been executing their plan well of developing technically challenging generic and biosimilar products in injectable, inhalation, and intranasal markets that are identified to have huge demand. I think that AMPH is a company that is facing temporary headwinds. Thanks to these short-term issues, the stock has been punished excessively and I believe it is trading at a discount to its fair value. At a time when many companies capable of growing revenue and earnings are trading at valuation far above what is normal, AMPH is a rare find.

Read the full article here