Investment action

I recommended a buy rating for Analog Devices (NASDAQ:ADI) when I wrote about it two months ago, as I expected, FY24 to be the recovery year for ADI, and growth should accelerate in FY25. Based on my current outlook and analysis, I recommend a buy rating. My key update to my thesis is that I have more confidence in a recovery cycle happening in FY24 after reviewing the 2Q24 results. While the magnitude of the decline was larger than I had expected, I think it was a net positive, as management guidance suggests 2Q24 to be the trough.

Review

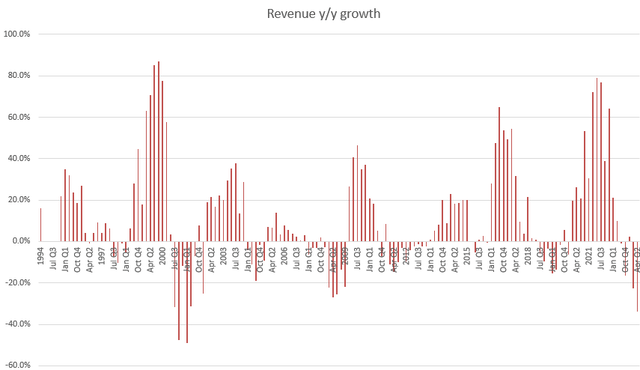

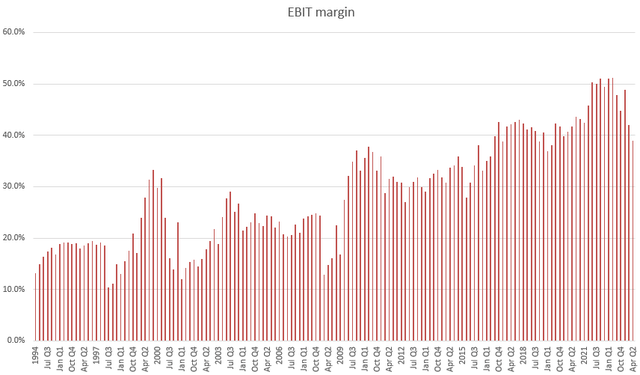

ADI reported 2Q24 earnings last week, with revenue down 14% sequentially and 34% annually to $2.16 billion. While the decline trend continued, this marked the first time over the past 7 quarters that ADI beat consensus estimates. By end-market, industrial revenue fell 42% vs. last year; communications revenue fell 47% last year; consumer revenue fell 12% last year; and automotive revenue fell 16% vs. last year. In terms of gross margin, 2Q24 adj gross margin fell by 700bps to 66.7%, down 230bps vs 1Q24. Consequentially, adj EBIT margin was down as well by 300 sequentially and 12.2ppts vs last year to 39%.

The biggest takeaway from this set of results is that 2Q24 seems to be the bottom of this cycle, after a 34% decline in quarterly revenue from peak-to-trough, and this can be inferred from two aspects.

Firstly, management cited an improving booking environment while noting that book-to-bill exceeded 1x in the quarter for the first time in more than a year. The reason why this 1x threshold is important is because it suggests underlying demand has improved, which has been a constraint to ADI recovery. Since ADI has the capacity to meet this demand, the improved backlog outlook paints a very positive picture for sequential growth ahead. The improving backlog outlook is well-supported by the encouraging design wins that ADI saw across various end markets. For instance, ADI won new deals across healthcare (surgical robotics and the continuous glucose monitoring market), industrial automation, and automative (ADI expanded GSML engagements from 12 to 15 of the top 20 customers).

Secondly, the 3Q24 guide includes an expectation for positive sequential growth (5% based on $2.27 billion revenue at the midpoint) for the first time over the past year, which reflects normalizing customer inventories and shipping closer to end consumption levels. Importantly, management saw improving trends across all segments, and I believe this comment carries a lot of weight given that the earnings call was held last week, which means management already has ~3 weeks of 3Q24 data.

ADI has done a really great job managing inventories. Inventory has now declined by 13% from $1.71 billion at its peak in the Jul’23 quarter to $1.48 billion at the end of 2Q24. This compares very well against other peers in the industry, such as NXP Semiconductors (NXPI) and Microchip Technology (MCHP), which only saw their inventory down by 2% from a peak-to-trough basis. In addition, management has stated that channel inventory was reduced to approximately 8 weeks at the end of the quarter and that it is expected to decrease even further in 3Q24 as we approach ADI’s target range of 7 to 8 weeks. The reason for my focus on inventory management is because it shows the potential for gross margin upside as ADI goes through the upcoming recovery cycle. The logic is that ADI is running at low utilization rates today to reduce inventories, and if we flip it around, it means that there is a lot of room for ADI to ramp up production (i.e., improve utilization rates) that carries high incremental margins given the fixed cost.

Valuation

Author’s work

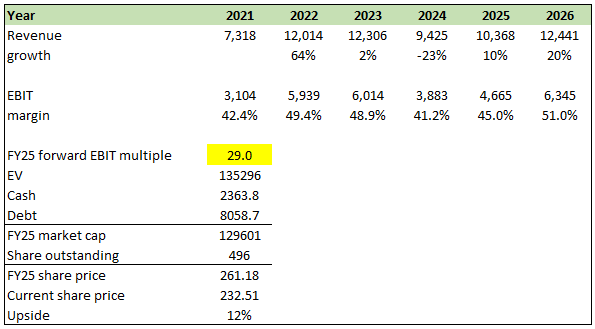

I believe the visibility of the recovery cycle has increased significantly. Hence, while I have reduced my FY24 expectations by a big delta (from expecting 3% growth to now expecting negative 23% growth), I believe this is a net positive situation. The reason for this big change is that I did not expect such a big magnitude of decline in 2Q24. I modeled a full-year decline of 23% by assuming 3Q24 to grow sequentially as guided and 4Q24 to see similar sequential revenue growth strength. For FY25, I am now more convinced that ADI is going to see a recovery, and based on historical y/y growth trends, FY25 should see ~10% growth followed by 20% growth in FY26.

For EBIT margin, the large magnitude of decline in 2Q24 dragged down margins naturally, and I have adjusted my FY24 estimates to reflect this weakness (assuming 2H24 to achieve 1Q24 EBIT margin since it is expected to grow positively). As ADI accelerates growth, I am expecting it to hit ~50% EBIT margin, which was what it achieved at the peak of the recent upcycle.

With higher visibility into a recovery cycle, ADI should continue to trade at a premium valuation multiple to its historical average. ADI now trades at 29x forward EBIT, way above its average of 20x over the past 5 years, and while the premium is huge, I think it is justified as I expect EBIT to inflect by more than 40% in FY26 vs. LTM2Q24, which implicitly means that ADI is trading at ~21x my FY26e EBIT (just 1x above the 5-year average; hence, I don’t think the current multiple is very demanding).

Author’s work Author’s work

Risk

I am still citing this from my previous post, as I still see this as the main downside risk to ADI’s investment case. The risk is that the recovery cycle doesn’t happen due to any possible reasons, including those that I have mentioned previously (the Red Sea conflict, the China/Taiwan conflict, the Russia/Ukraine conflict, etc.). The only difference today is that valuation is now a lot higher, and that also means that the downside is larger today vs. the last time I wrote about ADI.

Final thoughts

My recommendation is a buy rating for ADI. I believe there are strong signs of a recovery cycle underway. Revenue is expected to grow sequentially for the first time in a year in 3Q24, backed by an improving booking environment and a healthier inventory situation. Management’s commentary also suggests positive trends across all segments. While the valuation is at a premium, the potential for a significant EBIT margin improvement in the next two years justifies the current multiple.

Read the full article here