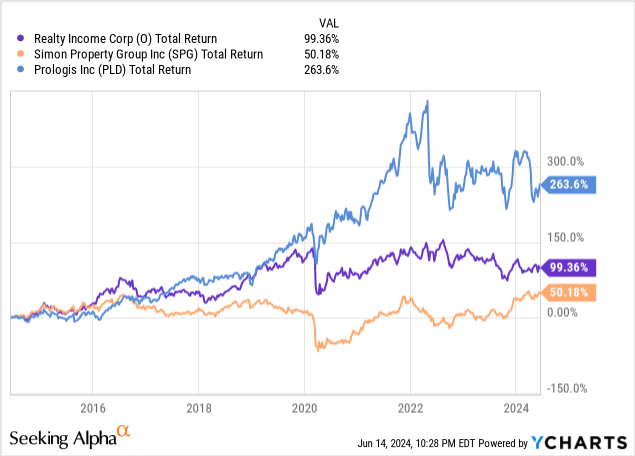

As we know, REITs come in a variety of shapes and sizes. Most discussion of REITs is centered around the best and biggest in the industry, including blue chip landlords like Realty Income (O), Simon Property Group (SPG), or Prologis (PLD). There is good reason as these companies own massive portfolios of high quality real estate and have established impressive track records, rewarding investors along the way.

However, these REITs are more similar than one might think. These equity REITs are in the business of building, owning, managing, and leasing real estate. The business model of developing and owning real estate is fairly bland once you look beyond the specifics of each asset class. Many of these behemoth landlords, including the three above, have earned themselves places among the 500 largest companies in the United States.

But there are hundreds of REITs, many of them unrecognized or working to establish track records of their own. Today, we travel to the world of mortgage REITs and explore a young and complex REIT operating in a unique niche. We will explore Angel Oak Mortgage REIT (NYSE:AOMR) covering different aspects of their business and the outlook.

Who is Angel Oak Mortgage REIT?

AOMR is an externally managed mortgage REIT that invests in non-qualified mortgage, or non-QM, loans. The REIT is small and managed by parent advisor, Angel Oak. The Angel Oak platform is a vertically integrated mortgage business combining sourcing, underwriting, loan acquisition, asset management, and securitization. The firm differentiates itself as an “originator” rather than an ‘aggregator”, meaning there is a focus on generating loans through their proprietary lending platform as opposed to acquiring loans from the balance sheet of another lender or bank. Before moving further, we should understand why this is critical for AOMR.

Mortgage REITs, or mREITs, are diverse businesses. Most mREITs invest in commercial mortgages held over large commercial properties such as offices, mixed use developments, apartments, or industrial facilities. AOMR is a residential mREIT meaning they invest in home loans as opposed to commercial mortgages. More specifically, AOMR invests predominantly in first lien non-QM loans.

Before diving into AOMR’s business, we should understand more about non-QM loans.

What are non-QM loans?

Like any loan, mortgages come in a variety of shapes and sizes. Two primary categories are qualified mortgage loans and non-qualified mortgage loans. Non-qualified mortgages are also known as non-QM loans.

Non-qualified loans are loans made to borrowers who do not meet the traditional requirements of standard loans. Most commonly, non-QM loans have a special income qualification such as no income or other sources than W-2. This could be self-employment income or non-income investment earnings. Some positive examples would be wealthy buyers in alternative income situations, buyers with lumpy annual earnings, or other uncommon situations. However, this can also include buyers who do not meet creditworthiness requirements of traditional loans such as low FICO scores. A non-QM loan doesn’t fit the requirements of the Consumer Financial Protection Bureau’s lending standards. Being “non-qualified” does not necessarily equate to poor credit.

Non-QM loans are usually more flexible with the credit history of prospective buyers. A non-QM lender such as Angel Oak may lend to a borrower despite a significant credit event in the borrower’s history, such as foreclosure or bankruptcy. Non-QM loans use different forms of income verification to approve prospective borrowers. Lenders and borrowers have more flexibility including longer term or interest-only payments.

The bottom line is that non-QM loans are not necessarily always more risky than qualified mortgages. The lenders require a unique set of verifications that differ from traditional lending requirements, but that doesn’t necessarily mean subprime.

Business Model

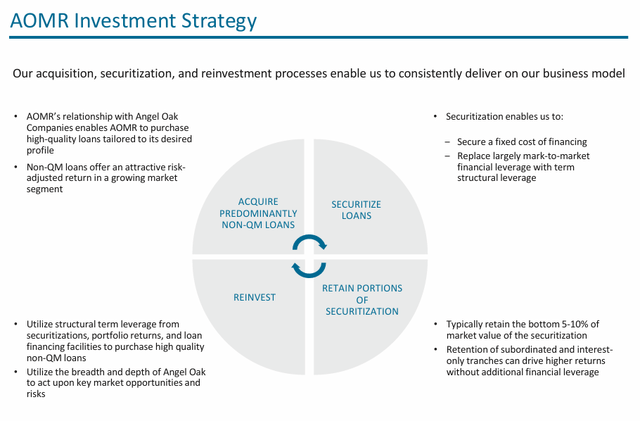

AOMR is a more complex business than most REITs. AOMR is an mREIT formed as the brainchild of Angel Oak Mortgage Lending and Angel Oak Capital Advisors.

Angel Oak Mortgage Lending is a vertically integrated lending platform founded in 2011. The platform is a non-bank originator of non-qualified mortgage loans serving at the primary sourcing mechanism for AOMR. This segment of the business identifies and underwrites non-qualified home purchasers who fit their credit criteria. The lending segment is closely tied to the mREIT portion of the business, acting as an origination vehicle for AOMR. Remember, AOMR describes themselves as an “originator” as opposed to an “aggregator.”

Angel Oak Capital Advisors is an alternative asset manager founded in 2009, specializing in mortgage lending and structured credit. The advisor is experienced in securitization and the structured credit market, specializing in RMBS.

Together, these businesses combine to form the “Angel Oak Ecosystem.”

AOMR Investor Presentation

AOMR focuses primarily on vertical integration to form an efficient business. While the mortgage lending segment sources and underwrites loans, AOMR is responsible for securitizing loans and selling the tranches to other investors. AOMR retains a portion of each securitization, but sells the majority with the intention of recycling proceeds back into new loans. This business is highly cyclical and heavily correlated to volume in the housing market.

Portfolio

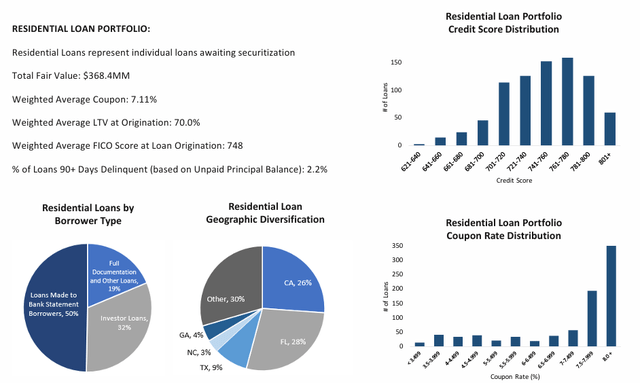

AOMR acquires loans from Angel Oak’s lending segment and holds them in a portfolio awaiting securitization. The REIT targets one securitization per quarter, providing consistent liquidity to accumulate and offload loans. In AOMR’s investor presentation, management provides insight into the current loan portfolio awaiting securitization, including details on LTV and credit scores. Interestingly, average FICO score at origination was 748 and average LTV was 70%.

AOMR Investor Presentation

However, more interesting is the geographic concentration of portfolio loans. Most loans are in high quality coastal markets including CA and FL which together account for more than 50% of the current portfolio.

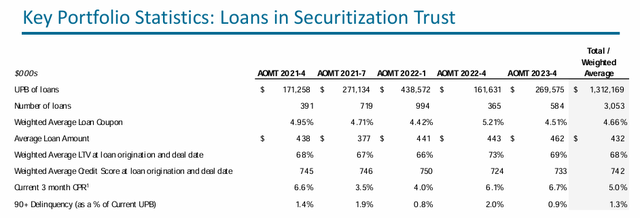

AOMR also includes information on historical securitization rounds over the past three years, including information on number of loans and delinquency rates. In total, AOMR has securitized over 3,000 non-QM loans over five rounds.

AOMR Investor Presentation

Securitization Structure

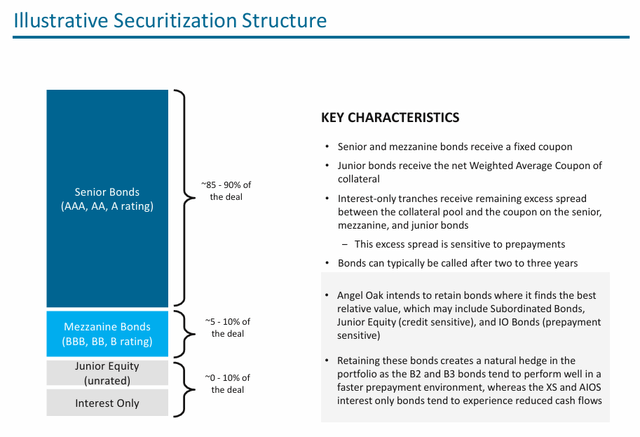

AOMR’s principal business of acquiring, securitizing, and selling loans is similar to other participants across securitized credit. Accordingly, the securitization structure is similar to a collateralized loan obligations or CLOs

The portfolio of loans is separated into tranches based on payment priority. Higher rated tranches receive a higher priority to payment and are rated accordingly. Junior tranches and interest only, or equity, tranches are the lowest on the totem pole, collecting the remnants of the spread between the collateral pool and coupon payments of senior tranches.

AOMR Investor Presentation

The model is extraordinarily efficient and continues to grow. AOMR sells the senior and mezzanine tranches, recycling the proceeds into new loans for future securitization. However, AOMR often retains positions in the interest only and junior tranches.

Dividend

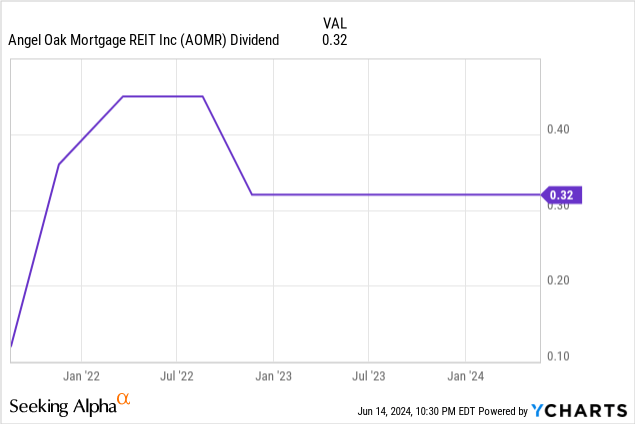

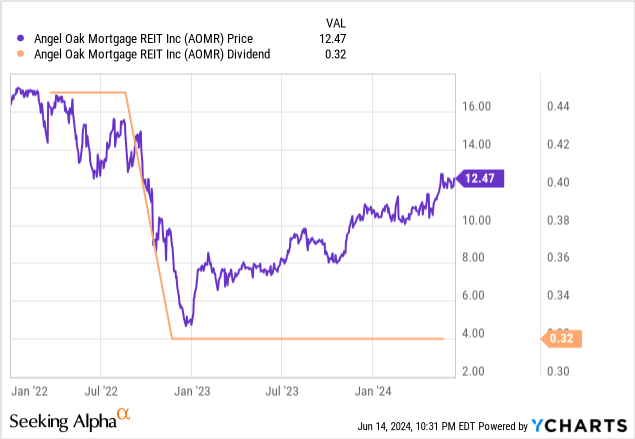

AOMR distributes quarterly dividends. AOMR paid their first full quarter’s payment of $0.36 per share in the fourth quarter of 2021. Shortly thereafter, the dividend was increased to $0.45 per share in the first quarter of 2022. Three months later, the distribution fell to $0.32 per share, where it remains thereafter.

AOMR’s business lends itself to an unstable dividend correlated to demand in the housing market. AOMR’s ability to acquire loans from their in-house lending segment is ultimately dependent on home buyers’ appetite for new mortgages.

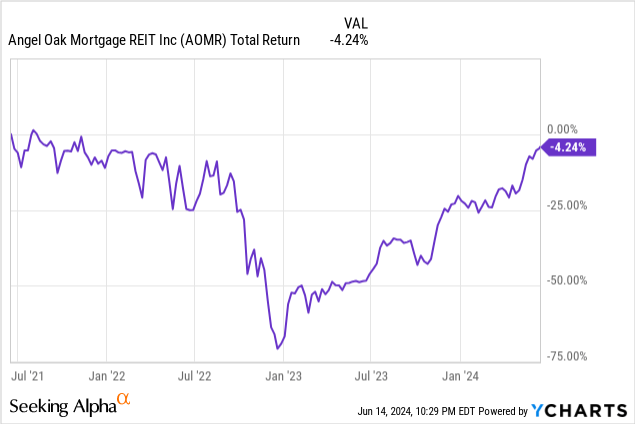

Even still, AOMR’s current distribution corresponds to a 10% dividend yield. The dividend is heavily linked to the short-term performance of AOMR’s business, residential mortgages. Let’s explore the outlook further.

Outlook

AOMR is a young business, having gone public in 2021. However, the business launched at an unfortunately tumultuous time for the mortgage sector. As we mentioned, AOMR’s business is different from a typical REIT. Most REITs are “buy and hold” investors to some degree. This means their performance is correlated to their respective asset class, whether commercial or residential.

A business like AOMR is different entirely. Rather than buying and holding single family homes like Invitation Homes (INVH), AOMR is a securitization vehicle for non-QM loans. This means AOMR’s business is in acquiring loans, securitizing, selling, and repeating. A key part of the recipe is healthy volumes of home loans. Angel Oak’s lending business is responsible for underwriting and lending, providing a healthy pipeline of loans for AOMR to acquire.

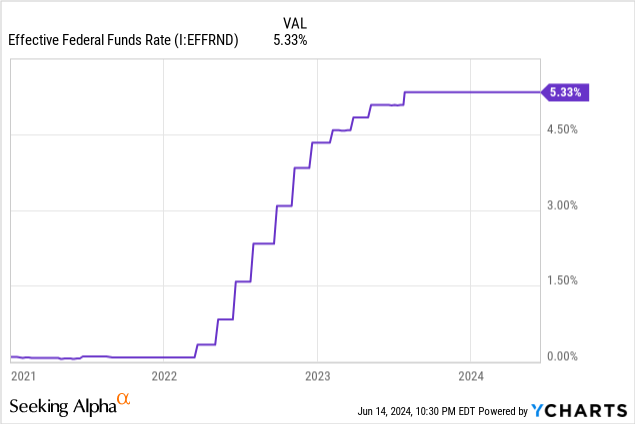

Over the past three years, the residential real estate market has been shaken by rising interest rates. Since 2021, the federal funds rate has increased by 500 basis points, marking one of the most rapid periods of increasing borrowing costs on record. Mortgage rates moved north accordingly, and home affordability has plummeted across the country.

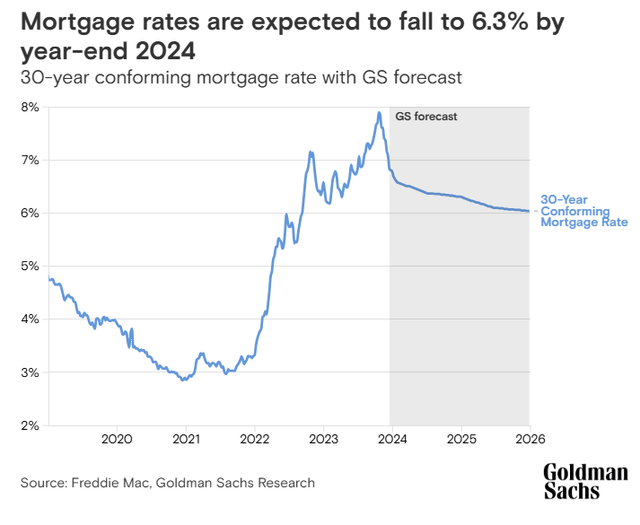

Goldman Sachs (GS)

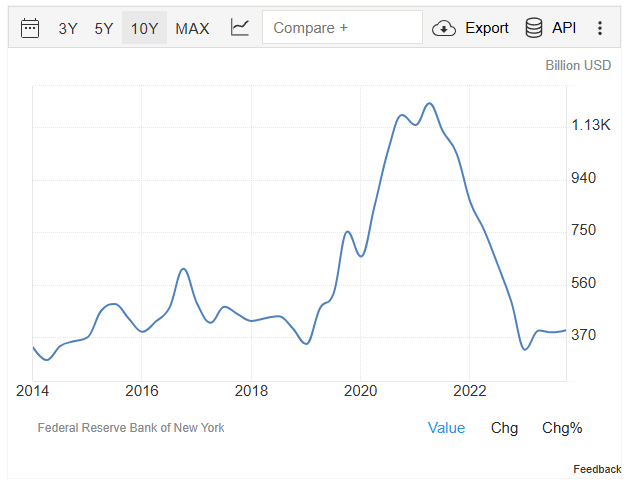

When AOMR launched, interest rates had bottomed below 3% for a 30-year fixed rate loan. Mortgages were cheaper than ever, and volume reflected the availability of capital. The mortgage renaissance of the post-pandemic era created a unique demand driver, which likely led to the formation of AOMR. The Federal Reserve Bank of New York provides details on mortgage origination volume:

Mortgage Originations in the United States increased to 393.77 Billion USD in the fourth quarter of 2023 from 386.37 Billion USD in the third quarter of 2023. Mortgage Originations in the United States averaged 583.59 Billion USD from 2003 until 2023, reaching an all time high of 1217.80 Billion USD in the second quarter of 2021 and a record low of 285.72 Billion USD in the second quarter of 2014.

Federal Reserve Bank of New York

Mortgage volume peaked when AOMR went public. Within 12 months, the demand had cooled significantly, pressuring AOMR’s volume-based business. AOMR’s share price and dividend distribution have been reflective of these demand trends since inception.

Conclusion

AOMR is one of the most unique REITs. Born from extraordinary mortgage demand and thriving with a vertically integrated, highly efficient business, this small mREIT has been one of the best performers in the segment over the past twelve months. Operating in a niche corner of the home loan market, AOMR lends to a unique customer set.

As investors are looking to rate cuts by year-end, there are catalysts aligning to potentially improve AOMR’s performance. Should rates decline, home sales could begin to improve as owners are motivated to begin transacting. Following several years of reduced demand, the backlog of homeowners itching to move for one reason or another is growing. Surging demand will build a pipeline for AOMR’s business to begin firing on all cylinders.

Should financing conditions begin to accommodate home sales, there could be significant money in motion. For a demand-based business like AOMR, this presents a potential tailwind. AOMR earns a “Hold” rating as the company continues to face headwinds impairing home sales volume. As performance improves, AOMR deserves a spot on watchlists.

Read the full article here