We have guided that it has been a wise investment decision to short Anheuser-Busch InBev SA/NV (BUD) stock following the consumer backlash stemming from its marketing campaign featuring transgender “TikTok star, Dylan Mulvaney, who promoted the company’s “Easy Carry Contest” on social media outlets and featured Bud Light prominently. A portion of the customer base disagrees tremendously with this and has called for boycotts. The boycott is clearly having a huge impact.

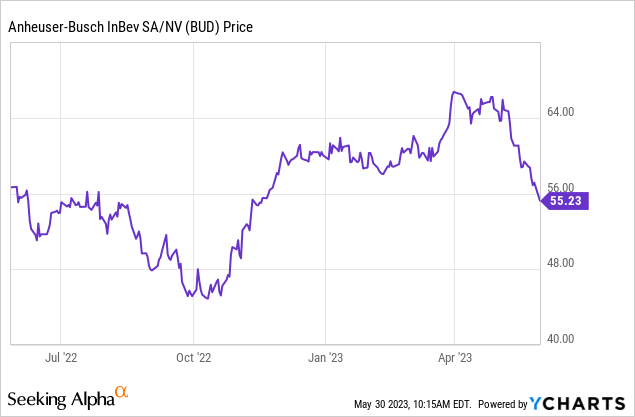

Last week, we told you sales were plummeting and that the stock was at a critical support. Take a look at the chart:

That support was identified to be about $56, and now BUD stock seems to be blowing through this level. Downside could be well under $50 now if sales data does not improve or if the company does not do something to win back its customer base. It may be too late for many to return, or, it could be a short-term impact. However, a review of the comments section of any article on this issue suggests lifelong customers may never return. For those who have not seen the video, it is here.

BUD stock has now retraced to and looks to be breaking below what we viewed as a very key level of support. In our opinion, if BUD stock does not recover the $56 level, there is at least another 10% downside here, and we think that sub $50 is easily in the cards if sales data continues to be weak.

Recent data has suggested sales are indeed plummeting, and a bearish take continues to be correct. Bulls need to circle the wagons at current levels in our opinion, as this is a pivotal spot for the stock. As you can see below, the BUD stock price is now sitting at a pivotal line.

Last week we told you that the Nielsen data showed sales of Bud Light are down dramatically, as volumes declined 24.6% in the week ended May 13th as compared to the same period in 2022. The consumer pushback had also spread to other brands. Now updated data is out, and it is getting worse.

We saw today updated data from consulting firm Bump Williams in an article in Newsweek. The firm has been following the sales trends for the company over the last few weeks following the controversy and uproar. BUD stock is to be avoided, and if you followed our shorting advice for members you have done well, probably best to hang on to short positions if you have them, but would not be a buyer here given all of the risk.

So, how bad is it now? Apparently, sales volume dropped an astounding 29.5% compared to the same period last year, while revenue from such sales was down 25.7% on the same week in 2022.

This comes as the company’s global CEO, Michel Doukeris, stated on May 4th that the dropping sales were less than 1% of the overall revenue. Given recent sales data, we think the company has to do more, whether it’s heavy marketing (there are massive rebates all over the country), or new commercials, etc., it seems no one is happy, as now the transgender community is also upset the company has not defended the backlash against Mulvaney.

Folks, the bottom line here is that the latest figures suggest the backlash is having a true and lasting impact on the beer brand’s U.S. revenue. This may has seen the degree of sales declines accelerate, capped by this 29.5% decline for the week ending 5/23. In April, the impact was a bit muted as the boycott began to spread more. Recall back in April Bud Light saw a decline in sales of 21.4% in terms of volume, or about 17% in revenue.

With this decline, there are now long ideas suggested for the competition, as Molson Coors (TAP) is seeing sales rise. Coors ight has seen a 22% year-over-year increase in sales. Looking at Miller Lite, there was a bit of backlash on their part for a very feminist or “woke” advertisement recently over the glorification and exploitation of females in the past, but that market campaign has been more tolerated, as sales of Miller and Coors Light continue to increase at Bud Light’s expense.

To be clear, other Anheuser-Busch InBev products have seen sales declines including Michelob Ultra, classic Budweiser, Natural Light, and Busch Light. In our anecdotal opinion, we believe that as consumers boycotting Bud Light learn of more of the parent company’s brands they are also actively avoiding them. More data is needed to support this assertion, but it seems plausible.

We believe it is clear that the consumer backlash is having an impact.

We want to remind you CEO Michel Doukeris earlier this month recently said, “our full year EBITDA growth outlook is unchanged.” At this point, Quad 7 Capital and BAD BEAT Investing are making the call here that the company will guide down during its Q2 report, if not sooner, especially if these trends continue. Recall they guided for EBITDA to grow between 4-8% and its revenue to grow ahead of EBITDA from a healthy combination of volume and price. But these sales numbers suggest the top line is going to come in much lighter than expected. The market is selling the stock down as it realizes that the data simply is damaging.

Final thoughts

Shares of Anheuser-Busch InBev SA/NV are down about 17% now since the marketing partnership occurred. Critical support looks like it’s being breeched, and Anheuser-Busch InBev SA/NV shares could have at least 10% more downside, if not much more if the data does not improve.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here