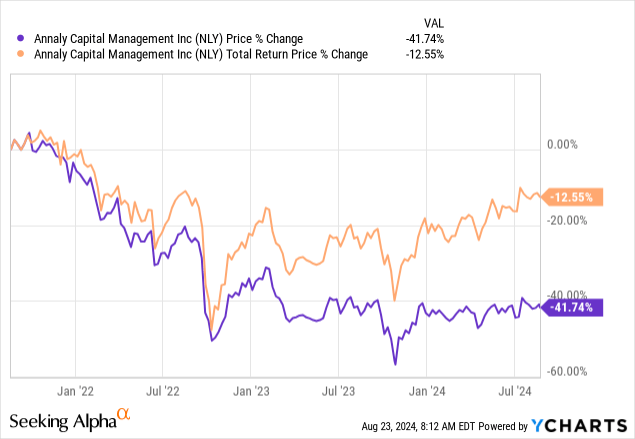

In the chorus of constant bullishness, two things have been clear for Annaly Capital Management, Inc. (NYSE:NLY) investors. They have not made money over the last three years, and they have been subjected to one dividend cut.

But, of course, the current thinking is that NLY will be the best play on a rate cutting cycle. We go over what needs to happen for that assumption to pan out.

1) You Need A Good Spread To Make Spread Income

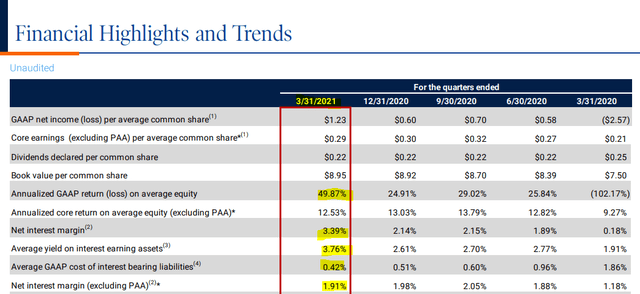

NLY is beholden to the yield curve. One of the reasons it has not made any money in the last few years is that its borrowing cost increases have outpaced its revenue gains. A good way to visualize this is to go back before NLY became a chronic eyesore. Back in 2021, it was producing massive levels of return on equity. Its net interest margin of 3.39%, coming from assets making 3.76% and liabilities costing just 0.42%.

NLY Q1-2021

Happy days.

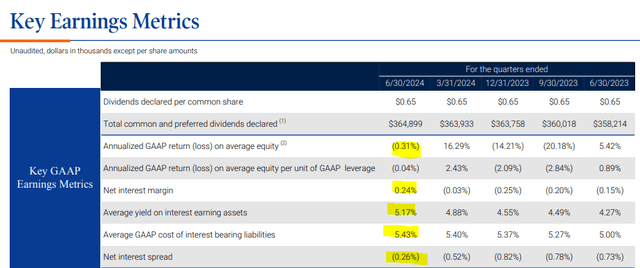

Fast-forward to today and the picture looks drastically different. This has come about even though average assets have yielded more. The highly praised mortgage-backed securities are indeed paying more than almost any other period when you benchmark against longer-dated Treasuries. But unfortunately, NLY maintains maximum susceptibility to the spread between shorter-term rates and MBS.

NLY Q2-2024

So whatever level of rate cuts you get over time, you have to get to a happy place where NLY’s borrowing costs are lower than its MBS yield.

2) NLY Has To Navigate That Path Perfectly

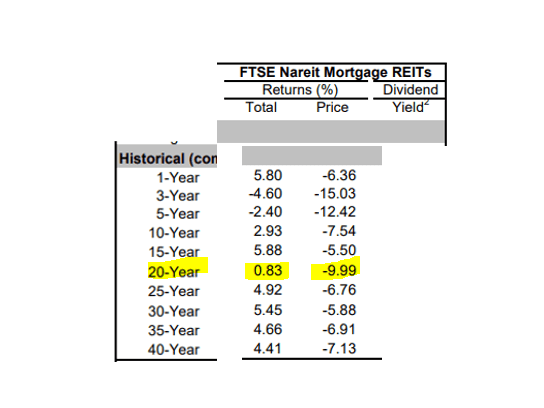

Buying and holding government guaranteed MBS is almost risk-free from a credit standpoint. You might miss out on other better opportunities. You might get plenty of prepayments that eat your expected return, but at the end of the day, you are generally not going to lose money over long timeframes. Unfortunately, no one can and no one should extrapolate that to mortgage REITs. The asset class has delivered 0.83% total annual returns over the last 20 years. So you got a big dividend and almost completely negated that by big price changes.

NAREIT

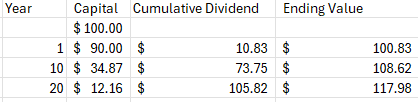

What does something like this 20-year return profile even look like? People have a hard time visualizing a 20-year flat return with such a big dividend. They keep creating weird goals about getting their money back, so everything else is just profit. Well, in mortgage REITs that can be an extremely painful journey. Over 20 years, the return profile, shown above, will result in your original $100 turning into $12.16. You will get $105.82 in dividends and that is how our total return becomes $117.98.

Author’s Calculations

One thing to keep in mind is if you invested for the income, you got two body blows that these numbers don’t show you.

The first is that you most likely have had to pay substantial taxes on the dividend. So your ending value most likely was not $117.98. Of course, if you held your mortgage REITs in an IRA, then one must ask why? If you don’t need the income, why chase after one of the poorest asset classes?

The second thing these numbers don’t tell you is that now your yield on original cost is in the neighborhood of 2%. If you assume you get a 14% yield on your $12.16, you are essentially getting $1.70 on our original $100 investment. Yea?

Our larger point is that over big cycles, mortgage REITs have not exactly done spectacularly. The last 20 years include quite a few interest rate cut cycles and also include a ZIRP era. NLY has to anticipate the changes in the entire curve fairly accurately to make money. They also have to know when to hedge and how much to hedge. Those things are quite complex to do with a 6-8X leveraged portfolio.

3) You Need This Inflation Cycle To Be An Anomaly

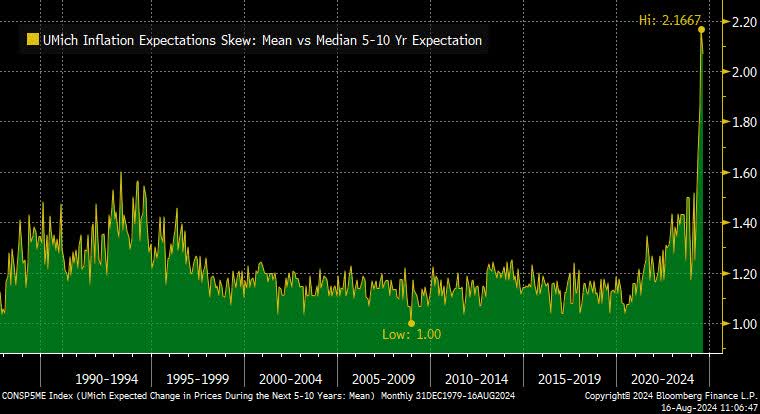

We all believe that, right? Before 2021, everyone felt there never would be any serious level of inflation. Now, at this point as well, we are all convinced that rates will go low and stay low forever. Blame it on debt, demographics, or the Easter bunny, but the average investor is convinced that the path for long-term rates is lower. Well, there are at least some contradictory pieces of information. University of Michigan skew (mean vs. median) on inflation expectations for one. #notanAIchart.

Bloomberg

Even the 30-year breakeven rate (which is an inflation expectation indicator) does not exactly look like it is collapsing.

Tavi Costa As Shared On X

So don’t assume this is it.

Disinflation while preserving labor market strength is only possible with anchored inflation expectations, which reflect the public’s confidence that the central bank will bring about 2 percent inflation over time. That confidence has been built over decades and reinforced by our actions.

Source: Jerome Powell On August 23 (emphasis ours).

If rates bottom out around 3.5%, and then we start seeing inflation reaccelerate, we might have another issue with NLY making money.

Verdict

The odds of NLY making money at this point (defined by total returns) are better than what it was before. The odds of Annaly Capital Management, Inc. stock beating 3-year CD remain just as poor as before. The intrepid can make trades here, for sure, but this remains a rather poor “buy and pray” stock.

Preferred Shares

NLY has a better buffer on its preferred equity than some comparable mortgage REITs. The three we have listed currently include,

1) Annaly Capital Management, Inc. 6.95% PFD SER F (NYSE:NLY.PR.F) which has a floating rate of three-month CME Term SOFR plus a spread adjustment of 0.26161% plus a spread of 4.993% per annum.

2) Annaly Capital Management, Inc. PFD SER G (NYSE:NLY.PR.G) is also in the same boat with a three-month CME Term SOFR plus a spread adjustment of 0.26161% plus a spread of 4.172% per annum.

3) Annaly Capital Management, Inc. 6.75% PFD SER I (NYSE:NLY.PR.I) moved to a floating rate in June 2024. The floating conditions are a three-month CME Term SOFR plus a spread adjustment of 0.26161% plus a spread of 4.989% per annum.

All three are fairly close to par on a stripped basis (next ex-dividend date of September 2 with about 60 cents accrued on each).

IBKR Aug 23, 2024

Those looking for longer-term security might gravitate towards NLY.PR.G. This is the least likely to be called out of the three. The two others should logically be called in the upcoming months, despite interest rate cuts. NLY should be able to place a new preferred in their place at a lower fixed cost if it ties the future float rate, to the 5-year Treasury.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult a professional who knows their objectives and constraints.

Read the full article here