Investment Thesis

ANSYS, Inc. (NASDAQ:ANSS) develops and markets engineering simulation software and services that enable engineers and researchers across diverse industries to analyze designs and improve product development efficiency. Its business is directed at the engineering simulation software sector and serves customers in various industries, including aerospace, automotive, healthcare, and more.

There are some positives and negatives to think about with ANSS. The positives include the fact that this business is highly cash flow generative. The negatives note is that its growth rates are around 15% (explained in the analysis that follows), and having to pay 25x forward cash flows for ANSYS is already a very rich multiple.

ANSS Near-Term Prospects

ANSYS specializes in the development and global marketing of engineering simulation software and services. Their software is widely used by engineers, designers, researchers, and students in various industries and academia, including high-tech, aerospace, automotive, energy, healthcare, and more.

ANSYS focuses on providing open and flexible solutions that allow users to analyze designs, either on-premises or in the cloud, to facilitate efficient and cost-effective product development from design concept to final-stage testing and deployment. Their simulation technologies cover a broad range of fields, from structural analysis and electronics to fluids, semiconductors, and more.

ANSYS aims to expand the use of simulation in product development, making it accessible to a broader range of users, and they also offer a variety of additional software tools and services to support the engineering and design process.

The following diagram is useful for comprehending the fundamental components that makeup ANSYS.

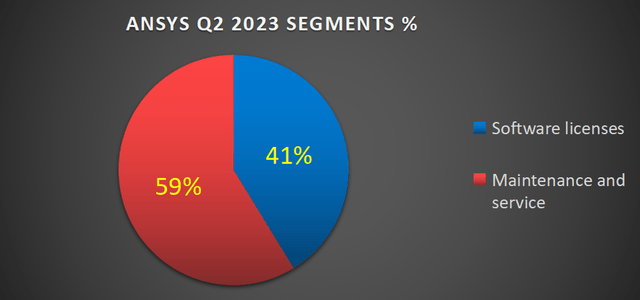

ANSS Q2 2023

As you can see above, its Maintenance and service segment makes up the majority of its revenues.

Moving on, ANSYS’s near-term prospects appear reasonable, driven by its robust pipeline.

ANSYS argues that it is well-positioned to capitalize on opportunities in the aerospace and defense sectors, which have seen significant growth. Additionally, ANSYS is actively integrating AI into its products, making simulation easier, faster, and more efficient, which will likely contribute to the company’s continued future opportunities.

In terms of products, ANSYS has a comprehensive portfolio, including multi-physics simulation solutions, which play a crucial role in industries undergoing transformations, such as aerospace. The company’s AI-driven innovations are expected to enhance the user experience and drive more simulation intensity across various sectors.

One challenge that ANSYS faces is the varying pace of AI adoption and its impact on different industries within its customer base. While high-tech and semiconductor companies are at the forefront of AI integration, industries like aerospace and automotive have longer development cycles, making the adoption of AI techniques a bit slower. This divergence in AI maturity across industries poses a challenge in terms of aligning ANSYS’s product offerings and strategies to cater to the evolving needs of its diverse customer base.

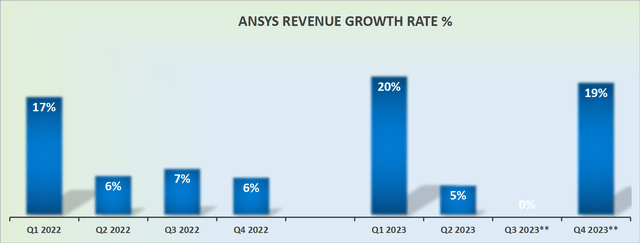

Revenue Growth Rates Require Interpretation

ANSS revenue growth rates

The most obvious aspect that strikes one when looking at this graphic is that Q3 sees no revenue growth rates and that Q4 sees a strong return to solid growth at close to 20% CAGR. With reference to Q3, this is what ANSYS stated on their earnings call:

Now in the quarter, the mix of license types which generate upfront recognition within the Q3 outlook, is relatively lower in 2022 versus 2023. So that’s what’s creating the year-over-year headwind in the quarter and that’s what’s causing the disconnect between the P&L [income statement] in the [Q3] quarter from the strong and accelerating third quarter and second half ACV outlook [Annual Contract Value].

Now when you look that year-over-year revenue and the resulting P&L in the third quarter, as we said, it’s not a reflection of momentum or any change in the business. And when you – if you consider the full year guidance and the Q3 guidance, and you can evaluate the implied Q4 revenue growth, you can see that, that outlook returns to strong double-digit growth.

And so that’s the reason why we’ve – our full year ACV guidance is really the best metric to observe momentum in our business. And that’s where we’ve seen kind of the continued progress and momentum.

In plain English, ANSYS argues that rather than relying on GAAP accounts, which in this specific situation aren’t especially informative, investors should look at ANSYS’s 15% CAGR in its ACV (Annual Contract Value) as a better indication of its underlying growth.

Let’s now turn our attention to ANSYS’ cash flows while keeping this background in mind.

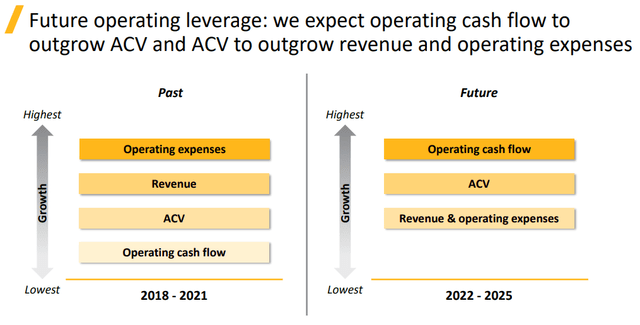

Focused on Growing Cash Flows

ANSS presentation

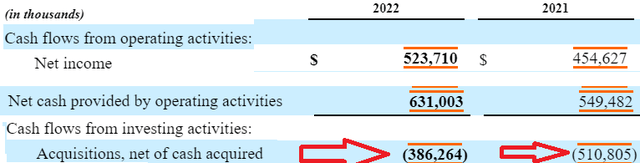

ANSYS has just over $260 million of net debt. And even though ANSYS is able to highlight its very strong cash flows, which are expected to reach slightly more than $700 million this year, we have to keep in mind the following matter.

ANSYS Q2 2023

ANSYS’s growth is supported in no small measure by several acquisitions each year. And given that its balance sheet isn’t as flexible as it once was, I have to wonder whether in 2024 there’s enough room left for any significant needle-moving acquisition.

ANSS SEC Filings

Finally, further confounding matters, the stock is priced at 25x this year’s cash flows. If one were to be willing to pay more than 20x forward cash flows, there are plenty of better options, with cleaner stories.

The Bottom Line

In evaluating ANSYS, Inc., it’s important to consider both the company’s strengths and potential challenges. On the positive side, ANSYS is a cash flow generative business with a robust pipeline and a focus on expanding its presence in the aerospace and defense sectors, which have seen significant growth.

Their integration of AI into their products aims to enhance efficiency and user experience.

However, uncertainty arises when assessing ANSYS, Inc. valuation. With a forward cash flow multiple of 25x, the stock is considered relatively expensive. The company’s growth heavily relies on acquisitions, and questions arise about whether there’s room for significant acquisitions in the near future given the current balance sheet constraints.

Furthermore, the varying pace of AI adoption across industries presents a challenge in aligning product offerings with diverse customer needs. Thus, while ANSYS stock holds promise, the high valuation and dependency on acquisitions raise questions about the level of investment risk associated with the company.

Read the full article here