Applied Materials (NASDAQ:AMAT) detailed its “eBeam Technology and Product Launch” in a webcast on December 14, 2022. The company uses this theatrical approach to introduce new products, and I discussed the launch in my December 20, 2022, Seeking Alpha article entitled “Applied Materials Ballyhooed E-Beam Inspection Sector Lost Share To KLA’s Optical.”

According to the bullets in that article:

- Applied Materials launched its new E-beam metrology/inspection technology on December 13, 2022.

- Despite efforts to promote its E-beam technology, Optical technology led by KLA continues to generate greater growth.

- Optical wafer inspection held a 5.4X market share value over E-beam technology promoted by Applied Materials.

- In the E-beam inspection sector, even ASML beats Applied Materials.

Applied Materials boasted about its “new” technology in 2022 but didn’t acknowledge that KLA (KLAC) dominated the market and that AMAT failed to mention that its “e-beam technology” isn’t surpassing KLA’s “optical technology” in market share, based on The Information Network’s report titled “Metrology, Inspection, and Process Control in VLSI Manufacturing.”

Later in this article, I compare market share for AMAT in the two main sectors its e-beam systems compete in.

AMAT vs. Competitors Metrology/Inspection Market Share

Chart 1 shows YoY revenue change of the Top 10 metrology companies for 2023 compared to 2022. These range from Company I growing +78% YoY to Onto (ONTO) growing -48%, according to The Information Network’s report.

AMAT’s revenue change, in the metrology/inspection segment of the overall WFE equipment market, was -30%. This compares to AMAT’s overall WFE growth of +0.1%, according to The Information Network’s report “Global Semiconductor Equipment: Markets, Market Shares and Market Forecasts.”

The Information Network

Chart 1

Table 1 shows revenues from semiconductor equipment sales to China between 2019 and 2023 for the Top 6 non-Chinese equipment companies. The last column is important and highlights that AMAT’s revenue growth for 2023 compared to 2022 was an impressive 66%, far outpacing competitors like Lam Research (LRCX), KLAC, Tokyo Electron (OTCPK:TOELY), and Screen.

Due to U.S. sanctions and China’s focus on producing trailing-edge chips (16nm and larger), AMAT’s sales of metrology/inspection equipment saw a 30% year-over-year decline, compared to AMAT’s overall WFE growth of +0.1%.

In contrast, KLAC experienced only a 12% YoY revenue growth from China in 2023. Consequently, their metrology/inspection equipment sales declined by only 8%, compared to a 14.2% decline in overall wafer fab equipment (WFE) sales.

This suggests that KLAC’s optical systems were not negatively impacted in China as they met the demands of process control for trailing-edge chips.

The Information Network

According to The Information Network’s above mention report, there are two major segments comprising the $12 billion Metrology/Inspection market in which AMAT competes:

- Wafer Inspection/Defect Review

- Lithography Metrology

In Chart 2, I show that AMAT had a 14.3% share of the Wafer Inspection/Defect Review segment in 2023, which dropped from a 15.2% share in 2022.

The Information Network

Chart 2

In Chart 3, I show that AMAT had an 11.1% share of the Lithography Metrology segment in 2023, which dropped from a 12.7% share in 2022.

The Information Network

Chart 3

Investor Takeaway

Not only is AMAT losing share in the metrology/inspection sector to competitors, including market leader KLAC, it is also underperforming in share price.

Chart 4 shows share price change for KLAC and AMAT over a 1-year period, showing a performance gain for KLAC (79.87%) over AMAT (71.33%).

YCharts

Chart 4

Chart 5 shows share price change for KLAC and AMAT over a 3-year period, showing a significant performance gain for KLAC (143.9%) over AMAT (66.88%).

YCharts

Chart 5

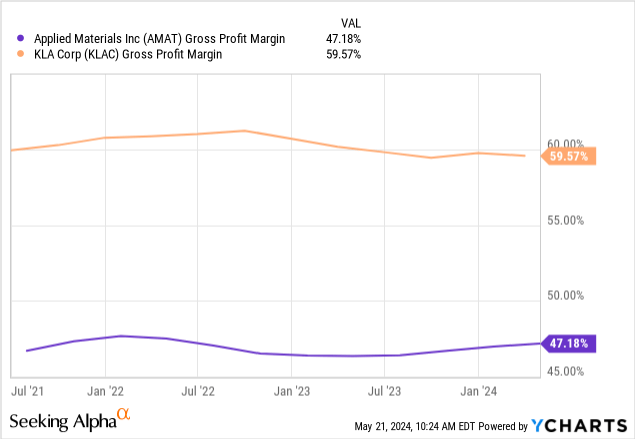

Chart 6 shows a significantly higher gross profit margin for KLAC than AMAT over a 3-year period.

YCharts

Chart 6

The hype behind AMAT’s theatrical montage for its new e-beam equipment doesn’t hold water considering market share data I’ve provided in this article.

Despite the strong growth of revenues from China, these sales actually hurts its business in metrology/inspection. Also, despite China sales, ASML overtook AMAT as the top WFE equipment company in 2023, as I detailed in a February 7, 2024, Semiconductor Deep Dive Investing Group article entitled ASML Led Global WFE Equipment Market In 2023 As China’s Naura Maintains 9th Position.

I continue to rate AMAT a sell.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here