REITs have been the safe haven in the market crash. This article will discuss the reasons they have been resilient and look at forward factors to try to determine if REITs will continue to be the safe haven.

The crash

The stock market peaked on February 19th, with the S&P 500 falling nearly 10% and the Nasdaq falling about 14% in the following month and a half.

S&P Global Market Intelligence

REITs have sat out the crash, staying relatively flat. Inclusive of dividends, REITs are up slightly year to date.

Let us begin by examining the reasons for the market crash and follow with a hypothesis on why REITs have so far been immune.

Why the market crashed

The financial media posits the following reasons for the market crash:

- Weak consumer sentiment.

- Stubbornly high inflation.

- Tariff uncertainty.

- Tepid employment numbers.

Each of these is a valid concern. However, the economy is a huge and complex machine that will always have some things wrong with it. Even in the best years, financial professionals could rattle off myriad concerns.

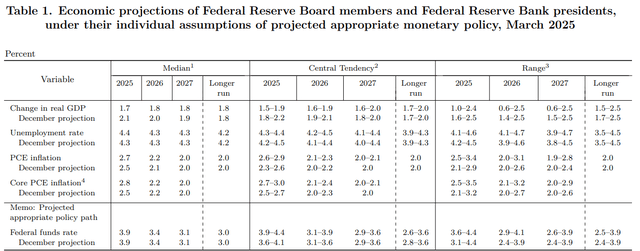

If we look at the economy overall, it looks quite normal. Below is the March Summary of Economic Projections from the Federal Reserve.

Fed summary of economic projections March

- Real GDP growth is expected to come in at 1.7%. This is slightly below normal but positive and significantly exceeds inflation as it is a real number.

- Unemployment at 4.4% is better than the historical average.

- PCE inflation at 2.7% is slightly higher than we want it (ideally at 2%), but really not that far from ideal.

Overall, it is projected to be a fairly normal year. It would fall right in the meat of the bell curve if one were to plot the historical range of economic scenarios. My guess would be somewhere around the 40th percentile.

Thus, while there are valid economic concerns, there are always valid economic concerns and these alone do not seem like enough to cause the market crash that has been observed in the last 6 weeks.

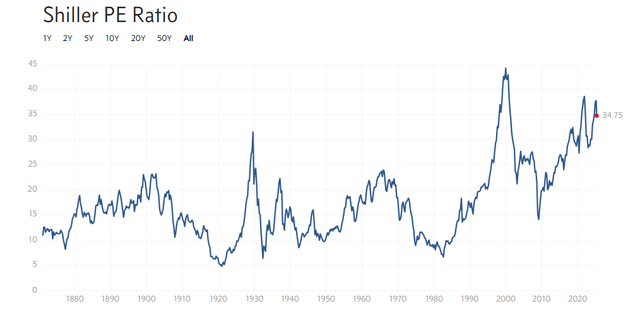

Instead, I posit that it is a reckoning of extreme valuation.

The S&P is precariously close to all-time highs on Shiller PE.

multpl.com

Even after the recent correction, Shiller’s P/E is roughly double the historically average valuation.

Valuation at that level is only sustainable if growth comes in strong and with the economy being slightly weaker than average, it seems difficult for companies to broadly achieve the requisite level of growth.

The NASDAQ, fueled by artificial intelligence (AI) anticipation, was even more aggressively valued. I suspect that is why it has fallen further.

The AI fundamentals remain largely okay with processor and other infrastructure sales still strong. It is just that linear strength is not enough to sustain multiples which requires exponential strength.

When priced for perfection, the reasonably small speed bumps of a tepid economy feel more like spike strips.

Why REITs are so far unscathed

REITs, unlike the broader market, did not reach lofty valuations. REIT valuation is well within historical norms on their primary metrics.

- Median P/NAV – 82.7% – cheaper than the historical norm.

- Median P/FFO -13.1X – within normal range.

- Median P/AFFO -15.3X – within normal range.

So while REITs would also prefer higher GDP growth, their valuation is appropriate for a tepid economy, so the stocks did not need to correct.

While I believe valuation played a large role in REIT outperformance during the market crash, there are also a couple of fundamental advantages

- REITs are largely isolated from tariffs.

- REITs are theoretically an inflation hedge.

As such, REITs are arguably more resilient to some main pain points of the economy right now.

Going forward, will REITs remain a safe haven?

I firmly believe that predicting short-term market price movement is unreliable, so the short answer is that I don’t know what will happen in the next 3 months.

However, from a longer-term perspective, I think REITs are well-positioned for the environment. Specifically, there are 3 foundational aspects which, in my opinion, make them better positioned than the broader market.

- Contractual growth.

- Valuation.

- The lack of new construction starts in 2024 and 2025.

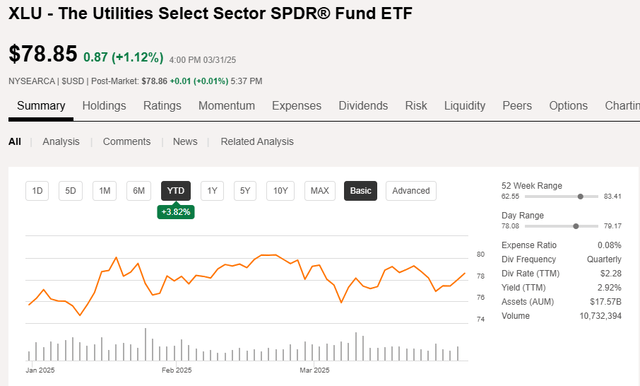

A substantial portion of REIT earnings growth comes from escalators in long-term rental contracts. These are pre-negotiated, resulting in a steady and predictable pace of contractual rent growth. When the economy is hot, they often get overshadowed by the fast growers and cyclicals. However, when the economy looks a bit weaker, reliable contractual growth becomes much more attractive than the unknown.

A parallel to this would be utilities which have similar steady, reliable growth. Utilities have also outperformed in the market downturn as measured here by the sector SPDR fund, The Utilities Select Sector SPDR® Fund ETF (XLU).

SA

Valuation

As discussed earlier, REITs are trading at a rather attractive valuation with a median FFO yield of 7.6%.

There is a bit of nuance to pay attention to, however, as there is quite a bit of variance within REITs. Large-cap REITs are currently substantially pricier than small and mid-cap such that the market cap-weighted REIT indices have significantly higher multiples than the median REIT.

The Dow Jones Equity REIT index, for example, has a P/FFO of 19.4X.

S&P Global Market Intelligence

That is nearly 50% more expensive than the median REIT.

You would find similarly high multiples in many of the popular REIT ETFs like the Vanguard Real Estate Index Fund ETF Shares (VNQ).

There are much better bargains to be had in selecting individual REITs.

Finally, perhaps the biggest reason we are bullish on the forward outlook of REITs is the lack of new construction activity in 2024 and 2025.

We discuss these supply dynamics frequently and perhaps too much for those who read all of our work, but it is a huge deal for REIT fundamentals.

REIT AFFO per share growth is inversely related to the construction activity of the preceding 2 to 4-year window, depending on the property sector. It is just so much easier to push rental rates up when there aren’t newly delivered buildings with which to compete.

High construction starts in 2021 and 2022 are why REIT AFFO growth was slow in 2023 and 2024 and the low construction starts in 2024 and 2025 are why REIT AFFO growth is going to come in strong in 2026 and 2027. It is just basic supply and demand principles, but the market seems to really miss this aspect of REITs.

Wrapping it up

REITs have been quite resilient in the face of the broader market crash. We believe they will continue to be the safe haven due to healthy valuation and a strong fundamental setup.

Read the full article here