Introduction

Ares Capital (NASDAQ:ARCC) serves the same purpose as all my other holdings, high-quality dividend stocks that provide me with income. But with ARCC, I view it a little differently. I have a mixture of income stocks like BDCs & REITs, and dividend growth stocks such as Starbucks (SBUX) & Kroger (KR). With BDCs you typically don’t get a lot of capital appreciation, unless you’ve caught them on a flash crash or something to that effect like what happened in 2020. But one thing you can usually count on getting is a steady stream of income, and if you’re lucky you’ll get some end-of-year specials or supplementals along the way. ARCC is my third favorite business development company behind Blackstone Secured Lending (BXSL) and Capital Southwest (CSWC). I covered why ARCC was a buy back in my July article, and in this one I get into why it remains one of my largest holdings and a no-brainer for investors looking for income.

Why It Remains A Core Holding For Me

ARCC has been doing all year long exactly what I’ve expected them to do. Continue to benefit from high interest rates while beating estimates the majority of the time, and continue to out-earn its dividend. While many other BDCs like CSWC & BXSL have raised their dividend more frequently since the start of rate hikes, ARCC has continued to hold the dividend steady in 2023 with no supplementals or specials. Of course, the supplemental and special dividends are a great addition to any investor’s portfolio, especially during the current macro environment. But ARCC’s decision to hold the current dividend tells me that management remains cautious going into 2024.

With an expected recession, it’s best for any business to retain as much of its earnings as possible for an unexpected, or in this case, expected downturn. Having cash readily available during tough times puts any company in a better position to navigate the situation. While several other BDCs are sprinting to the finish line by paying out their extra income to shareholders as a benefit of higher rates, ARCC prefers to retain theirs and roll it over, or in this case jog to the finish line while focusing on what’s coming.

And if the recession becomes bad enough, I expect they will look for opportunities to deploy capital and invest in distressed businesses for cheap. Management confirmed this by stating they expect an uptick in M&A and additional sponsor-to-sponsor portfolio company sales to accelerate next year. This allows the BDC, or any company for that matter to have the upper hand at the negotiating table when it comes to loan structure. They also expect stronger sentiment amongst middle market companies next year as they look to invest to grow their businesses, creating stronger transaction volume for ARCC in the process.

Q3 Earnings

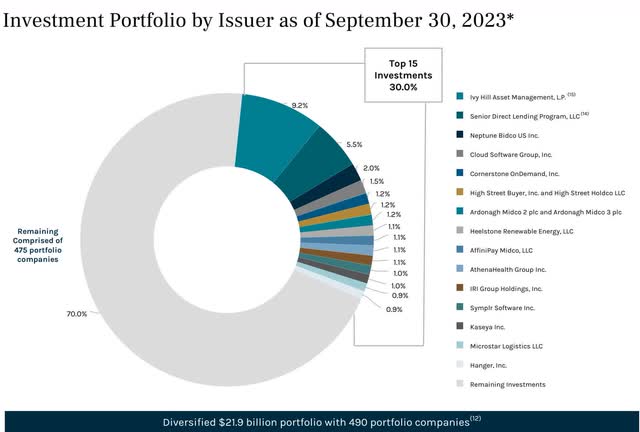

During the 3rd quarter NII fell from $314 million in Q2 to $289 million, but this was up from $288 million a year ago. They also beat analysts’ estimates by $0.01 on EPS but failed to beat on revenue, missing estimates by $4.14 million. Additionally, they managed to increase NAV by 2.2% quarter-over-quarter from $18.58 to $18.99. Although the BDC has been silent when it comes to dividend raises this year, they have been making noise with new investments. At the end of September, portfolio value stood at $21.9 billion across 490 companies and 25 industries, an increase of nearly 2% from approximately $21.5 billion at the end of June.

ARCC investor presentation

ARCC made approximately $410 million in new investments during the quarter with 97% of these being first-lien senior secured loans, and 2% in preferred equity investments, and 1% other equity. This activity made Q3 the third most active quarter in company history. Furthermore, 97% of these were floating rate investments with the other 3% being fixed rate and non-income producing. They also exited $158 million in investment commitments in the quarter as well.

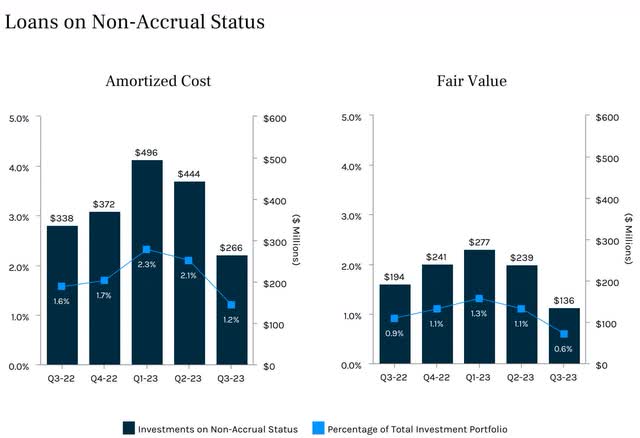

Decreased Non-Accruals

Although ARCC is one of my largest holdings and I consider it a sleep well at night stock, one of the biggest risks and something I have been keeping a close eye on is whether they had a rise in non-accruals in Q3. When I covered this last July non-accruals had begun to creep up above 2% as interest rates began to take effect. But I’m not surprised the company was able to decrease this as their management team is one of the best in the sector. During Q1 of this year, ARCC saw a rise in non-accruals from 1.7% to 2.3% because of the rapid pace of rate hikes.

Many BDCs enjoy the benefits of higher rates due to their floating rate loans to businesses, but some of their portfolio companies start to feel the pressure as the cost of borrowing goes higher, causing companies to become distressed. But as seen below ARCC’s has been on a decline from 2.3% in Q1 to 1.2% currently which is good to see. Despite the rise from the end of 2022 to Q1, this was still below their targeted range of 3%, and the KBW BDC average of 3.8%. One thing to note is if we do enter into a recession next year, investors may see another rise in non-accrual loans.

ARCC Q3 investor presentation

Healthy Balance Sheet & Leverage Decrease

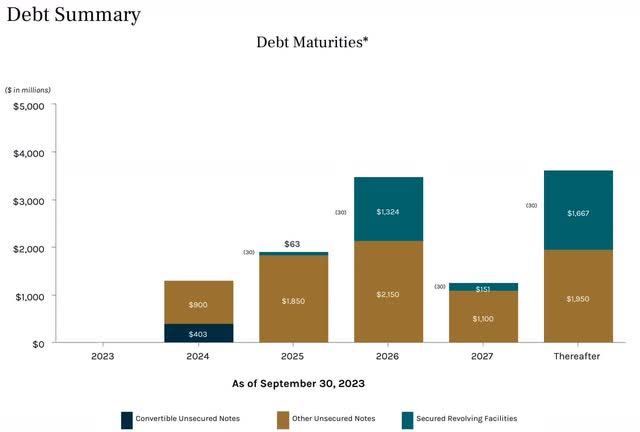

As previously mentioned ARCC managed to decrease leverage to 1.03x, down from 1.07x in Q2. And although they have no debt maturities this year, they have roughly $1.3 billion due in the first half of 2024 with $403 million due in March and an additional $900 million due in June. Both of these have an interest rate of 4.625% and 4.2% respectively. Even though I suspect a rate cut sometime in 2024, chances are they’ll be higher than ARCC’s current rate. This may be a reason the BDC has elected to preserve some income as well instead of paying out to shareholders. At the end of September they had a total of $11.5 billion in debt, a decrease from $12.2 billion at the end of 2022. They’ve also managed to increase cash on hand by nearly 74% from $303 million to $527 million over the same period and had approximately $5.3 billion in total liquidity.

ARCC Q3 investor presentation

This prepares them well going into 2024 by paying down debt and increasing cash. It tells me management is looking ahead and prepared to carry over spill-over income going into the next year, something they usually do. Because of their conservative nature, ARCC remains one of my favorite BDCs. Last year the company carried over about $643 million in spillover income. I’m not sure how much they plan to carry over going into 2024 but I suspect it’ll be close to last year’s amount. I expect management to make this announcement during Q4 earnings.

Price Has Held Up Well

Before Q3 earnings, ARCC was trading slightly below its NAV, closing at a price of $18.78 on October 20th. But since then, the price has risen above $19. Most BDCs have held steady over the course of six months due to their historical high-yields while many dividend stocks have fallen due to higher rates on safer, fixed-rate investments like bonds and CDs. Despite the BDC being up over the last 6 months, I think ARCC remains a buy for those with a long-term outlook. Furthermore, their current P/E is higher than the sector median but lower than their 5-year average of 9.62x.

Like I said ARCC is a SWAN stock and I plan to hold forever and the price has held up well since my last coverage and received a “strong buy” rating from Quant. Most analysts’ have the stock rated a strong buy as well, and although it trades at a slight premium to NAV, I agree with the strong buy recommendation. As I suspect rates to decline next year, I anticipate many BDC’s prices will follow as investors rotate back into lower-yielding dividend stocks. But ARCC isn’t just some high-yielder; it’s the largest, and one of the safest stocks in my opinion, regardless of sector.

Tipranks

Conclusion

Although some investors may prefer to invest in other BDCs that they consider to be more shareholder friendly, ARCC remains one of my favorites due to their conservative nature, and management’s forward thinking. ARCC prefers to rollover spill-over income into the next year. I think the reason the company has not raised the dividend this year is in preparation for a recession, or a higher for longer environment. These are the type of stocks you want to hold in your portfolio, ones with conservative management teams if we do enter into economic downturns. During the 3rd quarter, Ares Capital I think proved why they remain one of the top BDCs in the sector and I rate them a buy.

Read the full article here