Thesis Review

I have had a ‘buy’ rating on Ares Capital (NASDAQ:ARCC) since early July. Since publication of my last article on the stock, this pick has slightly underperformed the S&P500 (SPY) (SPX) (VOO) by +2.03%. Now, after reviewing the Q2 FY23 results and commentary, I am downgrading my stance to a ‘Neutral/Hold’ for the following reasons:

- Investment activity is yet to rebound materially

- The rising rates offset argument is fading

- Sectoral headwinds are weighing on portfolio quality

Investment activity is yet to rebound materially

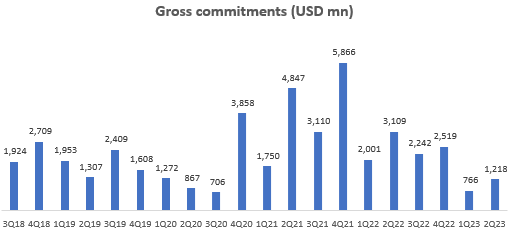

Gross commitments are a leading indicator of future investment activity. This rebounded a bit from Q1 FY23 levels, posting a 59% QoQ growth:

Gross Commitments (USD mn) (Company Filings, Author’s Analysis)

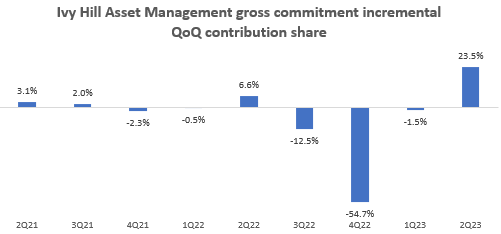

However, digging in a bit more, we see that this rebound was weighted toward 1 main source as Ivy Hill Asset Management contributed 23.5% to the uptick:

Ivy Hill Asset Management Gross Commitment Incremental QoQ Contribution Share (Company Filings, Author’s Analysis)

Now, I do acknowledge that this source of investment activity is composed of multiple return streams. So my concern is not so much on the concentration risk as it is the broad-based health of the rebound. Overall, I prefer to wait for more evidence of a sustained healthy rebound in investment activity.

The rising rates offset argument is fading

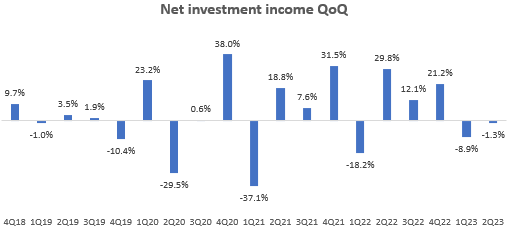

In my last update, my idea was that the slow investment activity is outweighed by the possible tailwinds of rate hikes. Well, the rate hike did occur as the Fed raised rates by 25bps to 5.25-5.50%, however Ares Capital still did not generate material alpha over my opportunity cost; the S&P500 passive indexing alternative.

Furthermore, the chances of another rate hike event is much lower now at 20% compared to 93% at the time of my previous update. Therefore, I do not see rising rates to be a major growth tailwind for net investment income going forward:

Net Investment Income QoQ (Company Filings, Author’s Analysis)

Sectoral headwinds are weighing on portfolio quality

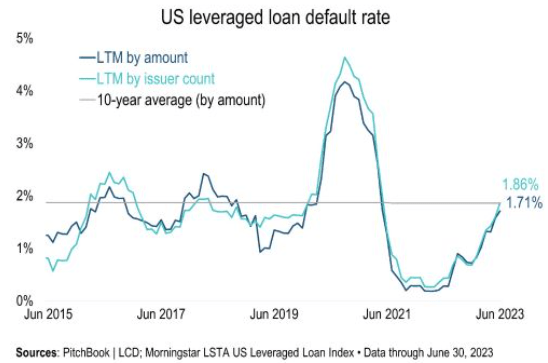

According to data from the Morningstar Loan Syndications and Trading Association (LSTA) US Leveraged Loan Index, the leveraged loans market is undergoing portfolio quality headwinds. The default rate is climbing up rapidly back toward the 10-yr average mark at 1.71%:

US Leveraged Loan Default Rate (PitchBook’s Leveraged Commentary & Data (LCD); Morningstar LSTA US Leveraged Loan Index)

And the outlook from Leveraged Commentary & Data (LCD)’s Leveraged Finance Survey expects the default rate to continue rising to 2.5-3% over the next 11 months.

The software and healthcare sectors together contributed to 40.1% of the overall distressed loans mix. This makes me wary of Ares Capital’s credit quality since these 2 sectors contribute 33.0% (see slide 12 in link) of the overall investment portfolio.

Now a key question is whether the sectoral trends applicable to Ares Capital. I am making an educated guess in saying yes it is because Ares Capital is the largest BDC company with ~20% share of total assets. Hence, sectoral trends are likely to be applicable to the market leader.

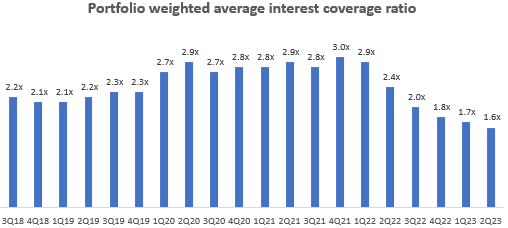

In my last update, I highlighted the company’s portfolio weighted average interest coverage ratio as the main risk and monitorable. In the Q1 FY23 call, management had suggested that 1.7x would be a bottom. However, in Q2 FY23, this fell another point to 1.6x:

Portfolio Weighted Average Interest Coverage Ratio (Company Filings, Author’s Analysis)

Overall, these data points about the sectoral headwinds on asset quality make me more cautious about Ares Capital’s portfolio quality.

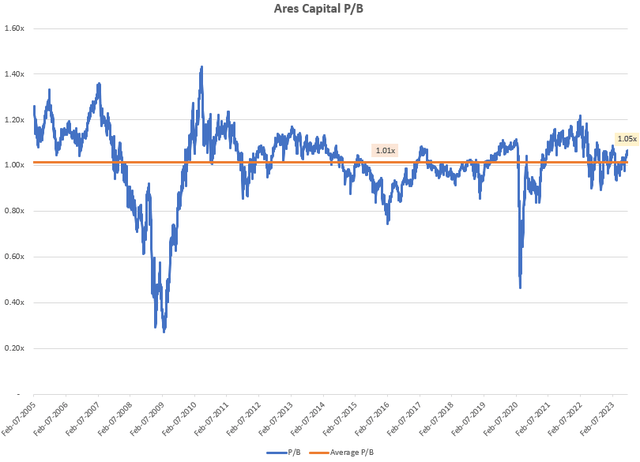

Valuations don’t give much margin of safety

Ares Capital P/B (Capital IQ, Author’s Analysis)

Ares Capital is currently trading at a P/B of 1.05x, which means a mere 3.8% premium to the longer term average of 1.01x. Given the weaker operating momentum in the business, I believe this does not provide sufficient margin of safety for buys.

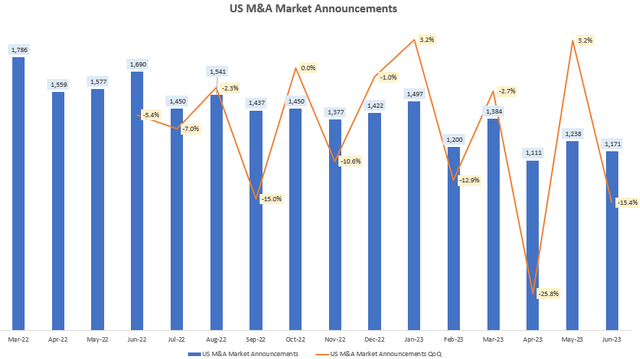

US M&A activity is a key leading indicator

In the earnings call, management highlighted that M&A activity will lead to a pickup in investment activity:

What’s really going to drive a pickup from here is just going to be more M&A activity. And as we’ve mentioned, we’ve got the benefit of having a large diverse portfolio that contributes to a lot of follow-on capital opportunities for us. But yes, to be materially busier, we just need the M&A environment to pick up.

– CEO Robert DeVeer in the Q2 FY23 earnings call

As the US makes up more than 90% of the investment portfolio, I am keeping track of US M&A deal activity as that is a key leading indicator of a material pickup in investment flow volumes and hence net investment income.

US M&A Market Announcements (FactSet FlashWire US Monthly July 2023, Author’s Analysis)

I would like to see sustained month-on-month (MOM) increases in the US M&A announcements trend to gain more confidence on investment deal volumes for Ares Capital.

Takeaway

My earlier buy stance on Ares Capital has not really played out as per my expectations. Now, after reviewing the Q2 FY23 results, I find it hard to justify a buy.

Investment activity posted a bit of a rebound but it is still below historical levels. Moreover, the rebound is not very broad-based, which would be a healthier sign.

In my last update, my thesis was that rising rates would be a driver of net investment income, offsetting the slowness in deal flow volumes. This has not really played out and the situation ahead also does not have the benefit of a likely rate hike anymore.

My research on sectoral data suggests seeping portfolio quality concerns in the leveraged loans market, in which Ares Capital is a market leader. Combining this macro perspective with the bottom-up data showing a continued fall in Ares Capital’s weighted average interest coverage ratio (contrary to management’s suggestion of a bottoming in Q1 FY23) gives one reasons to be more cautious about Ares Capital’s overall portfolio quality.

The valuations are also trading near the longer-term averages, reducing the margin of safety for a prudent buy decision. Hence, I am downgrading the stock to a ‘neutral/hold’. I may revise my thesis if M&A activity picks up as that would be a leading indicator of new investment activity.

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P500 on a total shareholder return basis, with higher than usual confidence

Buy: Expect the company to outperform the S&P500 on a total shareholder return basis

Neutral/Hold: Expect the company to perform in-line with the S&P500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P500 on a total shareholder return basis, with higher than usual confidence

Read the full article here